美国政坛将上演“10月惊奇”,可能影响未来数年的投资市场

Bernhard Warner

2020-10-14

这个月发生的事件可能会持续影响美国未来四年甚至更长时间。

文本设置

文本设置

Plus(0条)

Plus(0条)

一场颇具争议的总统大选可能演变成严重宪法危机。第三波新冠疫情来袭。经济刺激救助计划在华盛顿陷入僵局。

进入10月,在2020年最后一个季度的开端,这些问题成为笼罩在市场上空的阴影。资深投资者或许想要避开第四季度,这是可以理解的,因为这是总统大选年常用的投资策略。

然而,今年的情形不同寻常。10月第一周,纳斯达克和标普500指数都上涨了2.2%,股市的涨幅足以收回整个9月的损失,这也符合今年让人完全无法预测的局势。

到底出了什么问题?

你可以把它称作提前到来的“10月惊奇”,而且它可能会持续影响未来四年甚至更长时间。

美国总统特朗普新冠肺炎检测呈阳性,可能打乱了他的连任计划,但却对市场产生了积极影响。从那一刻开始,乔•拜登巩固了自己在民调中的领先优势,提高了当选的几率,而华尔街和投资者开始思考一位民主党总统入主白宫和民主党在国会大胜之后,其投资组合的表现。

投资公司BMO Capital Markets 的债券分析师伊恩•林根上周在一篇投资者报告中写道:“拜登当选的几率持续上升,民主党在国会完胜的可能性也在提高。如果说最近投资高风险资产有任何指导意义的话,那么这种不可测事件对于国内股票市场的影响绝对是积极的。”

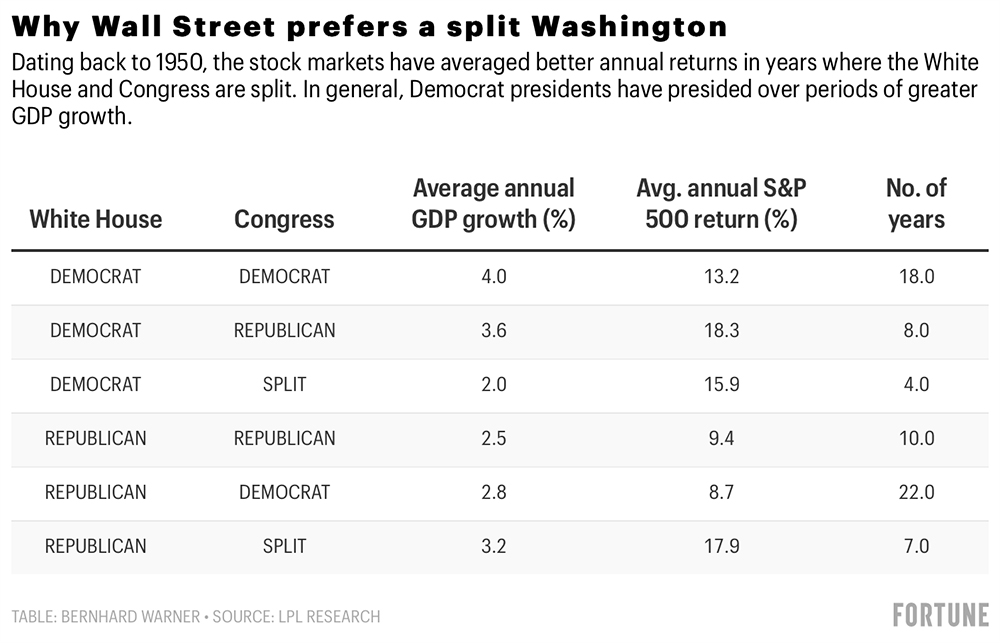

通常情况下,华尔街并不喜欢华盛顿被一党控制。其实,华尔街更倾向坚持低税率和解除监管的共和党人入主白宫。这种渴望情绪根深蒂固,即便历史数据并不支持这样的偏执。

但今年的故事情节发生了反转。面对明年1月华盛顿可能被民主党绝对掌控的情景,华尔街不仅表现地非常平静,甚至有些乐见其成。

支出和税收

如果拜登当选,意味着2021年之后政府可能要加税,但越来越多华尔街分析师认为,拜登当选利大于弊。

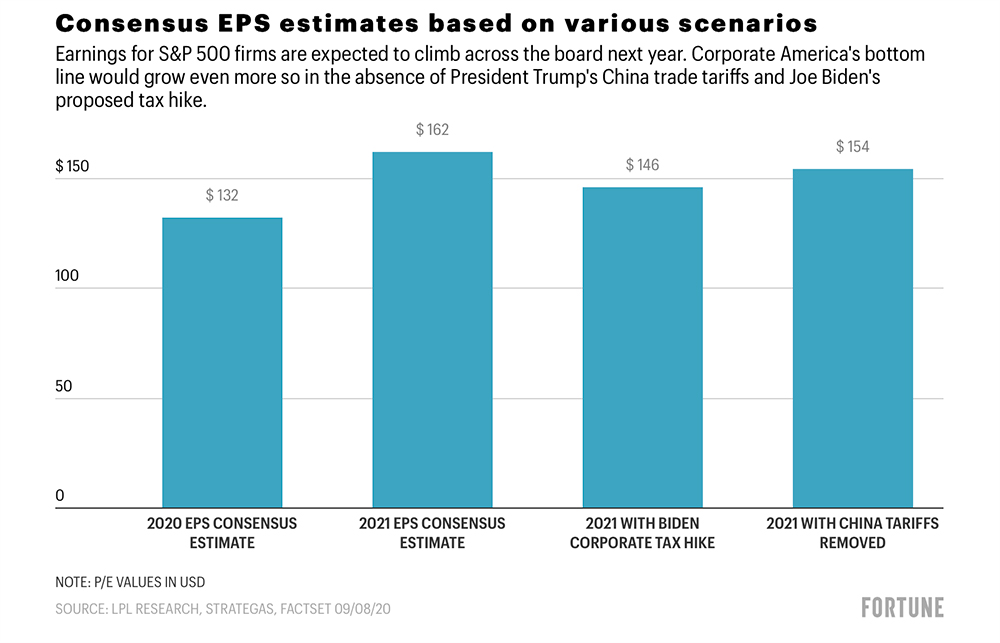

高盛(Goldman)的首席经济学家贾恩•哈奇乌斯上周对投资者说:“如果民主党完胜,我们可能会更新预期。因为1月20日总统就职典礼之后,政府很快通过至少2万亿美元财政刺激方案的可能性会大幅提升。之后,政府可能会增加在基础设施、气候、医疗和教育等领域的长期支出,至少可以抵消对企业和高收入者长期加税的影响。”

LPL Financial Research的副总裁兼市场策略师杰夫•布赫宾德同样认为不必担心民主党完胜。布赫宾德认为,拜登领导下的白宫通过大规模消费刺激方案和终止特朗普时代的贸易战,是美国企业界的福音,能够抵消民主党加税的负面影响。LPL公司的计算显示,对于企业收入最有利的情况是恢复自由贸易和不加税。

布赫宾德表示,拜登加税可能使公司收入减少10%(高盛计算的结果为9%),但取消对中国和欧洲等美国主要贸易伙伴的关税可以提高每股收益,两者能够相抵。

另外,值得注意的是,分析师都认为拜登的加税计划在被签署成法律之前会大打折扣。班森集团(Bahnsen Group)的创始人及执行合伙人戴维•班森告诉《财富》杂志:“美国历史上没有一位总统在竞选中提出的税收计划能够丝毫不差地变成税法。从来没有。”

尽管如此,我们依旧需要分析哪些行业最后可能会受到拜登税收计划的影响。与任何新税收计划一样,总有人会获利,有人会蒙受损失。

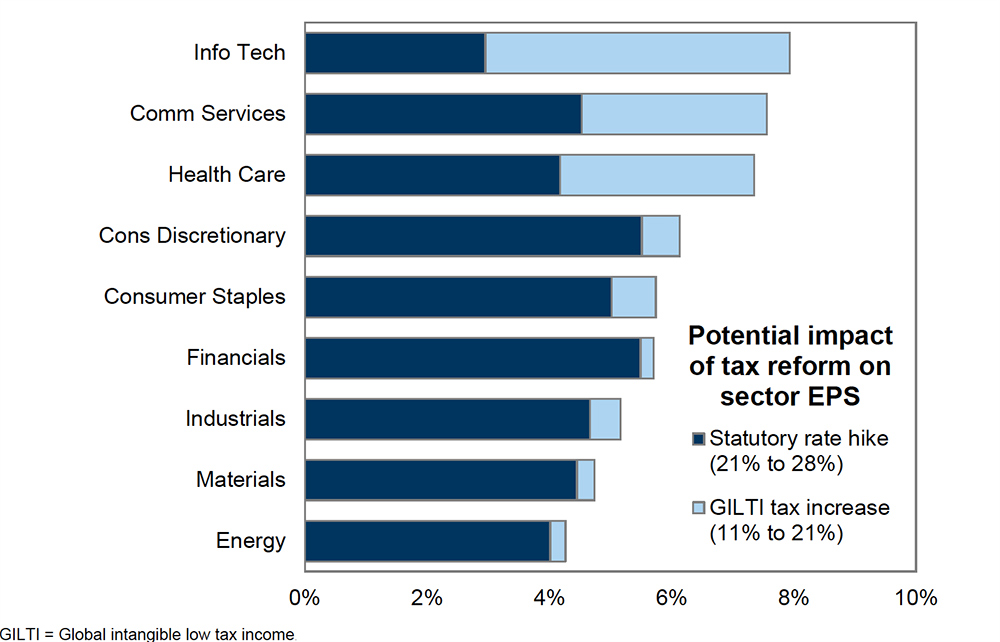

高盛认为,未来几年,信息技术、医疗、通信服务和非必需消费品等行业的每股收益受加税影响最大。如下图所示,能源和金融行业受到的影响较小:

万能的美元

美元是可能刺激股市上涨的第三个因素。外汇市场对于外交政策转变和高层的变动高度敏感。

高盛的外汇分析师在写给投资者的最新一期《选举手册》(Election Playbook)报告中指出:“我们认为,如果前副总统拜登当选,并且民主党在参议院获胜,这种‘民主党完胜’的情景会加快美元贬值。”他们认为增加政府支出、加征公司税和恢复全球自由贸易,会对美元产生影响。

弱美元将降低出口成本,使美国跨国公司在全球贸易中占有更大竞争优势,从而大幅增加公司收入。

高盛的分析师写道:“我们现在不会推荐新的美元做空策略,因为我们要等待更多信息,以分析总统的健康状况对大选的影响。但我们认为,美元当前的水平相对具有吸引力,可以体现我们积极的周期性观点,特别是在民调显示拜登依旧遥遥领先的情况下。”

大惊喜!

9月2日,标普500指数下跌至3,281.06点,距离2020年的盈亏平衡点不超过百分之一。当天市场收盘后,我的收件箱里塞满了各种历史数据分析,这些分析报告研究了每四年,华尔街在总统大选前两个月的糟糕表现。这些分析传达出的信息很明确:历史告诉我们要套现,等到美国选出总统之后再说。

但从现在的情况来看,那是非常糟糕的做法。9月2日之后,标普500指数上涨了6.5%(截至10月8日收盘),而且VIX指数显示,市场波动性也表现出好的迹象。

但亲爱的读者朋友们,现在还是10月。没有任何规矩说每次大选只能有一次“10月惊奇”。在大选日之前任何事情都可能发生。

对冲基金Hercules Investments的首席执行官詹姆斯•麦克唐纳德告诉《财富》杂志:“我们现在必须设想美国总统大选的各种情景。我最大胆的设想是如果乔•拜登也感染了新冠病毒怎么办。”(财富中文网)

翻译:刘进龙

审校:汪皓

一场颇具争议的总统大选可能演变成严重宪法危机。第三波新冠疫情来袭。经济刺激救助计划在华盛顿陷入僵局。

进入10月,在2020年最后一个季度的开端,这些问题成为笼罩在市场上空的阴影。资深投资者或许想要避开第四季度,这是可以理解的,因为这是总统大选年常用的投资策略。

然而,今年的情形不同寻常。10月第一周,纳斯达克和标普500指数都上涨了2.2%,股市的涨幅足以收回整个9月的损失,这也符合今年让人完全无法预测的局势。

到底出了什么问题?

你可以把它称作提前到来的“10月惊奇”,而且它可能会持续影响未来四年甚至更长时间。

美国总统特朗普新冠肺炎检测呈阳性,可能打乱了他的连任计划,但却对市场产生了积极影响。从那一刻开始,乔•拜登巩固了自己在民调中的领先优势,提高了当选的几率,而华尔街和投资者开始思考一位民主党总统入主白宫和民主党在国会大胜之后,其投资组合的表现。

投资公司BMO Capital Markets 的债券分析师伊恩•林根上周在一篇投资者报告中写道:“拜登当选的几率持续上升,民主党在国会完胜的可能性也在提高。如果说最近投资高风险资产有任何指导意义的话,那么这种不可测事件对于国内股票市场的影响绝对是积极的。”

通常情况下,华尔街并不喜欢华盛顿被一党控制。其实,华尔街更倾向坚持低税率和解除监管的共和党人入主白宫。这种渴望情绪根深蒂固,即便历史数据并不支持这样的偏执。

为什么华尔街喜欢分裂的华盛顿(从1950年至今,在白宫与国会分属不同党派的年份,股票市场的年收益率更高。总体而言,民主党总统执政时期GDP增幅更大。)资料来源:LPL RESEARCH

但今年的故事情节发生了反转。面对明年1月华盛顿可能被民主党绝对掌控的情景,华尔街不仅表现地非常平静,甚至有些乐见其成。

支出和税收

如果拜登当选,意味着2021年之后政府可能要加税,但越来越多华尔街分析师认为,拜登当选利大于弊。

高盛(Goldman)的首席经济学家贾恩•哈奇乌斯上周对投资者说:“如果民主党完胜,我们可能会更新预期。因为1月20日总统就职典礼之后,政府很快通过至少2万亿美元财政刺激方案的可能性会大幅提升。之后,政府可能会增加在基础设施、气候、医疗和教育等领域的长期支出,至少可以抵消对企业和高收入者长期加税的影响。”

LPL Financial Research的副总裁兼市场策略师杰夫•布赫宾德同样认为不必担心民主党完胜。布赫宾德认为,拜登领导下的白宫通过大规模消费刺激方案和终止特朗普时代的贸易战,是美国企业界的福音,能够抵消民主党加税的负面影响。LPL公司的计算显示,对于企业收入最有利的情况是恢复自由贸易和不加税。

布赫宾德表示,拜登加税可能使公司收入减少10%(高盛计算的结果为9%),但取消对中国和欧洲等美国主要贸易伙伴的关税可以提高每股收益,两者能够相抵。

基于不同情景的每股收益共同预估(标普500公司的营收预计明年将普遍上涨。如果没有特朗普总统的对华贸易关税和乔•拜登提出的加税,美国公司的利润会有更大幅增长。)资料来源:LPL RESEARCH,STRATEGAS,FACTSET 09/08/20

另外,值得注意的是,分析师都认为拜登的加税计划在被签署成法律之前会大打折扣。班森集团(Bahnsen Group)的创始人及执行合伙人戴维•班森告诉《财富》杂志:“美国历史上没有一位总统在竞选中提出的税收计划能够丝毫不差地变成税法。从来没有。”

尽管如此,我们依旧需要分析哪些行业最后可能会受到拜登税收计划的影响。与任何新税收计划一样,总有人会获利,有人会蒙受损失。

高盛认为,未来几年,信息技术、医疗、通信服务和非必需消费品等行业的每股收益受加税影响最大。如下图所示,能源和金融行业受到的影响较小:

税收改革对行业每股收益的潜在影响

万能的美元

美元是可能刺激股市上涨的第三个因素。外汇市场对于外交政策转变和高层的变动高度敏感。

高盛的外汇分析师在写给投资者的最新一期《选举手册》(Election Playbook)报告中指出:“我们认为,如果前副总统拜登当选,并且民主党在参议院获胜,这种‘民主党完胜’的情景会加快美元贬值。”他们认为增加政府支出、加征公司税和恢复全球自由贸易,会对美元产生影响。

弱美元将降低出口成本,使美国跨国公司在全球贸易中占有更大竞争优势,从而大幅增加公司收入。

高盛的分析师写道:“我们现在不会推荐新的美元做空策略,因为我们要等待更多信息,以分析总统的健康状况对大选的影响。但我们认为,美元当前的水平相对具有吸引力,可以体现我们积极的周期性观点,特别是在民调显示拜登依旧遥遥领先的情况下。”

大惊喜!

9月2日,标普500指数下跌至3,281.06点,距离2020年的盈亏平衡点不超过百分之一。当天市场收盘后,我的收件箱里塞满了各种历史数据分析,这些分析报告研究了每四年,华尔街在总统大选前两个月的糟糕表现。这些分析传达出的信息很明确:历史告诉我们要套现,等到美国选出总统之后再说。

但从现在的情况来看,那是非常糟糕的做法。9月2日之后,标普500指数上涨了6.5%(截至10月8日收盘),而且VIX指数显示,市场波动性也表现出好的迹象。

但亲爱的读者朋友们,现在还是10月。没有任何规矩说每次大选只能有一次“10月惊奇”。在大选日之前任何事情都可能发生。

对冲基金Hercules Investments的首席执行官詹姆斯•麦克唐纳德告诉《财富》杂志:“我们现在必须设想美国总统大选的各种情景。我最大胆的设想是如果乔•拜登也感染了新冠病毒怎么办。”(财富中文网)

翻译:刘进龙

审校:汪皓

A disputed election that could devolve into a full-blown constitutional crisis. A COVID third wave. A stimulus rescue package that bogs down in Washington.

As the calendar flipped to October, the start of the final quarter of 2020, these clouds hung thick and dark over the markets. Veteran investors could be excused for wanting to take the fourth quarter off, a common strategy in a presidential election year.

But something unusual happened. In keeping with this completely unpredictable year, the markets rallied, with the Nasdaq and S&P 500 both climbing 2.2% in the first week of October, enough to just about recoup all of September's losses.

What gives?

You can call it an October surprise that came early, and one that may have a enduring impact for the next four years, and beyond.

President Trump’s positive COVID-19 diagnosis may have thrown his re-election bid into turmoil, but it has had the opposite effect on the markets. From that point on, Joe Biden’s lead in the polls and election odds solidified, and Wall Street and investors started to come to grips with how their portfolios would perform with, gasp, a Democrat in the White House, and a blue sweep overtaking Congress.

“The odds of a Biden victory continue to rise, as do the chances of a blue sweep," Ian Lyngen, a BMO Capital Markets bond analyst, wrote last week in an investors note. "And if the recent bid for risk assets is any guide, such an eventuality could prove a decidedly positive event for domestic equities.”

Ordinarily, Wall Street hates one-party control. And, if anything, it usually prefers a low-tax, regulation-busting Republican in the Oval Office. That anxiety runs deep, even if the historical data doesn't quite back up the paranoia.

But this year, the script has flipped. Wall Street is not only unperturbed by the prospect of Washington awash in blue come January, it sees a possible upside.

Spending and taxes

Yes, a Biden presidency would likely mean a tax hike at some point after 2021, but, all in all, the pros outweigh the cons, a growing chorus of Wall Street analysts say.

"A blue wave would likely prompt us to upgrade our forecasts," Goldman's chief economist, Jan Hatzius, told investors last week. "The reason is that it would sharply raise the probability of a fiscal stimulus package of at least $2 trillion shortly after the presidential inauguration on January 20, followed by longer-term spending increases on infrastructure, climate, health care and education that would at least match the likely longer-term tax increases on corporations and upper-income earners."

Jeff Buchbinder echoes that fear-not message. Buchbinder, vice president and market strategist at LPL Financial Research, sees the addition of a big fat stimulus spending package from a Biden-led White House plus the removal of the Trump era trade wars as two tailwinds for Corporate America that could just about offset the negative hit brought on from a Democrat-led tax rate hike. The best scenario for corporate earnings would be a return to free trade and no new taxes, as LPL's calculation here shows.

Still, Buchbinder figures the 10% hit (Goldman calculates it at an 9% hit) to corporate earnings that you'd see from a Biden tax hike matches the EPS boost you'd get from removing tariffs from America's top trading partners in China and Europe.

And, it should be noted, the consensus is that a Biden tax hike would be watered down before it gets signed into law. "Not a single President in American history has had a tax plan in their campaign that then got photocopied and became a tax law. Ever,” David Bahnsen, founder and managing partner of the Bahnsen Group, tells Fortune.

Even still, it's time to look at which sectors would be most exposed to Biden's tax proposal. As is is the case with any new tax plan, there will be winners and losers.

According to Goldman Sachs, the following sectors—information technology, health care, communications services and consumer discretionary—could see the biggest EPS hits from a tax rate hike in the years to come. Energy and financials would be less exposed, as the following Goldman chart shows:

The almighty dollar

There's a third factor that could add rocket fuel to a stocks rally: the dollar. The FX markets are highly sensitive to shifts in foreign policy, and to changes at the top.

"A 'blue wave' scenario—where former Vice President Biden wins the presidency and Democrats also take the Senate—should accelerate US Dollar weakness, in our view," Goldman Sachs FX analysts wrote in its latest "Election Playbook" report to investors. They see increased government spending, higher corporate taxes and a return to freer global trade as three factors that could weigh on the greenback.

And a weak dollar is a big stimulus for corporate earnings as it makes exports cheaper and gives American multinationals a competitive edge in global trade.

"We are holding off on recommending new Dollar shorts for now as we await more information on how the President’s health situation will affect the race," the Goldman analysts wrote. "But we view current levels as relatively attractive to express our positive cyclical views—especially if polling continues to indicate a sizable lead for Biden."

Surprise!

On Sept. 2, the S&P 500 slumped to 3,281.06, putting it within a few fractions of a percent of break-even for 2020. After the markets closed that day, my in-box filled up with all kinds of historical analyses how, every four years, Wall Street typically performs poorly in the two months prior to a presidential election. The message was clear: history says to move into cash, and wait it out until America elects a president.

As it stands now, that would have been an extraordinarily bad move. The S&P 500 is up 6.5% since then (as of the Oct. 8 close), and market volatility, as measured by the VIX index, is flashing a green light.

But, dear reader, this is still October. There's no rule saying only one October surprise per election cycle. Anything can still happen between now and Election Day.

"We must now run 'what-if' scenarios toward the U.S. presidential race," James McDonald is CEO of Hercules Investments, told Fortune. "My biggest 'what-if' is if Joe Biden contracts COVID-19, too."

请打开财富Plus APP