这家传统银行是怎么喜欢上区块链的?

|

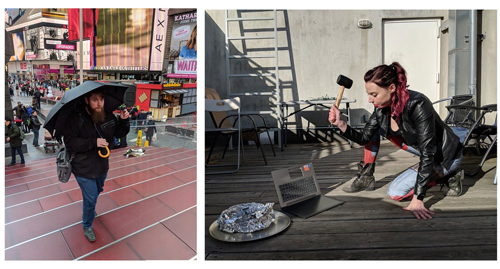

在曼哈顿时代广场附近的百思买(Best Buy)柜台上,安布尔·巴耳代抛起了一个特大号的黄色骰子。 五点。 巴耳代说:“奇数。”这个结果确定了她选择的电脑。如今她所有的决定都采用这种方式,借此迷惑任何尾随的间谍。她身穿军绿色法兰绒上衣,脚踩带有饰钉的黑色皮靴,选择了“奇数”对应的249美元联想(Lenovo)电脑。而“偶数”对应的电脑是旁边的169美元款。 她的同事帕特里克·麦伦德·尼尔森问:“你确定不要再掷几次,选到那款便宜的?”遭到拒绝后,他把盒子拿给了收银员。 这趟古怪的购物之旅发生在3月中旬的一个星期二。当时,巴耳代是美国最大银行、《财富》美国500强排名第20的公司摩根大通(JPMorgan Chase)的区块链项目主管。而尼尔森是摩根大通的首席工程师,他建立了区块链Quorum,这种分布式会计总账采用了加密货币网络以太坊(Ethereum)背后的技术。 某种程度上说,两人如今正在休假……他们在计划把数据载入这台笔记本电脑——他们将此称为“燃烧炉”,因为它的确是要按照字面意思被焚毁的。这是升级大零币(Zcash)代码的过程之一。这种加密货币类似比特币(Bitcoin),不过隐私性要强大许多。它通过名为“零知识证明”的数学方法,让匿名在理论上成为了可能。为了让他们的代码用于验证,巴耳代和尼尔森必须编写一个秘密公式,并摧毁痕迹。假如危险分子获取了数据,他们就能制造出无限的大零币,这是不可接受的。 身穿蓝色衬衫的收银员工扫描了包裹的条形码,并问道:“你们要用这个干什么?” 尼尔森面无表情地表示:“做一件事,然后毁掉它。”在他长到胸口的大胡子中,完全看不到一点笑容的痕迹。但推销员并未气馁,他继续问道:“你们需要延长保修期吗,或者安装一套微软(Microsoft)Office办公软件?” 尼尔森表示:“不,我们会摧毁它。” 售货员皱起了眉头。他试探道:“你们要用它做试验之类的吗?” “我们要砸烂它然后烧掉——” 巴耳代打断了他:“是啊,做科学实验。”她给了销售员一张纸,上面有个二维码。“这就是我们做的事情,如果你觉得无聊,可以看看。” |

Amber Baldet flings an oversize yellow die atop a display counter at a Best Buy near Times Square in Manhattan. Five. “It’s odd,” says Baldet. The outcome dictates her choice of laptop. Today she’s making all her decisions this way—a precaution intended to confound any trailing spies. Dressed in an army-green flannel shirt and black leather boots with studs, Baldet selects a $249 Lenovo computer, the “odd” designee, vs. a neighboring $169 “even” option. “You sure you don’t want to roll again until you get the cheaper one?” asks Patrick Mylund Nielsen, her colleague. Negative. He whisks the box to a cashier. On the mid-March Tuesday when this eccentric shopping trip takes place, Baldet is head of the blockchain program at JPMorgan Chase, the biggest bank in America and No. 20 on the Fortune 500. And Nielsen is lead engineer of the ¬JPMorgan Chase–built blockchain Quorum, a distributed accounting ledger adapted from the technology behind the cryptocurrency network Ethereum. The pair is taking off from work today … sort of. They’re planning to load data onto the laptop—a “burner,” literally to be incinerated—as part of a process aimed at upgrading the code behind Zcash, a crypto¬currency similar to Bitcoin except with significant privacy enhancements. Zcash enables anonymity, in theory, through mathematical techniques called “zero knowledge proofs.” To contribute their portion of the code for the proofs, Baldet and Nielsen must cook up a secret formula—and destroy the ingredients. If a bad actor compromised the data, the troublemaker could manufacture an infinite supply of Zcash, an inadmissable proposition. “What are you going to use this for?” inquires a blue-shirted checkout clerk, scanning the package’s bar code. “Doing one thing, and then we’re going to destroy it,” Nielsen deadpans. Any hint of grin is obscured under his chest-length thicket of beard. The sales rep, undeterred, continues his script. “Do you need an extended warranty, or Microsoft Office Suite?” “Nope,” Nielsen says. “We’re going to destroy it.” A crease forms on the salesman’s forehead. “Are you doing an experiment or something?” he probes. “We’re going to smash it and then burn—” “Yup! It’s for science,” Baldet chimes in. She hands the salesman a slip of paper bearing a QR code. “That’s what we’re working on, if you get bored you can look it up.” |

|

该项目确实是个科学实验——不是两个伪装的华尔街人士做的那种典型实验,反而可以让雇主获益。的确,摩根大通与大零币的结盟关系对主流银行而言很不寻常。该公司把大零币的密码算法整合到了Quorum中,有朝一日,它可能会让银行间的交易免于窥探。这家金融巨头与澳新银行集团(Australia and New Zealand Banking Group)和加拿大皇家银行(Royal Bank of Canada)一起,在去年秋季建立了“银行间信息网络”,探索如何使用Quorum提升全球支付系统的效率。尽管这种尝试目前还处于初期阶段,但摩根大通表示,这个项目和其他类似项目有助于把交易处理的延迟从几周缩短到几个小时;考虑到银行财产服务业务涉及的资产高达每天6万亿美元,这项技术可能会产生巨大的影响。 不过考虑到这项工作的特殊性质,巴耳代和尼尔森很谨慎地避免越过银行的界限。离开百思买后,巴耳代对我强调说她不希望这趟加密之旅以任何形式牵扯到摩根大通。她坚持道:“要明确,我们只是以个人身份做这件事。” “他们认为我们疯了。” 从摩根大通首席执行官杰姆·戴蒙对比特币的斥责来看,他可能是地球上最不愿意雇用巴耳代和尼尔森的人。他的批评言论屡次占据标题,也让他在加密货币领域的博客上遭到了妖魔化(有时候人们会把他的姓氏Dimon改成Demon,称其为“杰姆·德蒙”)。2015年11月,在旧金山的《财富》全球论坛上,戴蒙预测政府会制裁这些不受管制的货币。他宣称:“折腾比特币纯属浪费时间。”去年9月,比特币一路猛涨到接近2万美元的高点,这时戴蒙重申了他的怀疑态度。他表示:“比特币就是诈骗。”并声称要开除任何交易比特币的员工。一个月后,他又补充道:“如果你蠢到去买比特币,总有一天你会付出代价。” 戴蒙后来说他很后悔发表那些观点。不过作为一名每天要处理四分之一美元总量的金融巨头的领导者,戴蒙很有理由对这种藐视管理、价格剧烈波动且没有预兆的资产表示怀疑。没错,摩根大通拥有超过5万名技术专家,几乎是Facebook总员工的两倍。不过比起银行许多使命重大的技术业务职能——维持价值流让公司和消费者得到资金、贷款和投资——加密货币似乎金融价值不大,徒然令人分心。尽管如此,戴蒙的公开鄙视也隐含了一个微妙的事实:银行如何看待加密货币、区块链,以及它们诱人却可能未被察觉的潜力。 “实际上我们已经在用它了。它在很多方面都会发挥作用。上帝保佑区块链。” ——摩根大通首席执行官杰米·戴蒙 戴蒙在去年10月生硬拒绝比特币后不久,Chain的首席执行官亚当·卢德温就给戴蒙写了一封公开信,阐述加密技术的潜在价值。这家初创公司已经登陆纳斯达克,并获得了Visa的支持,为金融业打造区块链。公开信获得了近50万次阅读,很快就被送到了戴蒙的办公桌前。戴蒙与卢德温通了个电话。卢德温回忆道:“你知道,他本来可以很轻易地说,你怎么敢用我的名字骗点击,但相反,他很欣赏我写的内容以及其中蕴含的思想。他对此的认真态度也让我印象深刻。” |

The project is indeed a science experiment—not one typical of two ostensible Wall Streeters, but one that could benefit their employer. Indeed, JPMorgan Chase’s relationship with Zcash represents a very unusual alliance for a mainstream bank. The firm has incorporated the cryptography behind Zcash into Quorum, where one day it may shield transactions among banks from prying eyes. Along with Australia and New Zealand Banking Group and the Royal Bank of Canada, the financial titan in the fall formed an “interbank information network” to explore how to use Quorum to make global payments more efficient. Although the venture is in its early stages, JPMorgan Chase says the program, and others like it, could help reduce transaction-processing delays from weeks to hours; at the scale of the bank’s treasury-services business, which facilitates a staggering $6 trillion in payments per day, the technology could be a game changer. But given the peculiar nature of the day’s task, Baldet and Nielsen are cautious about not overstepping the bank’s perceived boundaries. While leaving Best Buy, Baldet emphasizes to me that she doesn’t want this cryptoconjuring expedition to reflect on JPMorgan Chase in any way. “Just make clear we’re doing this in a personal capacity,” she insists. “They think we’re batshit crazy.” Based on his denunciations of Bitcoin, JPMorgan Chase CEO Jamie Dimon might seem like the last person on earth who would employ Baldet and Nielsen. His criticisms have commanded headlines and earned him demonization (sometimes literally, in the form of the nickname “Jamie Demon”) on cryptocentric blogs. Speaking at Fortune’s Global Forum in San Francisco in November 2015, Dimon predicted that governments would crack down on ungoverned moneys: “You’re wasting your time with Bitcoin,” he asserted. Last September, as Bitcoin prices began a run-up to near-$20,000 highs, Dimon reiterated his skepticism. “Bitcoin is a fraud,” he said, promising to fire any employees who traded it. A month later, he added, “If you’re stupid enough to buy it, you’ll pay the price for it one day.” Dimon later said he regretted airing his opinion. But as a man who runs a financial behemoth that handles a quarter of the U.S. dollar supply on any given day, Dimon has good reason to be cynical about an asset class that defies governance and whose price fluctuates wildly and without warning. Yes, ¬JPMorgan Chase employs more than 50,000 technologists—almost twice the total number of employees at Facebook. But compared with the bank’s many mission-critical tech operations—functions that sustain the flow of value that lets busi¬nesses and consumers get paid, take out loans, and invest in new endeavors—crypto¬currency can seem like both a financial pip-squeak and a distracting sideshow. Still, behind Dimon’s public dismissals lies a subtler truth about the bank’s relationship to cryptocurrencies, blockchains, and their enticing if still unrealized potential. “We actually use it. It’ll be useful in a lot of different ways. God bless the blockchain.” ——Jamie Dimon: CEO, JPMorgan Chase On the heels of Dimon’s blunt October rejection, Adam Ludwin, CEO of Chain, a Nasdaq- and Visa-backed startup building blockchains for the financial industry, addressed an open letter to Dimon elucidating the potential value of cryptotechnologies. The piece racked up nearly half a million reads, and promptly crossed the desk of Dimon, who arranged a call with his interlocutor. “He could have easily said, you know, how dare you use my name as clickbait, but instead his perspective was that he appreciated the note and the thinking in it,” Ludwin recalls of their conversation. “I was, in turn, impressed that he took it seriously.” |

|

确实,尽管戴蒙似乎贬低了加密货币,但他对支持这些货币的技术赞不绝口。去年,就在他质疑比特币买家智商的那个大会上,他也表示:“上帝保佑区块链。”他给了员工充分的空间去研究随心所欲的加密货币世界中的试验性技术,这种自主权远超其他大部分银行。 举个例子,Quorum就源于使用谷歌(Google)构思的编程语言Go的软件客户端。当加密货币社区改良了市值仅次于比特币的加密货币以太坊时,摩根大通的区块链工作人员也可以获取那些更新。类似的,可以支持数字代币交易的Quorum“零知识安全层”,也是与大零币的开发商Zerocoin Electric Coin Co.合作开发的。 戴蒙的“欺诈”言论激起了社交媒体的强烈反响,安布尔·巴耳代转发了推特,附上了一个“¯\_(ツ)_/¯”的表情符号,这个淡定的耸肩是混迹于网络的一代人喜欢使用的标志性表情。在去年秋天的Money 20/20金融科技大会上,她的回答更加微妙。“对大部分其他银行而言,站出来说‘区块链好,比特币不好’都情有可原,因为他们可以明确把两者区分开来。考虑到摩根大通既与以太坊有联系,又与创造大零币的那批人有联系……这番话就意义不大了。” 跨国公司都是跨界机构,其中有许多充满各种担忧和梦想的独立思考者。这些公司高层领导的信念,并不总能匹配或很好地概括公司内部的情绪。在摩根大通区块链项目中,金融巨头谨慎、以盈亏为导向的领导风格与新技术架构者无法无天的创造性能量共存着,并往往能结出硕果。 实际上,摩根大通已经有了巨大的进步,模糊了公共区块链(加密货币领域的蛮荒西部)与具有商业亲和力的私人或“得到许可的”区块链(未来高效的金融基础设施的基石)之间的界限。随着这些技术走向成熟,它们的崛起可能很大程度上要归功于许多看起来不相配的合作关系,戴蒙和巴耳代的联系就属于这一种。 2015年2月,摩根大通网站的岗位列表上出现了一个不同寻常的工作。岗位描述写道:“你在意颠覆,对比特币和其他加密货币有一些想法,可能对于为大型金融机构工作的前景感到矛盾。”《华尔街日报》(Wall Street Journal)当时如此描述这种自我贬低的态度:“他们需要那些不太想为他们工作的人。” 摩根大通需要新鲜血液——众所周知,在技术巨变的时代,许多拥有百年历史的机构都有这种愿望。为此,该银行在2014年成立了一个名为“新产品开发”(New Products Development)的特殊团队。该团队研究的都是热门话题,包括云计算、数字化和对开发者更友好的编程界面,这也是安布尔·巴耳代最终加入的团队。 |

Indeed, as down as Dimon may seem on cryptocoins, he has lavished praise on the technology undergirding them. “God bless the blockchain,” he said last year, at the same conference where he questioned the intelligence of Bitcoin buyers. And he has given employees a long leash to work on experimental technologies drawn from the freewheeling cryptocurrency world, with far greater autonomy than most banks have conferred. Quorum, for instance, is a derivation of a software client that uses the Google-conceived programming language Go. When the cryptocommunity makes improvements to Ethereum, the second-largest cryptocurrency network by market value after Bitcoin, JPMorgan Chase’s blockchain crew can piggyback on those updates. Similarly, Quorum’s “zero-knowledge security layer,” which enables transactions involving digital tokens, was built in collaboration with the Zerocoin Electric Coin Co., makers of Zcash. When Dimon’s “fraud” comment lit up social media, Amber Baldet retweeted coverage with her take: “¯\_(ツ)_/¯,” the unflappable shrug emoji, iconic among a generation weaned on the web. At last fall’s Money 20/20 fintech conference, she offered a more nuanced response. “For most other banks it probably makes sense to stand up and say, ‘Blockchain good, Bitcoin bad,’ because you can completely draw a hard line between the two. Given the activity that JPMorgan has had both with Ethereum and with the folks who created Zcash … it’s less sensical.” Multinational corporations are sprawling organizations—collections of independent thinkers who encompass a diversity of dreads and dreams. The beliefs of their top officers don’t always match, or neatly summarize, the sentiments within. And in JP¬Morgan Chase’s blockchain efforts, a financial giant’s cautious, bottom-line-oriented leadership has coexisted, often fruitfully, with the entrepreneurial, anarchic energies of a new technology’s architects. In truth, the bank has made enormous strides in blurring the lines between public blockchains—the Wild West world of cryptocurrencies—and business-friendly private or “permissioned” blockchains, the building blocks of future efficient financial infrastructures. As these technologies mature, their ascendance may owe a lot to the kinds of odd-couple relationships that linked Dimon and Baldet. In February 2015, an unusual job listing appeared on JPMorgan Chase’s website. “You care about disruption,” the description read, in part. “You have an opinion on Bitcoin and other cryptocurrencies, and you are probably ambivalent about the prospect of working for a large financial institution.” As the Wall Street Journalcharacterized the self-deprecation at the time: “They need people who aren’t eager to work for them.” JPMorgan Chase wanted fresh blood—a desire known to many a century-old institution in days of technologic upheaval. To tap it, the bank created a skunkworks in 2014 called New Products Development. The team pursued the buzziest topics, including cloud computing, digitization, and developer-friendly programming interfaces—and it’s where Amber Baldet eventually landed. |

|

巴耳代起初不像个银行家。她一直喜欢反主流文化,游荡于黑客圈。2008年,她搬到纽约,在一家小型避险基金公司工作,当时公司和经济都不景气。随后她进入了咨询公司Capco,在那里为摩根大通工作,直到2012年全职加入摩根大通。她的反叛精神并未消减,在“占领华尔街”(Occupy Wall Street)的活动中,她摆出了一个造型,让莫利·卡巴博摄影,后者是一位激进的艺术家,以描绘关塔那摩监狱(Guantánamo Bay)的生活而闻名。在场景中,巴耳代戴着墨镜,靠着一块标志牌,上面写着“支持现实财政改革的华尔街员工。我们的人数比你们想象中更多。”这幅照片如今还挂在纽约历史学会(New York Historical Society)。 在摩根大通,巴耳代进入了新产品开发团队,最早从事的是机器学习研究。随着对企业区块链的热情日益增加,这个团队在此类项目上的战略投资翻了一番。公司给Digital Asset投入了大量资金。前摩根大通高管布莱斯·马斯特斯认为正是该公司发明了信用违约交换,尽管这一观点存在争议。摩根大通是研究以太坊技术的企业以太坊联盟(Enterprise Ethereum Alliance)的创始成员,也是Linux基金会(Linux Foundation)跨行业区块链合作集团,即之后被称为“超级账本”(Hyperledger)的项目的创始成员。 “对大部分其他银行而言,站出来说‘区块链好,比特币不好’都情有可原。” ——安布尔·巴耳代,前摩根大通区块链领导 同时,摩根大通还有了更进一步的发展,打造了自己的内部技术。然而,情况变得很明显,银行注重合规性的文化无法与区块链技术专家共享一切的气质无缝对接。近年来,摩根大通的区块链试验前途光明,但留住它们的创造者却难度重重。 第一批测试的项目中,有一个名为Juno的分布式总账。区块链系统在使用量巨大的情况下往往会“疲劳”,效率降低,Juno的设计目的就是让它们复原力更强。技术专家斯图尔特·波普乔伊与他的主要编码员威尔·马蒂诺领导了这个项目的开发。他们做的事情对摩根大通而言十分新鲜,但摩根大通几乎没有发布开源软件的经验。(马蒂诺兴奋地在代码分享网站Github用自己的私人账户发布了Juno的代码。)当团队在2016年的超级账本会议上推出Juno时,摩根大通拒绝发布关于它的新闻稿。波普乔伊对《财富》表示:“很明显,如果我们想真正兑现这项技术的潜力,就要自己跳出来干。”他们那一年离开了摩根大通,他们的新项目Kadena募集了近1,500万美元的资金,创始人表示《财富》排名前100的医疗公司已经与他们签订了合同,成为了他们的客户。 |

Baldet was an unlikely banker from the start. She has long had an affinity for counterculture and hung around hacker circles. She moved to New York in 2008, taking a job at a boutique hedge fund just as the firm—and the economy—unwound. She later joined a consultancy, Capco, where she did work for JPMorgan Chase before moving there full-time in 2012. Her rebelliousness persisted; during Occupy Wall Street, she posed for a portrait by Molly Crabapple, an activist-artist known for depicting life at Guantánamo Bay. In the scene, Baldet wears shades and leans on a sign that reads, “Wall Street workers for realistic fiscal reform. There are more of us than you think.” It now hangs at the New York Historical Society. At JPMorgan Chase, Baldet found her way to New Products Development, working at first on machine learning. As enthusiasm for enterprise blockchains surged, the group doubled down on strategic investments in such projects. The company pumped funds into Digital Asset, a startup helmed by Blythe Masters, a former JPMorgan Chase executive credited, controversially, with inventing the credit default swap. The bank was a founding member of the Enterprise Ethereum Alliance, a consortium of businesses exploring that technology, as well as of the Linux Foundation’s cross-industry blockchain collaboration group, later dubbed Hyperledger. “For most other banks it makes sense to stand up and say, ‘blockchain good, Bitcoin bad.'” ——Amber Baldet, former JPMorgan Chase blockchain leader Concurrently, the bank went further still, building its own technology in-house. It soon became clear, however, that the compliance-conscious culture of the bank wouldn’t be a seamless fit with the share-everything ethos of blockchain tinkerers. In recent years, JPMorgan Chase’s blockchain experiments have been promising; keeping their creators in the fold has proved challenging. Among the first test cases was a distributed ledger known as Juno. Blockchain systems often tucker out under heavy use; Juno was designed to make them more resilient. Technologist Stuart Popejoy led the project’s development with his main coder, Will Martino. What they were doing was so new to JPMorgan Chase, however, that the bank had little experience with releasing open-source software to fall back on. (Martino wound up releasing Juno’s code under his personal account on Github, a code-sharing website.) When the team unveiled Juno at a Hyperledger meeting in 2016, JPMorgan Chase declined to issue a press release about it. “It became clear to us if we really wanted to realize the potential of this technology, we needed to go out on our own,” Popejoy told Fortune. They left the bank that year; their new project, Kadena, has raised nearly $15 million, and the founders say they’ve signed on a Fortune 100 health care company as a client. |

|

那时,巴耳代已经成为了产品团队区块链领域实际上的领导者。她招聘的第一个人是克里斯汀·莫伊,之前在马斯特斯手下做过一段时间的券商。随后帕特里克·尼尔森也加入了他们。他曾在近来陷于困境的俄罗斯杀毒软件开发商卡巴斯基实验室(Kaspersky Lab)担任研究员。最后,尼尔森成为了Quorum的首席开发人员。 随着时间的推移,Quorum开始模拟区块链,让主流的金融服务供应商团结在一起。它便于使用,而附带的私人信息工具Constellation意味着它可以保证机密性,这是吸引许多银行客户的筹码。而其前瞻性的零知识安全层(zero knowledge security layer)又可以在未来带来更多价值——私下完成的数字资产交换。与此同时,摩根大通的管理制度也有所发展,开始接受新产品的文化:等到团队做好准备,在开源软件许可之下发布Quorum时,也能够让它合规了。摩根大通用了官方的Github账户发布了相关代码。 Chain的卢德温谈到以太坊和大零币时表示:“这些试验初步涉及了其他银行认为不可捉摸的技术。我认为安布尔在其中居功至伟,杰米也起到了很大贡献。” |

By then, Baldet had become the de facto leader of the product team’s blockchain efforts. Her first hire was Christine Moy, a former securities trader who worked for a stint under Masters. They were eventually joined by Patrick Nielsen, a former researcher at Kaspersky Lab, the lately embattled Russian antivirus maker; eventually, Nielsen became the lead developer on Quorum. Over time, Quorum began to resemble a blockchain that mainstream financial-service providers could rally behind. Its ease of use and its private messaging tool, Constellation, meant it could provide confidentiality that would be table stakes for many banking clients. And its forward-looking zero knowledge security layer promised to bring more value—privately settling digital asset swaps—in the future. JPMorgan Chase’s regulatory regime, meanwhile, had grown to embrace new-product culture: By the time the group was ready to release Quorum under an open-source software license, it could do so in a way that met compliance, and the bank released it under an official Github account for JPMorgan Chase. “They were early to experimentation with what other banks would have viewed as untouchable technologies,” says Chain’s Ludwin, referring to Ethereum and Zcash. “I give Amber a lot of credit for that, and also [credit] Jamie for enabling that.” |

|

尽管如此,Quorum的采用,甚至它在摩根大通的未来,都还远未确定。由于Quorum是开源的,所以摩根大通必须谨慎处理反垄断问题,因为这种合作涉及了与其他银行的联手。为此和其他原因,行业的内部人士推测Quorum最好是由超级账本这样的团体或金融技术开源基金会(FINOS)之类的金融业团体来监管。摩根大通的首席信息官洛里·比尔表示,它的命运还悬而未决。她说:“我们相信它是一种很出色的资产。我们会继续评估Quorum进化和发展的最佳方式。” 然而,这种进化不会在巴耳代和尼尔森的领导下进行了。今年4月,他们宣布辞职。巴耳代表示:“我们只是希望离开高度管制的实体,这样动作更快一些。” 巴耳代和尼尔森憧憬在不远的将来,得到许可的(企业用)区块链和公共(类似比特币的)区块链能够更加紧密地结合。巴耳代把如今区块链的状态比作几年前企业评估亚马逊网络服务(Amazon Web Services)或微软(Microsoft)Azure等公共云时候的情况。最终,人们会提出包含私人云和公共云的混合云方案,从而让商业经营更具弹性和效率。(克里斯汀·莫伊接替巴耳代成为了摩根大通团队的主管,她对区块链世界有着类似的看法,她最近对Coindesk网站表示:“也许将来某一天这些都会整合起来。”)这是巴耳代和尼尔森创立Clovyr的动机之一。他们这家新的初创公司的名字来源于高速公路驶入匝道和驶出匝道的立体交叉结构。 Clovyr将为对区块链感兴趣的开发商、企业和消费者服务。巴耳代的产品理念包括一个为台式电脑准备的、类似浏览器的工具,它可以帮助用户接通竞争的区块链,使用分布式的应用,从而测试最新的创新成果。尼尔森开始编写初步的代码,公司也开始了融资。在他们看来,区块链的竞赛不一定非要有一个赢家。公司和人们——包括杰米·戴蒙——应该可以联手搞清到底哪些管道和部件最适合他们。 不过在Clovyr 5月中旬的发布会之前,巴耳代和尼尔森还有最后一个任务要完成,让Quorum和摩根大通获益。我来到了巴耳代在布鲁克林的公寓,见证了这一过程。她的猫莉莉在客厅昂首阔步地边走边叫,而两人正在拆卸一台笔记本。这是大零币编码贡献的最后一步。 前一天,两天在纽约的时代广场和联合广场进行了录制采访,还使用了巨大的伞来遮蔽空中的窥探。他们采访了一对加拿大夫妻、一位抽大麻的以色列演员、一位佛教徒还有其他人,询问他们对于隐私、加密货币和监管的看法。他们捕捉了鸽子在公园中飞翔、出租车按喇叭和一位牙买加女士在地铁上喊着下流话的镜头。这样做是为了以视频文件的形式,产生一些任何人都无法再现的数据,然后把这段视频导入一个程序,将其转化为大零币核心的私密技术要用到的基础代码。 这项工作完成后,就到了毁灭的时刻。在巴耳代的屋顶,她拿出了一只丙烷喷灯,融毁了计算机的内部架构,尤其是记忆芯片。燃烧后的残渣发出了刺鼻的气味。巴耳代表示:“我们这道火炖电路板做得不错。” 回到厨房里,尼尔森发现电脑的一部分还没有彻底被毁坏。巴耳代把它放到了灶台的平底锅中。随后,她打开了抽油烟机,让火焰吞噬金属和塑料碎片。她和尼尔森把浓烟扇向排气扇。随着最后一点白烟飘上天空,仪式就这样结束了。(财富中文网) 本文最初登载于《财富》2018年6月1日刊。 译者:严匡正 |

Still, Quorum’s adoption and even its future at JPMorgan Chase are far from assured. Because Quorum is open-source, the bank must carefully navigate antitrust regulations, since such collaborative efforts involve coordinating with other banks. For that reason and others, industry insiders have speculated that Quorum would be better off overseen by a group like Hyper¬ledger or a financial-industry consortium, like FINOS. Lori Beer, JPMorgan Chase’s chief information officer, says its fate is yet to be decided. “We believe it’s a really fantastic asset,” Beer says. “We’ll continue to assess what is the best approach to evolve and grow Quorum.” That evolution won’t take place under Baldet and Nielsen, however; in April, they announced their resignation. “We simply wanted to move more quickly than was really possible at a highly regulated entity,” Baldet says. Baldet and Nielsen envision a world, not far off, where permissioned (business-ready) and public (Bitcoin-like) blockchains are joined much more closely. Baldet compares the state of blockchains today to the period a few years ago when corporations were weighing using public clouds such as Amazon Web Services or Microsoft’s Azure. Eventually, they settled on hybrid architectures that include both private and public clouds, enabling more resilient, efficient ways of doing business. (Christine Moy, who succeeded Baldet as head of the JPMorgan Chase team, sees the blockchain world similarly; she recently told the website Coindesk, “Maybe someday this will all converge.”) That’s part of Baldet’s and Nielsen’s impetus to found Clovyr, their new startup, which takes its name from the cloverleaf infrastructure of highway on-ramps and off-ramps. Clovyr will serve blockchain-curious developers, businesses, and consumers. Baldet’s product ideas include a browserlike tool for desktops to help users plug into competing blockchains and play with decentralized apps, in order to experiment with the latest innovations. Nielsen has started writing preliminary code, and the company has begun fundraising. There doesn’t have to be one winner in the blockchain race, in their view. Businesses and people—including Jamie Dimon—should be able to cobble together whatever pipes and component parts work best for them. But before Clovyr’s mid-May launch, Baldet and Nielsen have one last task to complete to benefit Quorum and JPMorgan Chase, in an event I’ve come to Baldet’s Brooklyn apartment to witness. Her cat, Lily, prances around the living room and mews while the duo dismantle a laptop—the last stage of the Zcash code-contribution ceremony. The day prior, the duo had conducted video-recorded interviews in New York’s Times Square and Union Square, using huge umbrellas to block eyes-in-the-sky from snooping. They interviewed a Canadian couple, an Israeli actor smoking a spliff, and a Buddhist monk, among others, for their thoughts on privacy, cryptocurrency, and surveillance. They caught footage of pigeons flapping around parks, taxis honking, and a Jamaican lady yelling an obscenity at them on the subway. The goal was to generate data in the form of a video file that would be impossible for anyone to reproduce, and then to feed that video into a program that converted it into foundational code for the privacy tech at the heart of Zcash. With that work completed, it’s time for destruction. On Baldet’s rooftop, she whips out a propane blowtorch and melts the computer’s innards, taking special care to incinerate the memory chips. An acrid miasma emanates from the pan in which the detritus sits. “We’re making a nice PCB stew,” Baldet says. Back in her kitchen, Nielsen identifies an insufficiently demolished piece of the computer. Baldet places it in a pan on her stovetop. She turns on a range-hood vent, and lets the flame rip—frying the metal and plastic bits. She and Nielsen waft smoke through the exhaust fan. A faint white cloud escapes heavenward. And thus the ritual concludes. This article originally appeared in the June 1, 2018 issue of Fortune. |