比特币价格一直被人为操纵,这可信吗?

SHAWN TULLY

2023-02-27

格里芬认为,在加密货币市场最动荡的时候,正常情况下会剧烈波动的比特币却能保持平和稳定,这种现象很符合有幕后推手在联手支撑和推高其价格的情况。

文本设置

文本设置

Plus(0条)

Plus(0条)

早在2017年,得克萨斯大学麦库姆斯商学院(University of Texas McCombs School of Business)的金融专业教授约翰·格里芬就发现了一种奇怪的现象。商学院的金融专业教授们通常在研究商业周期对大宗商品价格的影响,或美联储政策对利率期限结构的影响等课题。但格里芬的研究方向与他们截然不同。这位身高6英尺2英寸的前高中橄榄球明星认为自己是一位正义的十字军战士,是道德侦探。正如他对《财富》杂志所说,他“致力于揪出金融领域的坏人,给世界带来光明,曝光市场中的黑暗面”。金融大危机结束后,格里芬成了一位虔诚的基督徒。从此以后,他开始致力于开展公正的司法调查,挖掘从内幕交易到抵押贷款欺诈以及在金融危机期间篡改债券评级等不良行为,取得了非凡成就。

2017年,格里芬和阿明·夏姆斯在挖掘各种不良行为的时候,惊奇地发现一种应该与美元1∶1挂钩的代币,鲜为人知,却被大量发行。夏姆斯当时是麦库姆斯商学院的博士研究生,他也参加了格里芬的多项秘密调查。他们顺藤摸瓜,发现了另外一条线索:每当新一批这种代币出现时,比特币的价格似乎就会上涨。似乎某个人或者某个群体在利用这种新印发的“免费资金”,炒高比特币的价格,为自己牟利。他和夏姆斯详细分析了多达200G的交易数据,相当于史密森学会(Smithsonian Institution)两年收集的数据数量,两人还跟踪了250万个单独电子钱包的买卖交易。

2018年,他们共同发表了一篇突破性的研究报告。他们发现,有一个依旧无法确定身份的比特币“大户”,在2017年年底和2018年年初,通过扭曲比特币交易,几乎以一己之力推动了比特币的大幅上涨。

2022年底,又有一个神秘的趋势引起了格里芬的注意。虽然加密货币市场崩盘,并且受到其他各种负面因素的影响,但比特币价格每次跌破16,000美元,很快就会反弹,使比特币的交易价格始终维持在16,000美元至17,000美元之间。令人难以置信的是,进入2023年,加密货币市场持续崩溃,比特币的价格却逆势而行,自1月7日以来比特币价格上涨了35%,达到23,000美元。

格里芬对《财富》杂志表示:“这种现象非常可疑。目前的比特币市场依旧不真实,我们在2017年所见过的手段,现在可能仍在搅动市场。”

格里芬认为,在加密货币市场最动荡的时候,正常情况下会剧烈波动的比特币价格却能保持相对稳定,这种现象很符合有幕后推手在联手支撑和推高其价格的情况。格里芬补充道:“如果你是加密货币的幕后操纵者,你希望为自己的加密货币设定一个价格下限。当市场上出现大量负面情绪时,我们发现比特币存在一个牢不可破的价格下限,这非常可疑。”

虽然操纵市场的说法未能得到证实,但一些迹象却令人不安

值得注意的是,到目前为止没有确切的证据能证明有人在利用不良手段操纵比特币。格里芬说道:“现在比特币市场变得更加庞大,因此数据挖掘的难度增大。老练的市场参与者很善于隐藏自己的身份。”我们看到过一些可信的泄露信息,表明如果主要市场参与者担心,一位加密货币行业领袖计划采取他们认为鲁莽的、危及行业生存的举动,他们就会召集行业精英开会。但目前并没有证据能够证明,这些行业参与者曾开会协调购买比特币或其他加密货币。例如,众所周知,去年秋天早些时候,全球最大加密货币交易平台币安(Binance)的首席执行官赵长鹏(又被称为“CZ”)以及其他加密货币行业领导者认为,山姆·班克曼-弗莱德的对冲基金Alameda正在攻击当时几近崩溃的加密货币泰达币,而泰达币的可靠性对于整个行业的健康至关重要,因此媒体报道称他们建议弗莱德停手。(泰达币[代码USDT]也是格里芬和夏姆斯曝光的2017年至2018年市场操纵案的主要目标。)

目前加密货币领域的众多破产程序、诉讼和刑事调查中,或许能够曝出业内相互勾结、排外行为的证据。荷兰央行经济学家、跟踪比特币碳足迹的网站Digiconomist的经营者亚历克斯·德福里斯预测:“随着班克曼-弗莱德遭到指控,他可能供出其他市场参与者相互勾结的行径。”Genesis借贷业务的破产,令其母公司数字货币集团(Digital Currency Group)的老板巴里·希尔伯特与陷入困境的交易平台Gemini的联合创始人卡梅伦和泰勒·温克莱沃斯翻脸。温克莱沃斯兄弟称,数字货币集团欠款9亿美元,都是Gemini存款用户向支付高利息的Genesis项目出借的资金,并威胁起诉数字货币集团和希尔伯特,指控其采取恶意拖延战术,并否认数字货币集团的实际责任。简而言之,曾经的盟友对簿公堂,如果双方之间有任何秘密交易,可能会被公布于众。

格里芬并不是唯一一位对业内的不良行为保持警惕的知名观察者。欧洲央行(European Central Bank)市场业务总干事乌尔里克·宾德赛尔和欧洲央行顾问于尔根·沙夫在11月30日发表了一篇名为《比特币的最后一站》(Bitcoin’s Last Stand)的长文,认为比特币的再次兴起是“人为操纵的回光返照,比特币已经走上末路”。两位华尔街的重要人物对笔者解释该篇文章的背景称,比特币的价格波动没有受到大量坏消息的影响,这种情况看起来并不真实,与由独立卖家和买家左右的正常自由市场截然不同。

比特币在负面市场情绪中表现出惊人的稳定性

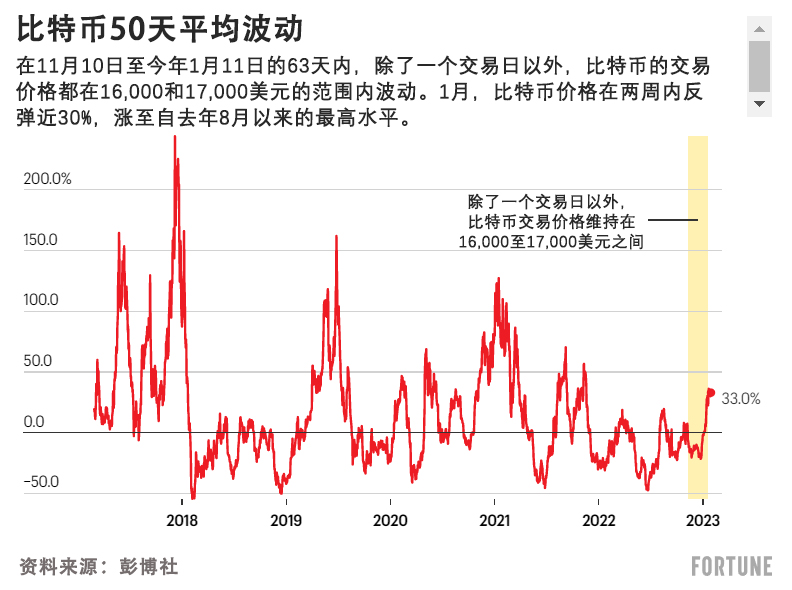

有一个重要的标志表明,比特币从协调买入行动中受益:其惊人的稳定表现,在似乎会冲击主要加密货币的FTX破产事件后,为比特币价格暴涨至五个月新高奠定了基础。从去年11月5日,也就是关于FTX的报道广为流传的前一天,到11月9日,比特币价格(按成交价计算)从21,300美元下跌到15,900美元,跌至自2020年年末以来的最低水平,跌幅达25%。之后按照比特币的标准,这种正常情况下会失控的加密货币表现却趋于稳定。从去年11月10日到今年1月11日的62天内,除了一个交易日以外,比特币的交易价格都在16,000和17,000美元的范围内波动。从去年11月22日至今年1月11日的50天内,比特币的成交价格一直在一个较小的区间内波动,最低为16,200美元,最高为17,900美元,相差10%。

委婉地说,比特币超级顺利的行情最开始的时候就非比寻常。《财富》数据编辑斯科特·德卡罗详细分析发现,自2017年初以来,在40个连续50天的期限内,比特币的价格波动幅度从未低于19%,在四个七周期限内,有三个期限的波动幅度超过30%。从低位到高位的中位数波动幅度为44%。因此,在FTX引发的混乱最高潮时,比特币价格却经历了最小幅度的波动,从低位到高位的差距只有过去六年平均水平的四分之一至五分之一。

从今年1月12日至24日,比特币价格开始了匪夷所思的大幅上涨。在这段时间,比特币价格从17,035美元上涨至23,000美元,涨至自去年8月以来的最高水平,涨幅高达28%,远高于FTX引起的恐慌开始蔓延时的价格。而在此期间,加密货币市场经历了去年11月28日贷款机构BlockFi破产;去年12月21日最大上市挖矿公司之一Core Scientific破产;以及一个月后的Genesis贷款业务破产。

你可能认为,与比特币有关的混乱会动摇小型投资者和机构对加密货币的信心,从而带来严重的抛售压力,并导致价格暴跌。事实上,在FTX破产之后,社交媒体上出现了大量有关比特币的严重负面情绪。交易活动大幅减少,表明投资者的热情正在消退。Coinbase第四季度的交易量远低于第三季度,较第一季度下跌了52%。

对于比特币的稳健表现,是否还有其他解释?有多位关注加密货币日常交易的专家认为,所谓人为推高比特币价格的阴谋并不存在,比特币价格稳定的原因是市场运转良好。区块链分析提供商Nansen的研究员安德鲁·瑟曼表示:“我并没有发现内幕交易的阴谋。众所周知,比特币的价格波动具有周期性。”最好的解释通常是最无聊的解释。对比特币价格上涨最好的解释是,因为买家的数量超过卖家的数量。假如Celsius和FTX等破产的公司出售比特币,并且为了支持自己的加密货币而打压比特币的价格。”挪威加密货币数据分析公司Arcane Research的高级分析师维特尔·伦德认同这种观点。“我没有发现有一群人正在支撑比特币的价格。现在我们处于一种平衡的动态变化当中。FTX破产之后的被迫出售在某种程度上已经被市场吸纳,我们没有看到更多被迫出售。”这种现象使比特币价格近期反弹至超过23,000美元。

但毫无疑问,比特币在FTX破产后的稳健表现,尤其是其最近的上涨,对于收入与比特币价格息息相关的企业而言,是天大的好消息。在FTX破产后的几天内,加密货币交易平台、挖矿公司和贷款机构的股价全线下跌。但Riot、Marathon和Bitfarms等挖矿公司的股价在12月跌至两年最低水平之后,截至1月27日已经分别上涨了92%、150%和189%。全球最大的加密货币交易平台之一Coinbase从新年前的低谷上涨85%,其市值增加了70亿美元。Riot和Bitfarms都已经反弹到接近于FTX破产之前的水平。

有一家最渴望得到刺激的公司获得了巨大的好处。它就是综合软件提供商和比特币投机商MicroStrategy公司。该公司的联合创始人兼执行董事长迈克尔·塞勒负债24亿美元购买比特币,在去年11月11日比特币价格跌破16,000美元时,其所欠的借款总额已经远远超过他所持有的比特币的价值。如果比特币持续下跌,MicroStrategy会面临大麻烦。但比特币价格反弹帮助MicroStrategy摆脱了困境,其股价从去年11月中旬的166美元上涨到1月27日的258美元,涨幅高达55%。

与几乎任何其他金融领域相比,加密货币行业的空间更小。决定大型加密货币企业盈利还是陷入破产的因素是比特币的价格,而比特币价格作为基准,反过来会左右其他加密货币的价格波动。加密货币行业有很大一部分已经受到严重冲击。由于FTX破产动摇了加密货币行业脆弱的基础,如果比特币不能找到适当的基础,还会有更多加密货币的支持者倒下。

格里芬和夏姆斯在2017年至2018年的调查结果对今天的意义

格里芬和夏姆斯对2017年至2018年比特币泡沫背后的因素所做的研究,为我们分析FTX破产之后出售比特币的策略提供了指导。夏姆斯现任俄亥俄州费舍尔商学院(Fisher College of Business)教授。格里芬和夏姆斯最早在2018年发表了118页的报告,并于两年后在著名的同行审议期刊《金融杂志》(Journal of Finance)上发表。

两人警告表明市场上可能存在人为操纵行为的证据之一,是与泰达币密切相关的大型交易平台Bitfinex对这种所谓稳定币没有做到透明。格里芬回忆说:“我们发现有许多博客怀疑Bitfinex没有为这种加密货币提供全额担保。”他说道:“如果有人通过发行没有法定货币担保的泰达币来增加资金,就会引发比特币泡沫。这是一种假设。”

格里芬和夏姆斯发现,有两种做法刺激了比特币的突然大幅上涨。第一种是大量新发行的加密货币,使欺诈者获得了炒作比特币的货币。第二种是目前最流行的做法,那就是一位或多位操纵者合谋,每次比特币下跌到目标价位时,他们就会出面将比特币的价格推高到基准水平以上。

他们发现比特币价格呈现出一种非常明显的可疑模式。如果比特币价格下跌,并且市场上出现了大量新发行的泰达币,这时比特币就会迎来最大幅度上涨。当时的情况与目前一样,泰达币是最重要的“稳定币”,或者应该与法定货币储备一比一挂钩的加密货币。泰达币实际上是美元的替代者;每一枚泰达币都应该与一张等额的美元法定货币挂钩。泰达币的发行方是来自中国香港的iFinex公司的分支机构,该公司还拥有当时全球最大的交易平台Bitfinex。

格里芬和夏姆斯重点研究了2017年3月初至2018年3月底之间1%的一小时区间,在这些时段,Bitfinex大量发行泰达币和另外两个交易平台Bittrex与Poloniex大量买入比特币的情况最多。在每个时段开始之前,比特币价格都面临压力。但在每一个时段似乎都有一位大买家救场,在60分钟结束前使比特币的价格大幅上涨。这些“大户”用泰达币买入比特币,使比特币的价格暴涨,但他们的身份至今仍是个谜。夏姆斯回忆说:“我们发现了一种常见的价格趋势大幅度逆转的规律。”

在13个月内的95个一小时时段中,接近60%的比特币价格大幅上涨,其原因都是泰达币和比特币的大量流入。

夏姆斯表示:“泰达币被作为交易比特币和其他加密货币的现金。”虽然泰达币的市值与比特币相比不值一提,其交易量却高于比特币。考虑到泰达币在交易中的重要性,通过无担保发行泰达币注入“新资金”的做法,就像美联储超量印发美钞一样。格里芬对《财富》杂志表示:“在比特币供应量不变的情况下,无担保发行泰达币会增加追逐比特币的货币量。凭空发行的泰达币推高了比特币和其他加密货币的价格。”

大户获得新发行的泰达币后,就会在Bittrex和Poloniex上用这些泰达币交易大量比特币。大量买入比特币逆转了其价格下跌趋势,使价格远高于开始下跌之前的水平。研究称:“大户要么展现出好像能够洞悉未来一样预测市场时机的能力,或者对比特币价格产生了极其巨大的影响。”格里芬表示,现在看来,可以确定在比特币繁荣时期,泰达币并未持有充足的货币储备,因此“几乎可以确定,凭空出现的资金会推高价格。”

报告发表以后,Tether有限公司(Tether Ltd.)坚称该报告的结论存在缺陷,并表示泰达币不可能被用于推高比特币价格。但商品期货交易委员会(Commodity Futures Trading Commission)的调查却得出了相反的结论。2021年10月,商品期货交易委员会获得Tether公司及其所有人支付的4,100万美元和解金,原因是其并没有像宣传的那样将泰达币与美元挂钩。商品期货交易委员会发现“从2016年到2018年的26个月内,Tether公司仅有27.6%的时间有足够的美元储备……作为流通中的泰达币的担保”,并且“将储备资金与Bitfinex的经营和客户资金混为一谈。”格里芬表示:“比特币和泰达币不能用于买车和披萨等商品,只能用于购买加密货币。因此在这个封闭的系统中,在凭空发行新代币的刺激下,即使相对少量的操纵买入,也可能导致比特币价格大幅上涨。”

大户设定并不断提高价格下限

两位作者还发现,大规模购买比特币的行为,通常发生在比特币价格达到特定门槛时,比如略低于500美元的倍数。格里芬表示:“我们发现在达到这些门槛时购买比特币的情况大幅增多。大户不断设定并且提高价格下限。它并不是一个俱乐部,而是一家实体。当大户将比特币价格维持在门槛水平时,在外人看来比特币在这些价位是安全的。基金和小客户就会安心购买比特币,从而进一步推高比特币的价格。”夏姆斯表示:“当比特币维持在整数价位左右时,我们发现交易活动会推高价格。”

格里芬怀疑目前加密货币市场仍存在类似的做法。他表示,共谋支撑比特币的价格意味着,有一帮买家同意当价格接近下限时共同买入。假设这个价格下限就是16,000美元,因为在比特币价格极其稳定的这段时期,其价格几乎总是维持在这个价位。例如,如果出现大规模卖出,导致比特币价格可能跌破16,000美元,大户俱乐部就会集体入场。格里芬说道:“例如,16,000美元可能作为一个协调机制。”操纵者可以将价格推高到接近17,000美元,然后通过多次小笔交易卖掉部分收获,不会引起市场波动。他们通过操纵价格在16,000美元至17,000美元之间上下波动,可以获得丰厚利润。

随着人们日益确信比特币不会跌破16,000美元,将会有更多投机者加入购买比特币。之后,操纵者们就会约定将新的价格下限设定为18,000美元。格里芬表示:“在加密货币领域,一群市场操纵者可以推高比特币价格下限,除非出现有实力的一方采取截然不同的操作。”但做空比特币的难度,远高于做空股票或债券。我们没有发现任何证据表明,有另外一群人正在压低比特币的价格,这让任何做多比特币的投资者都更有优势。格里芬表示:“比特币市场的大多数参与者都有维持价格下限的强烈动机。”

格里芬总结称,他与夏姆斯的研究表明,有确切的证据证明在2017年和2018年存在市场操纵行为,并且有一个人在幕后操控这一切。他说道:“现在我们没有进行具体分析。如果存在共谋的行径,在某些故事中可能会暴露出真相。”他说道,我们得到的启示是“比特币市场依旧特别容易被人为操纵。”

事实上,在FTX破产之后,比特币的表现已经令人惊奇。或许已经到了令人难以相信的地步。(财富中文网)

译者:刘进龙

审校:汪皓

早在2017年,得克萨斯大学麦库姆斯商学院(University of Texas McCombs School of Business)的金融专业教授约翰·格里芬就发现了一种奇怪的现象。商学院的金融专业教授们通常在研究商业周期对大宗商品价格的影响,或美联储政策对利率期限结构的影响等课题。但格里芬的研究方向与他们截然不同。这位身高6英尺2英寸的前高中橄榄球明星认为自己是一位正义的十字军战士,是道德侦探。正如他对《财富》杂志所说,他“致力于揪出金融领域的坏人,给世界带来光明,曝光市场中的黑暗面”。金融大危机结束后,格里芬成了一位虔诚的基督徒。从此以后,他开始致力于开展公正的司法调查,挖掘从内幕交易到抵押贷款欺诈以及在金融危机期间篡改债券评级等不良行为,取得了非凡成就。

2017年,格里芬和阿明·夏姆斯在挖掘各种不良行为的时候,惊奇地发现一种应该与美元1∶1挂钩的代币,鲜为人知,却被大量发行。夏姆斯当时是麦库姆斯商学院的博士研究生,他也参加了格里芬的多项秘密调查。他们顺藤摸瓜,发现了另外一条线索:每当新一批这种代币出现时,比特币的价格似乎就会上涨。似乎某个人或者某个群体在利用这种新印发的“免费资金”,炒高比特币的价格,为自己牟利。他和夏姆斯详细分析了多达200G的交易数据,相当于史密森学会(Smithsonian Institution)两年收集的数据数量,两人还跟踪了250万个单独电子钱包的买卖交易。

2018年,他们共同发表了一篇突破性的研究报告。他们发现,有一个依旧无法确定身份的比特币“大户”,在2017年年底和2018年年初,通过扭曲比特币交易,几乎以一己之力推动了比特币的大幅上涨。

2022年底,又有一个神秘的趋势引起了格里芬的注意。虽然加密货币市场崩盘,并且受到其他各种负面因素的影响,但比特币价格每次跌破16,000美元,很快就会反弹,使比特币的交易价格始终维持在16,000美元至17,000美元之间。令人难以置信的是,进入2023年,加密货币市场持续崩溃,比特币的价格却逆势而行,自1月7日以来比特币价格上涨了35%,达到23,000美元。

格里芬对《财富》杂志表示:“这种现象非常可疑。目前的比特币市场依旧不真实,我们在2017年所见过的手段,现在可能仍在搅动市场。”

格里芬认为,在加密货币市场最动荡的时候,正常情况下会剧烈波动的比特币价格却能保持相对稳定,这种现象很符合有幕后推手在联手支撑和推高其价格的情况。格里芬补充道:“如果你是加密货币的幕后操纵者,你希望为自己的加密货币设定一个价格下限。当市场上出现大量负面情绪时,我们发现比特币存在一个牢不可破的价格下限,这非常可疑。”

虽然操纵市场的说法未能得到证实,但一些迹象却令人不安

值得注意的是,到目前为止没有确切的证据能证明有人在利用不良手段操纵比特币。格里芬说道:“现在比特币市场变得更加庞大,因此数据挖掘的难度增大。老练的市场参与者很善于隐藏自己的身份。”我们看到过一些可信的泄露信息,表明如果主要市场参与者担心,一位加密货币行业领袖计划采取他们认为鲁莽的、危及行业生存的举动,他们就会召集行业精英开会。但目前并没有证据能够证明,这些行业参与者曾开会协调购买比特币或其他加密货币。例如,众所周知,去年秋天早些时候,全球最大加密货币交易平台币安(Binance)的首席执行官赵长鹏(又被称为“CZ”)以及其他加密货币行业领导者认为,山姆·班克曼-弗莱德的对冲基金Alameda正在攻击当时几近崩溃的加密货币泰达币,而泰达币的可靠性对于整个行业的健康至关重要,因此媒体报道称他们建议弗莱德停手。(泰达币[代码USDT]也是格里芬和夏姆斯曝光的2017年至2018年市场操纵案的主要目标。)

目前加密货币领域的众多破产程序、诉讼和刑事调查中,或许能够曝出业内相互勾结、排外行为的证据。荷兰央行经济学家、跟踪比特币碳足迹的网站Digiconomist的经营者亚历克斯·德福里斯预测:“随着班克曼-弗莱德遭到指控,他可能供出其他市场参与者相互勾结的行径。”Genesis借贷业务的破产,令其母公司数字货币集团(Digital Currency Group)的老板巴里·希尔伯特与陷入困境的交易平台Gemini的联合创始人卡梅伦和泰勒·温克莱沃斯翻脸。温克莱沃斯兄弟称,数字货币集团欠款9亿美元,都是Gemini存款用户向支付高利息的Genesis项目出借的资金,并威胁起诉数字货币集团和希尔伯特,指控其采取恶意拖延战术,并否认数字货币集团的实际责任。简而言之,曾经的盟友对簿公堂,如果双方之间有任何秘密交易,可能会被公布于众。

格里芬并不是唯一一位对业内的不良行为保持警惕的知名观察者。欧洲央行(European Central Bank)市场业务总干事乌尔里克·宾德赛尔和欧洲央行顾问于尔根·沙夫在11月30日发表了一篇名为《比特币的最后一站》(Bitcoin’s Last Stand)的长文,认为比特币的再次兴起是“人为操纵的回光返照,比特币已经走上末路”。两位华尔街的重要人物对笔者解释该篇文章的背景称,比特币的价格波动没有受到大量坏消息的影响,这种情况看起来并不真实,与由独立卖家和买家左右的正常自由市场截然不同。

比特币在负面市场情绪中表现出惊人的稳定性

有一个重要的标志表明,比特币从协调买入行动中受益:其惊人的稳定表现,在似乎会冲击主要加密货币的FTX破产事件后,为比特币价格暴涨至五个月新高奠定了基础。从去年11月5日,也就是关于FTX的报道广为流传的前一天,到11月9日,比特币价格(按成交价计算)从21,300美元下跌到15,900美元,跌至自2020年年末以来的最低水平,跌幅达25%。之后按照比特币的标准,这种正常情况下会失控的加密货币表现却趋于稳定。从去年11月10日到今年1月11日的62天内,除了一个交易日以外,比特币的交易价格都在16,000和17,000美元的范围内波动。从去年11月22日至今年1月11日的50天内,比特币的成交价格一直在一个较小的区间内波动,最低为16,200美元,最高为17,900美元,相差10%。

委婉地说,比特币超级顺利的行情最开始的时候就非比寻常。《财富》数据编辑斯科特·德卡罗详细分析发现,自2017年初以来,在40个连续50天的期限内,比特币的价格波动幅度从未低于19%,在四个七周期限内,有三个期限的波动幅度超过30%。从低位到高位的中位数波动幅度为44%。因此,在FTX引发的混乱最高潮时,比特币价格却经历了最小幅度的波动,从低位到高位的差距只有过去六年平均水平的四分之一至五分之一。

从今年1月12日至24日,比特币价格开始了匪夷所思的大幅上涨。在这段时间,比特币价格从17,035美元上涨至23,000美元,涨至自去年8月以来的最高水平,涨幅高达28%,远高于FTX引起的恐慌开始蔓延时的价格。而在此期间,加密货币市场经历了去年11月28日贷款机构BlockFi破产;去年12月21日最大上市挖矿公司之一Core Scientific破产;以及一个月后的Genesis贷款业务破产。

你可能认为,与比特币有关的混乱会动摇小型投资者和机构对加密货币的信心,从而带来严重的抛售压力,并导致价格暴跌。事实上,在FTX破产之后,社交媒体上出现了大量有关比特币的严重负面情绪。交易活动大幅减少,表明投资者的热情正在消退。Coinbase第四季度的交易量远低于第三季度,较第一季度下跌了52%。

对于比特币的稳健表现,是否还有其他解释?有多位关注加密货币日常交易的专家认为,所谓人为推高比特币价格的阴谋并不存在,比特币价格稳定的原因是市场运转良好。区块链分析提供商Nansen的研究员安德鲁·瑟曼表示:“我并没有发现内幕交易的阴谋。众所周知,比特币的价格波动具有周期性。”最好的解释通常是最无聊的解释。对比特币价格上涨最好的解释是,因为买家的数量超过卖家的数量。假如Celsius和FTX等破产的公司出售比特币,并且为了支持自己的加密货币而打压比特币的价格。”挪威加密货币数据分析公司Arcane Research的高级分析师维特尔·伦德认同这种观点。“我没有发现有一群人正在支撑比特币的价格。现在我们处于一种平衡的动态变化当中。FTX破产之后的被迫出售在某种程度上已经被市场吸纳,我们没有看到更多被迫出售。”这种现象使比特币价格近期反弹至超过23,000美元。

但毫无疑问,比特币在FTX破产后的稳健表现,尤其是其最近的上涨,对于收入与比特币价格息息相关的企业而言,是天大的好消息。在FTX破产后的几天内,加密货币交易平台、挖矿公司和贷款机构的股价全线下跌。但Riot、Marathon和Bitfarms等挖矿公司的股价在12月跌至两年最低水平之后,截至1月27日已经分别上涨了92%、150%和189%。全球最大的加密货币交易平台之一Coinbase从新年前的低谷上涨85%,其市值增加了70亿美元。Riot和Bitfarms都已经反弹到接近于FTX破产之前的水平。

有一家最渴望得到刺激的公司获得了巨大的好处。它就是综合软件提供商和比特币投机商MicroStrategy公司。该公司的联合创始人兼执行董事长迈克尔·塞勒负债24亿美元购买比特币,在去年11月11日比特币价格跌破16,000美元时,其所欠的借款总额已经远远超过他所持有的比特币的价值。如果比特币持续下跌,MicroStrategy会面临大麻烦。但比特币价格反弹帮助MicroStrategy摆脱了困境,其股价从去年11月中旬的166美元上涨到1月27日的258美元,涨幅高达55%。

与几乎任何其他金融领域相比,加密货币行业的空间更小。决定大型加密货币企业盈利还是陷入破产的因素是比特币的价格,而比特币价格作为基准,反过来会左右其他加密货币的价格波动。加密货币行业有很大一部分已经受到严重冲击。由于FTX破产动摇了加密货币行业脆弱的基础,如果比特币不能找到适当的基础,还会有更多加密货币的支持者倒下。

格里芬和夏姆斯在2017年至2018年的调查结果对今天的意义

格里芬和夏姆斯对2017年至2018年比特币泡沫背后的因素所做的研究,为我们分析FTX破产之后出售比特币的策略提供了指导。夏姆斯现任俄亥俄州费舍尔商学院(Fisher College of Business)教授。格里芬和夏姆斯最早在2018年发表了118页的报告,并于两年后在著名的同行审议期刊《金融杂志》(Journal of Finance)上发表。

两人警告表明市场上可能存在人为操纵行为的证据之一,是与泰达币密切相关的大型交易平台Bitfinex对这种所谓稳定币没有做到透明。格里芬回忆说:“我们发现有许多博客怀疑Bitfinex没有为这种加密货币提供全额担保。”他说道:“如果有人通过发行没有法定货币担保的泰达币来增加资金,就会引发比特币泡沫。这是一种假设。”

格里芬和夏姆斯发现,有两种做法刺激了比特币的突然大幅上涨。第一种是大量新发行的加密货币,使欺诈者获得了炒作比特币的货币。第二种是目前最流行的做法,那就是一位或多位操纵者合谋,每次比特币下跌到目标价位时,他们就会出面将比特币的价格推高到基准水平以上。

他们发现比特币价格呈现出一种非常明显的可疑模式。如果比特币价格下跌,并且市场上出现了大量新发行的泰达币,这时比特币就会迎来最大幅度上涨。当时的情况与目前一样,泰达币是最重要的“稳定币”,或者应该与法定货币储备一比一挂钩的加密货币。泰达币实际上是美元的替代者;每一枚泰达币都应该与一张等额的美元法定货币挂钩。泰达币的发行方是来自中国香港的iFinex公司的分支机构,该公司还拥有当时全球最大的交易平台Bitfinex。

格里芬和夏姆斯重点研究了2017年3月初至2018年3月底之间1%的一小时区间,在这些时段,Bitfinex大量发行泰达币和另外两个交易平台Bittrex与Poloniex大量买入比特币的情况最多。在每个时段开始之前,比特币价格都面临压力。但在每一个时段似乎都有一位大买家救场,在60分钟结束前使比特币的价格大幅上涨。这些“大户”用泰达币买入比特币,使比特币的价格暴涨,但他们的身份至今仍是个谜。夏姆斯回忆说:“我们发现了一种常见的价格趋势大幅度逆转的规律。”

在13个月内的95个一小时时段中,接近60%的比特币价格大幅上涨,其原因都是泰达币和比特币的大量流入。

夏姆斯表示:“泰达币被作为交易比特币和其他加密货币的现金。”虽然泰达币的市值与比特币相比不值一提,其交易量却高于比特币。考虑到泰达币在交易中的重要性,通过无担保发行泰达币注入“新资金”的做法,就像美联储超量印发美钞一样。格里芬对《财富》杂志表示:“在比特币供应量不变的情况下,无担保发行泰达币会增加追逐比特币的货币量。凭空发行的泰达币推高了比特币和其他加密货币的价格。”

大户获得新发行的泰达币后,就会在Bittrex和Poloniex上用这些泰达币交易大量比特币。大量买入比特币逆转了其价格下跌趋势,使价格远高于开始下跌之前的水平。研究称:“大户要么展现出好像能够洞悉未来一样预测市场时机的能力,或者对比特币价格产生了极其巨大的影响。”格里芬表示,现在看来,可以确定在比特币繁荣时期,泰达币并未持有充足的货币储备,因此“几乎可以确定,凭空出现的资金会推高价格。”

报告发表以后,Tether有限公司(Tether Ltd.)坚称该报告的结论存在缺陷,并表示泰达币不可能被用于推高比特币价格。但商品期货交易委员会(Commodity Futures Trading Commission)的调查却得出了相反的结论。2021年10月,商品期货交易委员会获得Tether公司及其所有人支付的4,100万美元和解金,原因是其并没有像宣传的那样将泰达币与美元挂钩。商品期货交易委员会发现“从2016年到2018年的26个月内,Tether公司仅有27.6%的时间有足够的美元储备……作为流通中的泰达币的担保”,并且“将储备资金与Bitfinex的经营和客户资金混为一谈。”格里芬表示:“比特币和泰达币不能用于买车和披萨等商品,只能用于购买加密货币。因此在这个封闭的系统中,在凭空发行新代币的刺激下,即使相对少量的操纵买入,也可能导致比特币价格大幅上涨。”

大户设定并不断提高价格下限

两位作者还发现,大规模购买比特币的行为,通常发生在比特币价格达到特定门槛时,比如略低于500美元的倍数。格里芬表示:“我们发现在达到这些门槛时购买比特币的情况大幅增多。大户不断设定并且提高价格下限。它并不是一个俱乐部,而是一家实体。当大户将比特币价格维持在门槛水平时,在外人看来比特币在这些价位是安全的。基金和小客户就会安心购买比特币,从而进一步推高比特币的价格。”夏姆斯表示:“当比特币维持在整数价位左右时,我们发现交易活动会推高价格。”

格里芬怀疑目前加密货币市场仍存在类似的做法。他表示,共谋支撑比特币的价格意味着,有一帮买家同意当价格接近下限时共同买入。假设这个价格下限就是16,000美元,因为在比特币价格极其稳定的这段时期,其价格几乎总是维持在这个价位。例如,如果出现大规模卖出,导致比特币价格可能跌破16,000美元,大户俱乐部就会集体入场。格里芬说道:“例如,16,000美元可能作为一个协调机制。”操纵者可以将价格推高到接近17,000美元,然后通过多次小笔交易卖掉部分收获,不会引起市场波动。他们通过操纵价格在16,000美元至17,000美元之间上下波动,可以获得丰厚利润。

随着人们日益确信比特币不会跌破16,000美元,将会有更多投机者加入购买比特币。之后,操纵者们就会约定将新的价格下限设定为18,000美元。格里芬表示:“在加密货币领域,一群市场操纵者可以推高比特币价格下限,除非出现有实力的一方采取截然不同的操作。”但做空比特币的难度,远高于做空股票或债券。我们没有发现任何证据表明,有另外一群人正在压低比特币的价格,这让任何做多比特币的投资者都更有优势。格里芬表示:“比特币市场的大多数参与者都有维持价格下限的强烈动机。”

格里芬总结称,他与夏姆斯的研究表明,有确切的证据证明在2017年和2018年存在市场操纵行为,并且有一个人在幕后操控这一切。他说道:“现在我们没有进行具体分析。如果存在共谋的行径,在某些故事中可能会暴露出真相。”他说道,我们得到的启示是“比特币市场依旧特别容易被人为操纵。”

事实上,在FTX破产之后,比特币的表现已经令人惊奇。或许已经到了令人难以相信的地步。(财富中文网)

译者:刘进龙

审校:汪皓

Back in 2017, John Griffin, a professor of finance at the University of Texas McCombs School of Business, noticed something strange. Griffin follows a totally different beat from typical business school finance profs who explore, say, how business cycles influence commodity prices or Fed policy sways the term structure of interest rates. The 6-foot-2 former high school football star views himself as a crusader for good, a moral sleuth who, as he tells Fortune, “looks to expose financial evil, to shed light on the world and expose dark things in the markets.” After the Great Financial Crisis, Griffin became a devout Christian. He has since dedicated his distinguished career to righteous forensic digging that’s unearthed abuses ranging from insider trading to mortgage fraud to the doctoring of bond ratings during the financial crisis.

As Griffin and Amin Shams, then a doctoral candidate at McCombs who’s joined Griffin in several gumshoe investigations, screened for misdeeds in 2017, they were fascinated to see that a little-known token that’s supposed to be backed one-for-one to the dollar was getting printed in large quantities. That clue led the pair to another: When new batches appeared, the price of Bitcoin seemed to jump. It looked like someone, or a group, was using that freshly printed “free money” to inflate Bitcoin’s price for their own profit. He and his coauthor Shams sifted through an incredible 200 gigabytes of trading data, equal to the troves that the Smithsonian Institution collects in two years, and followed sales and purchases from 2.5 million separate wallets.

In 2018, they coauthored a groundbreaking study showing that a single, still unidentified, Bitcoin “whale” almost singlehandedly drove the token’s giant run-up in late 2017 and early 2018 by distorting the trading in the token.

Toward the end of 2022, another mystifying trend caught Griffin’s eye. Despite the crypto crash and myriad other negative forces, every time Bitcoin briefly breached the $16,000 floor, it bounced above that level and kept stubbornly trading between $16,000 and $17,000. Almost unbelievably, as the crypto market has continued to unravel into 2023, Bitcoin has gone in the opposite direction, trading up 35% since Jan. 7 to $23,000.

“It’s very suspicious,” Griffin told Fortune. “The same mechanism we saw in 2017 could be at play now in the still unreal Bitcoin market.”

For Griffin, the way normally super-volatile Bitcoin went calm and stable in the stormiest of times for crypto fits a scenario where boosters are uniting to support and juice its price. “If you’re a crypto manipulator, you want to set a floor under the price of your coin,” added Griffin. “In a period of highly negative sentiment, we’ve seen suspiciously solid floors under Bitcoin.”

Though manipulation is unproven, the signs are troubling

It’s important to note that no definitive proof of chicanery has so far emerged. “The space is bigger now so it’s harder to dig the data,” says Griffin. “Sophisticated players may be expert at hiding their identities.” We have seen credible leaks asserting that major market participants call meetings of the sector’s elite when they fear a crypto leader plans to make what they consider a reckless, industry-endangering move. But no evidence has surfaced that the players are gathering to coordinate buying of Bitcoin or other cryptocurrencies. For example it's well known that earlier this fall Changpeng Zhao (known as CZ), chief of Binance, the world’s largest crypto exchange and other crypto crypto leaders believed that Sam Bankman-Fried’s hedge fund Alameda was attacking Tether, the then-wobbling coin whose reliability is crucial to the industry’s well-being, and reportedly encouraged him to stop. (Tether—symbol USDT—by the way, was also at the center of the 2017-18 manipulation exposed by Griffin and Shams.)

It's possible that evidence of cozy, clubby practices will come to light in the numerous bankruptcy proceedings, lawsuits, and criminal investigations now pending in the crypto-verse. “Now that SBF is being charged, he’ll turn on the other players and could accuse them of collusion,” predicts Alex de Vries, an economist at the central bank of the Netherlands who runs Digiconomist, a site that tracks Bitcoin’s carbon footprint. The collapse Genesis's lending business has set Barry Silbert, the head of its parent Digital Currency Group, at the throats of Cameron and Tyler Winklevoss, cofounders of floundering exchange Gemini. The brothers claim that DCG owes the $900 million that Gemini’s depositors loaned to a Genesis program that paid high interest rates and threaten to sue DCG and Silbert, whom they accuse of stonewalling and denying DCG's true liability. Put simply, as onetime allies battle in court, the secrecy surrounding trading in concert, if it exists, could well crumble.

Griffin is far from the only prominent observer who’s wary of bad behavior. In a blog post on Nov. 30 titled “Bitcoin’s Last Stand,” European Central Bank Director General for market operations Ulrich Bindseil and ECB adviser Jürgen Schaaf dismissed Bitcoin’s resurgence as “an artificially induced last gasp before the road to irrelevance.” Two leading figures on Wall Street told this writer on background that Bitcoin’s price action, by resisting a flood of bad news, looks phony and different from a normal free market ruled by independent buyers and sellers.

Bitcoin has showed amazing stability amid negative sentiment

The leading sign that Bitcoin’s benefiting from coordinated buying: its astoundingly steady performance, forming the base for a takeoff to five-month highs following the FTX debacle that seemed likely to send the mainstay token reeling. From Nov. 5, the day before the FTX reports started spreading, to Nov. 9, Bitcoin (based on closing prices) dropped from $21,300 to $15,900, its lowest reading since late 2020, for a fall of 25%. Then the normally careening coin went, by Bitcoin standards, flat. In the 62 days between Nov. 10 and Jan. 11, it traded in the $16,000s and $17,000s for all but one day. In the 50 days from Nov. 22 to Jan. 11, its closing prices hovered in a narrow band, from a low of $16,200 and a high of $17,900, a difference from bottom to top of 10%.

This initial period of supersmooth sailing was atypical, to put it mildly. Fortune data editor Scott DeCarlo ran a detailed analysis and found that since the start of 2017, Bitcoin has never fluctuated in any of the 40 consecutive 50-day spans by less than 19%, and varied by over 30% in three out of four seven-week time frames. The median low to high reading was 44%. Hence, Bitcoin at peak FTX-induced turmoil showed both its smallest swings ever by a wide margin, and divergence from low to high that was one-fourth to one-fifth its average over the past six years.

Then, from Jan. 12 to 24, Bitcoin began a bizarre upward march. During those two weeks, it rebounded by 28% from $17,935 to $23,000, its best price since August and well above the number when FTX fears began raging. This occurred while the market was digesting the bankruptcies of lender BlockFi on Nov. 28; Core Scientific, one of the largest publicly traded miners, on Dec. 21; and the Genesis lending arm a month later.

You’d think that the turmoil surrounding Bitcoin would have shaken the confidence of small investors and institutions alike in crypto, leading to lots of selling pressure and sharply falling prices. Indeed, sentiment on social media turned heavily against Bitcoin following the FTX catastrophe. Reflecting the sinking enthusiasm was a steep retreat in trading activity. At Coinbase, volumes in Q4 were well below Q3 readings, and down 52% from Q1.

Could there be alternate explanations for Bitcoin's robust performance? A number of experts who follow crypto trading from day to day see no plot to inflate the prices, but a well-functioning market. “I don’t see a cabal of insiders,” says Andrew Thurman, a researcher at Blockchain analytics provider Nansen. “The price movements in Bitcoin are notoriously cyclical by nature. Often the best explanation is the most boring one. In this case, the price of Bitcoin is rising because there are more buyers than sellers. If anything, fallen players such as Celsius and FTX were selling Bitcoin and pushing down prices to prop up their own coins.” Vetle Lunde, a senior analyst at Norwegian crypto data analysis firm Arcane Research, agrees. “I don’t see a group holding up prices. Now we have a balanced dynamic. The forced selling following the FTX collapse has to some extent been absorbed and we’re seeing no further forced selling,” a phenomenon that’s aided Bitcoin’s recent rebound to over $23,000.

But there's no question that Bitcoin's post-FTX sturdiness, capped by its new jump, is a gigantic gift to the enterprises whose fortunes wax and wane with Bitcoin’s price. The stocks for exchanges, miners, and lenders all took a big leg down in the days after meltdown. But since hitting two-year lows in December, miners Riot, Marathon, and Bitfarms have jumped 92%, 150%, and 189% respectively as of Jan. 27. Coinbase, one of the world’s largest exchanges, has advanced 85% from its pre–New Year’s trough, adding $7 billion in market cap. Riot, Bitfarms have all rebounded to near their plateaus just prior to the FTX disaster.

One of the players most desperate for a boost got a big one. At MicroStrategy, cofounder and executive chairman Michael Saylor loaded his hybrid software provider and Bitcoin speculator with $2.4 billion in debt to buy coins, and when prices fell below $16,000 on Nov. 11, owed far more on his loans than the value of his cache of tokens. If Bitcoin kept dropping, MicroStrategy was heading for big trouble. But Bitcoin’s resurgence has lifted MicroStrategy’s holdings out of the red and sent its stock price from $166 in mid-November to $258 on Jan. 27, a gain of 55%.

Crypto operates on a narrower edge than virtually any other financial sector. The factor that determines whether the big crypto players mint profits or tumble into bankruptcy is the price of Bitcoin, the benchmark that in turn leads the prices for other coins. Much of the crypto world has already shattered. But a lot more stalwarts were due to go down unless Bitcoin found a decent foundation after the FTX downfall shook that slender edge.

Griffin and Shams’ findings from the 2017–18 rigging are echoing today

The Griffin-Shams study of the forces behind the 2017–18 Bitcoin bubble provides a guide to the strategies that could be pressing a thumb on the sales post-FTX. Griffin and Shams, now a professor at Ohio State’s Fisher College of Business, first published their 118-page report in 2018, and it appeared two years later in the prestigious, peer-reviewed Journal of Finance.

For the team, a tipoff for possible manipulation was that Bitfinex, the large exchange closely related to Tether, wasn’t providing much transparency about the supposed stablecoin. “We saw blogs speculating that Bitfinex wasn’t providing full backing for the coin,” recalls Griffin. “If someone’s printing money by printing Tether that’s unbacked by fiat currency, it could cause a bubble in Bitcoin,” he says. “That was the hypothesis.”

Griffin and Shams found that two practices converged to spur those huge, sudden gains. The first: a flood of newly created coins that gave the fraudster the currency to goose Bitcoin. The second is the approach that’s most relevant today, in which the manipulator or manipulators agree that every time the price drops to a target level, they’ll jump in to push it well above that benchmark.

The pair saw a strong and questionable pattern in Bitcoin prices. Bitcoin had its biggest spikes when two things happened: Prices started dropping, and lot of Tether was being printed. Then, as now, Tether was the most important “stablecoin,” or cryptocurrency supposedly supported one-to-one by reserves in fiat currency. Tether’s effectively a stand-in for the dollar; each coin is supposed to be backed by the equivalent of one greenback in fiat currency. Tether is issued by an arm of iFinex, a Hong Kong company that also owns what was then the world’s largest exchange, Bitfinex.

The authors focused on the 1% of all one-hour intervals between the beginning of March 2017 and end of March 2018 that featured the largest combinations of large Tether issuance on Bitfinex, and big Bitcoin buys on two other exchanges, Bittrex and Poloniex. Just before the start of each period, Bitcoin prices were under pressure. But in each case, it appeared that a single huge buyer rode to the rescue, pushing the token sharply higher by the end of the 60-minute interlude. The “whale,” whose identity remains a mystery, was using Tether to buy Bitcoin and hike its price. “We saw a regular pattern of very sizable price reversals,” recalls Shams.

The 95 one-hour spans that witnessed those big Tether and Bitcoin inflows accounted for nearly 60% of Bitcoin’s immense gains over those 13 months.

“Tether is used as cash to trade Bitcoin and other cryptocurrencies,” notes Shams. Although the market cap of Tether is a fraction of Bitcoin’s, Tether’s trading volumes are higher. Given its importance in trading, the printing of Tether without backing creates “new money” the way the Fed does when it prints excess quantities of dollars. “The issuing of Tether without backing inflated the amount of currency chasing the same supply of Bitcoin,” Griffin told Fortune. “The Tether created from thin air was inflating the price of Bitcoin and other cryptocurrencies.”

Once the whale obtained the newly minted Tether, it traded the coins for big quantities of Bitcoin on Bittrex and Poloniex. Those large buys reversed the downward trend in Bitcoin and boosted its price well above its level before the dip began. “This player either showed clairvoyant market timing or exerted an extremely large effect on Bitcoin’s price,” states the study. Today, it’s clear that Tether wasn’t holding full reserves behind the coins in this Bitcoin boom period, so that “it’s almost mechanical that money from nowhere would boost the price,” notes Griffin.

After the paper appeared, Tether Ltd. insisted that its conclusions were flawed and maintained that Tether couldn’t be used to balloon Bitcoin prices. But a Commodity Futures Trading Commission investigation found otherwise. In October 2021, the CFTC won a $41 million settlement from Tether and its owners for failing to back its coins with dollars as advertised. The CFTC found that “Tether held sufficient reserves to back…tokens in circulation only 27.6% of the time in the 26-month sample from 2016 through 2018” and “comingled reserve funds with Bitfinex’s operational and customer funds.” Says Griffin, “Bitcoin and Tether aren’t used for buying things like cars and pizzas, they’re used for buying other coins. So in that closed system, a relatively small amount of manipulated buying, spurred by creating new coins from nothing, can cause an outsize increase in the Bitcoin price.”

The whale mastered setting a floor and kept the floor rising

The authors also found that the sizable purchases frequently happened when Bitcoin’s price reached certain thresholds, just below multiples of $500. “We saw far more purchases at those benchmarks,” says Griffin. “The whale kept establishing price floors, and those floors kept rising. It wasn’t a club. It was one entity. But when the whale held the price at the thresholds, that made it look as if Bitcoin was safe at those floors. That made it look safe for funds and small customers to buy Bitcoin, driving the price still higher.” Adds Shams, “Around round number price levels of Bitcoin, we saw activities consistent with creating price supports.”

Griffin suspects that a similar dynamic is operating today. He says that collusion to prop up Bitcoin would mean that a clique of buyers agrees to purchase together when the price nears a floor. Let’s say that trigger is $16,000, a figure Bitcoin almost always remained just above during its time of extreme stability. If Bitcoin experiences heavy sales threatening to drive its price below $16,000, in our example, the whale club enters en masse.“That $16,000, for example, could serve as a coordinating mechanism,”says Griffin. The manipulators could drive the price up to near $17,000, then sell part of their winnings in many small trades that don’t move the market. They could pocket big profits just letting the price bounce back and forth in the tunnel between $16,000 and $17,000.

Growing confidence that Bitcoin won’t breach $16,000 would encourage more speculators to join in the buying. Then the group can agree to set a new floor at $18,000. “In crypto, a group of manipulators can push Bitcoin to higher floors unless a big party moves against them,” says Griffin. But it’s much harder to short Bitcoin than to short stocks or bonds. We aren’t seeing evidence of another group moving to drive down the price, giving a stronger hand to any possible club of bulls. “Most of the players in the space have a strong incentive to maintain a price floor,” says Griffin.

In conclusion, Griffin says, the Griffin-Shams study showed concrete proof of manipulation in 2017 and 2018, and that a single individual did the rigging. “We don’t have concrete analysis this time,” he says. “The truth may emerge in specific stories, if there is collusion.” The lesson, he says, “is that the Bitcoin market remains highly vulnerable to manipulation.”

Indeed, Bitcoin in the wake of the FTX debacle has registered a wondrous performance. Maybe too wondrous to be trusted.

请打开财富Plus APP