银行业趋势于稳定,但美国小企业的压力未减

TRISTAN BOVE , WILL DANIEL

2023-04-19

小企业被称为经济支柱是有原因的,它们雇佣了46%的美国工人,贡献了近一半的GDP。

文本设置

文本设置

Plus(0条)

Plus(0条)

小企业被称为经济支柱是有原因的。它们雇佣了46%的美国工人,贡献了近一半的GDP,在大流行期间,随着申请开办新企业的人数创下纪录,小企业蓬勃发展。但在去年,情况发生了逆转,首先是因为通胀飙升,其次是主要地区银行的倒闭——硅谷银行和签名银行的倒闭(美国史上第二和第三大倒闭案)登上头条。对银行业整合的恐慌情绪正在飙升,随之而来的是小企业面临的更具挑战性的经济环境,那么问题来了:如果当地银行倒闭了,创业者怎么办?银行体系稳定吗? 信贷紧缩是否即将来临?专家们对此意见不一,凸显了这场辩论的开放性。

美国财政部长珍妮特·耶伦(Janet Yellen)曾表示,银行业形势正趋向于“稳定”,花旗集团首席执行官简·弗雷泽(Jane Fraser)说,最近的混乱并“不构成信贷危机”,而是少数银行出现的孤立性问题。但“末日博士”、经济学家鲁里埃尔·鲁比尼(Nouriel Roubini)本周警告称,银行业危机可能引发经济“三难困境”,导致经济衰退,并最终引发重大信贷风险。最后,美联储主席杰罗姆·鲍威尔(Jerome Powell)上周警告说,银行业崩溃“可能会导致家庭和企业信贷条件收紧,这反过来又会影响经济状况。”

信贷紧缩对任何公司来说都是打击,但对资源较少的小企业来说尤其致命。“实力雄厚的大企业可以调用大量内部储备。”学术期刊《小企业经济学》(Small Business Economics)主编大卫·奥德里奇(David Audretsch)在接受《财富》杂志采访时表示,大企业有其他融资来源,而小企业往往在利率上升和流动性枯竭时 "受到冲击"。

如果考虑到许多小银行(通常是小企业的命脉)目前的困境,这个问题就会被放大。多年来的银行业整合已经导致贷款业务被不为小企业服务的华尔街巨头所控制,而最近的银行业危机只会加剧这一趋势。

奥德里奇表示:"总之......小企业将受到影响。如今对小企业主来说并不是好时机。"

小企业面临的大问题

大公司可以利用股票和债券市场融资,而小企业主要依靠信贷来支付从工资支出到租金的一切费用。倡导性非营利组织地方自力更生研究所(Institute for Local Self-Reliance)的数据显示,86%至94%的小企业使用信贷支付费用,其中52%的融资来自社区银行。

奥德里奇说:“我和一些小企业主谈过,他们意识到自己陷入了麻烦,因为他们无法获得贷款,或者成本会增加。我认为,情况在好转之前还会进一步恶化。”奥德里奇也是印第安纳大学的发展经济学家。

在某些方面,信贷紧缩只会导致预先存在的趋势加剧。美国商会(U.S. Chamber of Commerce)本周公布的一项调查显示,贷款可获得性已经连续五年下降,只有49%的小企业主表示他们目前的融资渠道良好。调查还发现,只有五分之一的小企业主认为美国经济状况良好。融资不足也导致越来越多的创业者动用自己的银行账户来支付费用,75%的企业主雇佣的员工少于5人,59%的规模较大的小企业主动用了自己的个人储蓄。

美国商会小企业政策副总裁汤姆·苏利文(Tom Sullivan)在接受《财富》杂志采访时表示:“一年多来,小企业一直在为信贷紧缩做准备。我们从未预料到一系列银行业的挑战会导致这场信贷紧缩。一年多以来,我们一直预期经济衰退会导致信贷紧缩。”

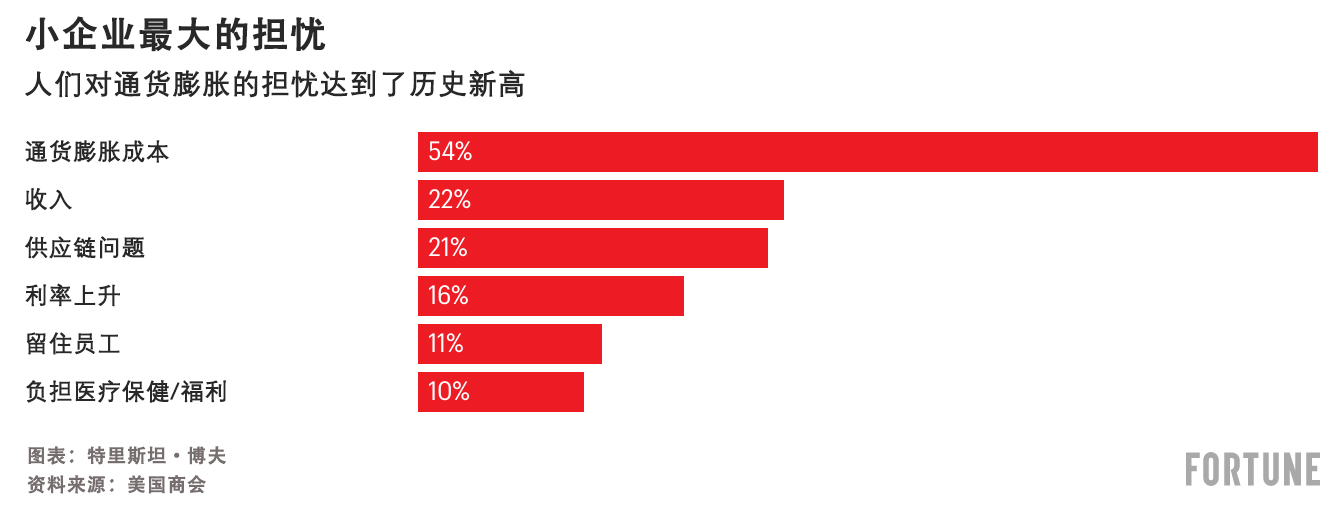

不过,专家们认为,尽管在一段时间内很难获得融资给小企业带来了负担,但该行业面临的更大挑战是通货膨胀。去年,85%的小企业主表示,他们的经营受到了商品和燃料价格上涨的影响,尽管通货膨胀率最近已经从去年夏天开始的一系列40年高点回落,但在美国商会最近的调查中,54%的小企业称这仍是他们最担忧的问题,超过了对盈利能力和利率上升的担忧。

美国商会资本市场竞争力中心执行副总裁汤姆·夸德曼(Tom Quaadman)在接受《财富》杂志采访时表示: “通货膨胀是一个长期问题。信贷紧缩更倾向于是一个短期问题,但你必须同时应对这两个问题。更睿智的企业主会想出一个一箭双雕的计划。”

在短期内应对信贷紧缩可能意味着要高度关注基本面和效率,同时还要密切关注通货膨胀和物价。巧妙地利用融资将是关键,但银行业危机后资金从何而来则是另一回事。

另一大困境:小银行的消失

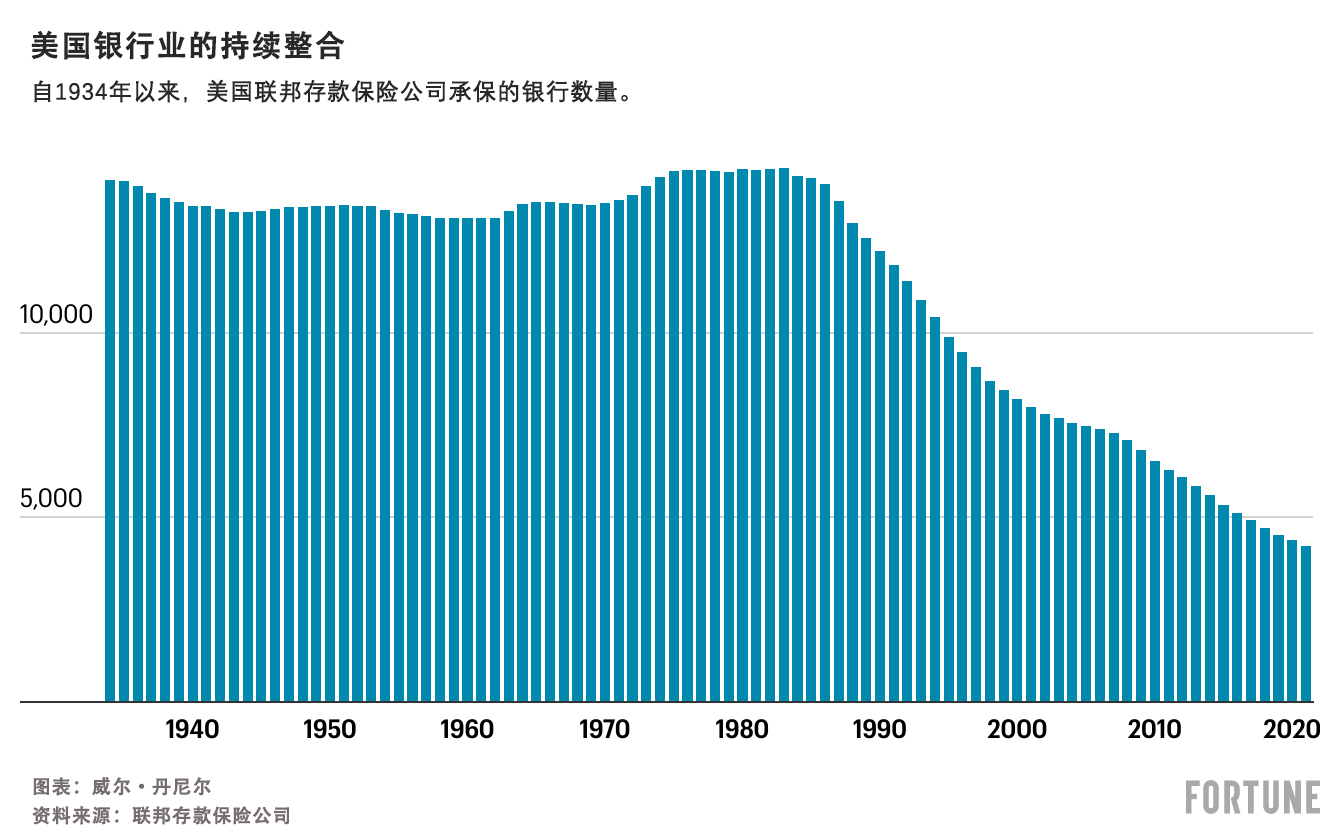

除了应对顽固的通货膨胀和每况愈下的经济,美国小企业正在慢慢失去一些最重要的合作伙伴:社区和地区银行。最近的银行业危机加剧了美国金融业长达数十年的整合。根据美联储的数据,自1984年以来,由于监管方面的变化和新技术使大型银行能够以较低的成本在全国范围内提供贷款服务,大约三分之二的美国银行已经消失。

科罗拉多州立大学经济学教授斯蒂芬·维勒(Stephan Weiler)在接受《财富》杂志采访时表示,当监管机构出面拯救硅谷银行和签名银行的储户时(甚至包括那些未投保的储户),消费者也产生了这样的印象:“大银行拥有小银行没有的东西”——几乎是全面纾困的“保证”。他说,这种担保让“大银行的吸引力变得非常大”。

美联储数据显示,硅谷银行破产后一周,小银行的存款减少了1190亿美元,而大银行的存款流入则有所增加。例如,美国银行(Bank of America)仅在那一周就流入了150亿美元。

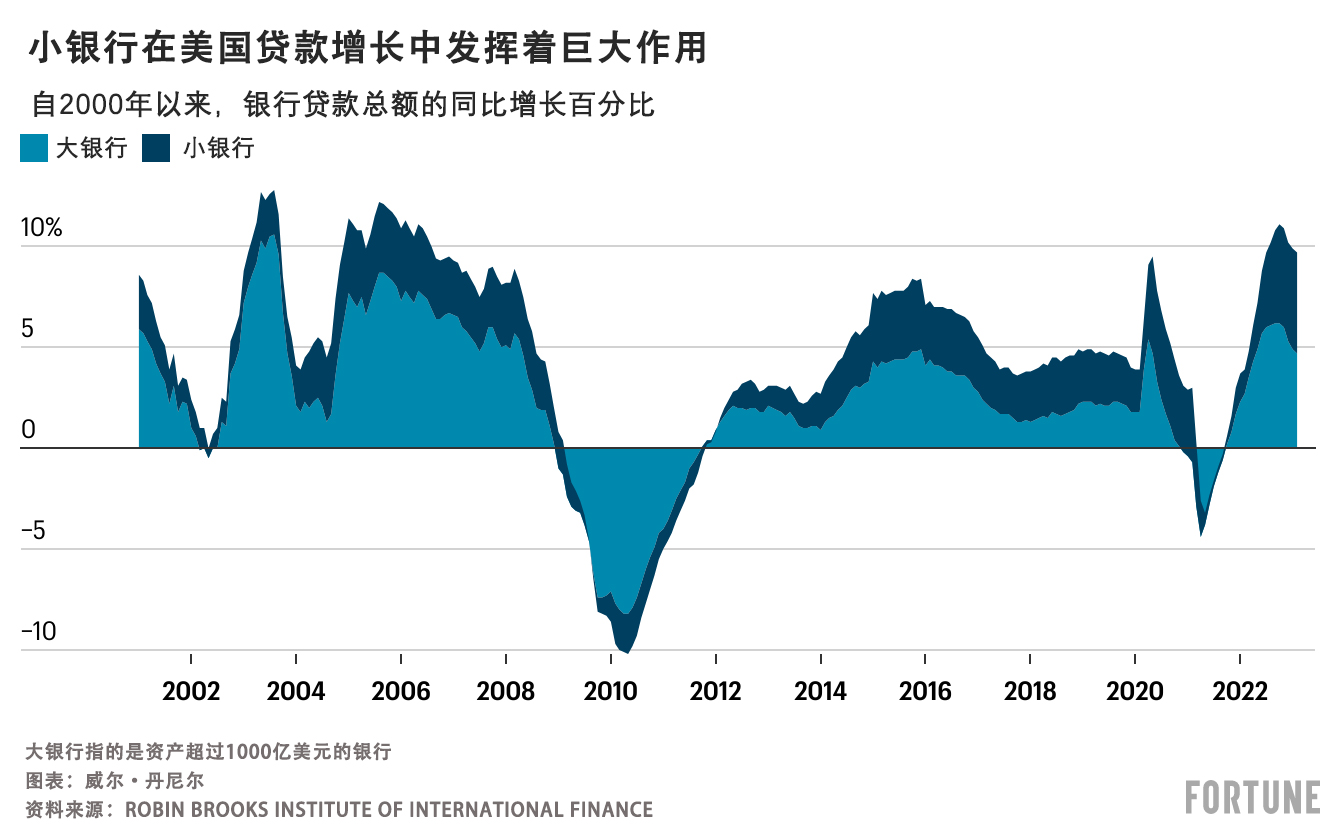

根据维勒的说法,如果存款继续从美国的地区和社区银行流出,这肯定会给小企业带来压力,因为历史上,小银行在推动美国贷款增长方面发挥着巨大的作用

同时担任区域经济发展研究所所长的维勒指出,社区和地区银行为小企业提供的贷款也远远多于规模较大的银行。

他说:“就份额而言,社区银行的商业贷款是大银行的三倍。”他补充说,这是因为小银行更了解当地客户的业务,能够为客户提供大银行甚至不会考虑的贷款。

维勒认为,小银行放贷的意愿使得它们在全国范围内“对创业和就业增长至关重要”。他表示,美国经济协会(American Economic Association)2019年发表的一项研究发现,地区和社区银行的关闭“导致当地小企业贷款持续下降”。

维勒表示:“社区银行越多,获得关系型贷款的可能性就越大,贷款基础就越稳定。这实际上会带来经济复原力,特别是在农村地区。”

困难时期的“盔甲”

随着融资变得越来越困难,小企业将需要运用创造性和灵活性来应对市场逆风。幸运的是,正如许多公司在大流行期间证明的那样,小企业知道如何适应环境。

奥德里奇称:"小企业若要渡过难关,并利用好危机环境中的机遇,毫无疑问,他们必须具备弹性和灵活性。"

目前尚不清楚银行业危机会在多大程度上通过金融体系造成蔓延,但考虑到其风险,小企业发生的情况可能是一个显著标志。奥德里奇称,该行业内"裁员和破产激增"将是经济衰退甚至金融萧条临近的一个指标。

但到目前为止,尽管信贷紧缩和通货膨胀持续存在,但小企业仍然具有韧性,即使他们对整体经济持悲观态度。在接受美国商会调查的企业主中,约三分之二的人表示,他们的企业财务状况良好,现金流充裕,69%的人表示,他们在过去一年里保留了相同数量的员工。

美国商会的沙利文表示:“许多在新冠肺炎疫情中幸存下来的小企业主现在都穿上了这身盔甲。他们说,‘如果我们能度过新冠肺炎疫情那样的难关,我们就能度过任何难关’,这很有道理。”

从新冠肺炎疫情中走出来的小企业是那些富有创造力并适应了新环境的企业。同样,过去一年不断恶化的市场环境淘汰了不可持续的科技初创公司和加密货币公司。现在创业的人可能会越来越少,小企业的发展可能在某种程度上是关于适者生存的(这与多年前的情况大不相同)。(财富中文网)

译者:中慧言-王芳

小企业被称为经济支柱是有原因的。它们雇佣了46%的美国工人,贡献了近一半的GDP,在大流行期间,随着申请开办新企业的人数创下纪录,小企业蓬勃发展。但在去年,情况发生了逆转,首先是因为通胀飙升,其次是主要地区银行的倒闭——硅谷银行和签名银行的倒闭(美国史上第二和第三大倒闭案)登上头条。对银行业整合的恐慌情绪正在飙升,随之而来的是小企业面临的更具挑战性的经济环境,那么问题来了:如果当地银行倒闭了,创业者怎么办?银行体系稳定吗? 信贷紧缩是否即将来临?专家们对此意见不一,凸显了这场辩论的开放性。

美国财政部长珍妮特·耶伦(Janet Yellen)曾表示,银行业形势正趋向于“稳定”,花旗集团首席执行官简·弗雷泽(Jane Fraser)说,最近的混乱并“不构成信贷危机”,而是少数银行出现的孤立性问题。但“末日博士”、经济学家鲁里埃尔·鲁比尼(Nouriel Roubini)本周警告称,银行业危机可能引发经济“三难困境”,导致经济衰退,并最终引发重大信贷风险。最后,美联储主席杰罗姆·鲍威尔(Jerome Powell)上周警告说,银行业崩溃“可能会导致家庭和企业信贷条件收紧,这反过来又会影响经济状况。”

信贷紧缩对任何公司来说都是打击,但对资源较少的小企业来说尤其致命。“实力雄厚的大企业可以调用大量内部储备。”学术期刊《小企业经济学》(Small Business Economics)主编大卫·奥德里奇(David Audretsch)在接受《财富》杂志采访时表示,大企业有其他融资来源,而小企业往往在利率上升和流动性枯竭时 "受到冲击"。

如果考虑到许多小银行(通常是小企业的命脉)目前的困境,这个问题就会被放大。多年来的银行业整合已经导致贷款业务被不为小企业服务的华尔街巨头所控制,而最近的银行业危机只会加剧这一趋势。

奥德里奇表示:"总之......小企业将受到影响。如今对小企业主来说并不是好时机。"

小企业面临的大问题

大公司可以利用股票和债券市场融资,而小企业主要依靠信贷来支付从工资支出到租金的一切费用。倡导性非营利组织地方自力更生研究所(Institute for Local Self-Reliance)的数据显示,86%至94%的小企业使用信贷支付费用,其中52%的融资来自社区银行。

奥德里奇说:“我和一些小企业主谈过,他们意识到自己陷入了麻烦,因为他们无法获得贷款,或者成本会增加。我认为,情况在好转之前还会进一步恶化。”奥德里奇也是印第安纳大学的发展经济学家。

在某些方面,信贷紧缩只会导致预先存在的趋势加剧。美国商会(U.S. Chamber of Commerce)本周公布的一项调查显示,贷款可获得性已经连续五年下降,只有49%的小企业主表示他们目前的融资渠道良好。调查还发现,只有五分之一的小企业主认为美国经济状况良好。融资不足也导致越来越多的创业者动用自己的银行账户来支付费用,75%的企业主雇佣的员工少于5人,59%的规模较大的小企业主动用了自己的个人储蓄。

美国商会小企业政策副总裁汤姆·苏利文(Tom Sullivan)在接受《财富》杂志采访时表示:“一年多来,小企业一直在为信贷紧缩做准备。我们从未预料到一系列银行业的挑战会导致这场信贷紧缩。一年多以来,我们一直预期经济衰退会导致信贷紧缩。”

不过,专家们认为,尽管在一段时间内很难获得融资给小企业带来了负担,但该行业面临的更大挑战是通货膨胀。去年,85%的小企业主表示,他们的经营受到了商品和燃料价格上涨的影响,尽管通货膨胀率最近已经从去年夏天开始的一系列40年高点回落,但在美国商会最近的调查中,54%的小企业称这仍是他们最担忧的问题,超过了对盈利能力和利率上升的担忧。

美国商会资本市场竞争力中心执行副总裁汤姆·夸德曼(Tom Quaadman)在接受《财富》杂志采访时表示: “通货膨胀是一个长期问题。信贷紧缩更倾向于是一个短期问题,但你必须同时应对这两个问题。更睿智的企业主会想出一个一箭双雕的计划。”

在短期内应对信贷紧缩可能意味着要高度关注基本面和效率,同时还要密切关注通货膨胀和物价。巧妙地利用融资将是关键,但银行业危机后资金从何而来则是另一回事。

另一大困境:小银行的消失

除了应对顽固的通货膨胀和每况愈下的经济,美国小企业正在慢慢失去一些最重要的合作伙伴:社区和地区银行。最近的银行业危机加剧了美国金融业长达数十年的整合。根据美联储的数据,自1984年以来,由于监管方面的变化和新技术使大型银行能够以较低的成本在全国范围内提供贷款服务,大约三分之二的美国银行已经消失。

科罗拉多州立大学经济学教授斯蒂芬·维勒(Stephan Weiler)在接受《财富》杂志采访时表示,当监管机构出面拯救硅谷银行和签名银行的储户时(甚至包括那些未投保的储户),消费者也产生了这样的印象:“大银行拥有小银行没有的东西”——几乎是全面纾困的“保证”。他说,这种担保让“大银行的吸引力变得非常大”。

美联储数据显示,硅谷银行破产后一周,小银行的存款减少了1190亿美元,而大银行的存款流入则有所增加。例如,美国银行(Bank of America)仅在那一周就流入了150亿美元。

根据维勒的说法,如果存款继续从美国的地区和社区银行流出,这肯定会给小企业带来压力,因为历史上,小银行在推动美国贷款增长方面发挥着巨大的作用

同时担任区域经济发展研究所所长的维勒指出,社区和地区银行为小企业提供的贷款也远远多于规模较大的银行。

他说:“就份额而言,社区银行的商业贷款是大银行的三倍。”他补充说,这是因为小银行更了解当地客户的业务,能够为客户提供大银行甚至不会考虑的贷款。

维勒认为,小银行放贷的意愿使得它们在全国范围内“对创业和就业增长至关重要”。他表示,美国经济协会(American Economic Association)2019年发表的一项研究发现,地区和社区银行的关闭“导致当地小企业贷款持续下降”。

维勒表示:“社区银行越多,获得关系型贷款的可能性就越大,贷款基础就越稳定。这实际上会带来经济复原力,特别是在农村地区。”

困难时期的“盔甲”

随着融资变得越来越困难,小企业将需要运用创造性和灵活性来应对市场逆风。幸运的是,正如许多公司在大流行期间证明的那样,小企业知道如何适应环境。

奥德里奇称:"小企业若要渡过难关,并利用好危机环境中的机遇,毫无疑问,他们必须具备弹性和灵活性。"

目前尚不清楚银行业危机会在多大程度上通过金融体系造成蔓延,但考虑到其风险,小企业发生的情况可能是一个显著标志。奥德里奇称,该行业内"裁员和破产激增"将是经济衰退甚至金融萧条临近的一个指标。

但到目前为止,尽管信贷紧缩和通货膨胀持续存在,但小企业仍然具有韧性,即使他们对整体经济持悲观态度。在接受美国商会调查的企业主中,约三分之二的人表示,他们的企业财务状况良好,现金流充裕,69%的人表示,他们在过去一年里保留了相同数量的员工。

美国商会的沙利文表示:“许多在新冠肺炎疫情中幸存下来的小企业主现在都穿上了这身盔甲。他们说,‘如果我们能度过新冠肺炎疫情那样的难关,我们就能度过任何难关’,这很有道理。”

从新冠肺炎疫情中走出来的小企业是那些富有创造力并适应了新环境的企业。同样,过去一年不断恶化的市场环境淘汰了不可持续的科技初创公司和加密货币公司。现在创业的人可能会越来越少,小企业的发展可能在某种程度上是关于适者生存的(这与多年前的情况大不相同)。(财富中文网)

译者:中慧言-王芳

Small businesses are referred to as the backbone of the economy for a reason. They employ 46% of American workers and make up nearly half of GDP, and they boomed during the pandemic as new business applications set records. But things have turned the other direction in the last year, first because of soaring inflation and then major regional bank failures—headlined by the second and third-largest collapses ever, at Silicon Valley Bank and Signature Bank. The specter of banking consolidation is rising, and with it an even more challenging economic environment for small business, raising the questions: What becomes of the entrepreneur if their local bank goes away? Is the banking system stable? And is a credit crunch on the horizon? Underscoring the open nature of this debate, expert opinion is split.

Treasury Secretary Janet Yellen has said that the banking situation is “stabilizing,” and Citigroup CEO Jane Fraser said the recent chaos “is not a credit crisis,” rather just a few banks with isolated problems. But “Dr. Doom” himself, the economist Nouriel Roubini, warned this week that the banking crisis could spark an economic “trilemma” leading to a recession and, eventually, significant credit risk. And finally, Federal Reserve Chair Jerome Powell cautioned last week that the banking collapses are “likely to result in tighter credit conditions for households and businesses, which would in turn affect economic outcomes.”

Economists are still expecting a “softish” landing with one more rate hike this year

A credit crunch would be a blow to any company, but is especially deadly for a small business with fewer resources. “Big companies have a lot of internal reserves that they can turn to. They’ve got other sources of finance,” David Audretsch, editor-in-chief of the Small Business Economics academic journal, told Fortune, while small businesses tend to “take the hit” when interest rates rise and liquidity dries up.

The problem is magnified when considering the ongoing troubles at many small banks which have typically been the lifeblood of small business. Years of banking consolidation have caused lending to be dominated by Wall Street behemoths that don’t cater to small businesses, and the recent banking crisis only made that trend worse.

“The bottom line … small businesses are going to be affected,” Audrestch said. “This is a bad time to be a small business.”

Big problems for small business

Unlike large corporations, which can tap equity and bond markets for financing, small businesses primarily rely on credit to cover everything from payroll expenses to rent. Between 86% and 94% of small businesses use credit to cover their expenses, and 52% of that financing comes from community banks, according to the Institute for Local Self-Reliance, an advocacy non-profit group.

“I’ve talked to small businesses that realize they’re in trouble because the loans aren’t going to be there, or they’re going to cost more. And I think that’s going to get worse before it gets better,” said Audretsch, who is also a developmental economist at Indiana University.

In some ways, the credit crunch would just amplify a preexisting trend. Loan availability has been declining for five years, and only 49% of small business owners say their current access to capital is good, according to a survey published by the U.S. Chamber of Commerce this week, which also found that only one in five small business owners sees the U.S. economy as being in good health. The lack of financing has also led to a growing share of entrepreneurs digging into their own bank accounts to cover expenses, with 75% of owners employing fewer than five people and 59% of larger small businesses tapping their own personal savings.

“Small businesses have been preparing for a tightening of credit for over a year,” Tom Sullivan, vice president of small business policy at the Chamber of Commerce, told Fortune. “We never foresaw that a set of banking challenges would result in this credit crunch. What we expected for over a year is that a recession would cause the credit crunch.”

But while more elusive financing has burdened small businesses for a while, the much bigger challenge to the sector, experts agree, has been inflation. Last year, 85% of small business owners said their operations had been affected by rising prices for goods and fuel, and even though inflation has recently fallen from a series of 40-year highs starting last summer, 54% of small businesses cited it as their biggest concern in the Chamber of Commerce’s recent survey, outpacing worries over profitability and rising interest rates.

“Inflation is a long-term problem. A credit crunch is more of a short-term problem, but you have to deal with both,” Tom Quaadman, executive vice president at the Chamber’s Center for Capital Markets Competitiveness, told Fortune. “The smarter businesses are going to figure out a plan to deal with both.”

Handling the credit crunch in the short term will likely mean having a strong focus on fundamentals and efficiency while also keeping an eye on inflation and prices. Smart use of financing will be key, but where that funding comes from post-banking crisis is another matter.

Yet another dilemma: vanishing small banks

On top of dealing with stubborn inflation and an ailing economy, U.S. small businesses are slowly losing some of their most critical partners: community and regional banks. The recent banking crisis has exacerbated a decades-long consolidation in the U.S. financial industry. Since 1984, roughly two-thirds of U.S. banks have disappeared due to regulatory changes and new technologies that enabled larger institutions to provide lending services nationwide at lower costs, according to the Federal Reserve.

And when regulators stepped in to save SVB and Signature Bank’s depositors, even those whose funds weren’t insured by the FDIC, consumers got the impression that “the big banks have something that the little banks don’t,” Stephan Weiler, an economics professor at Colorado State University, told Fortune—a near “guarantee” of a full bailout. That guarantee has made “the attraction of bigger banks pretty overwhelming,” he said.

Deposits at small banks fell by $119 billion the week after SVB’s collapse, according to Fed data, while large banks saw increased deposit inflows. Bank of America, for example, raked in $15 billion that week alone.

If deposits continue to flow out of America’s regional and community banks, it’s sure to put pressure on small businesses, according to Weiler, because smaller banks have played an outsized role historically in driving loan growth in the U.S.

Weiler, who also serves as the director of the Regional Economic Development Institute, noted that community and regional banks do far more small business lending than their larger peers as well.

“In terms of a share, community banks do three times the business lending of the bigger banks,” he said, adding that this is because smaller banks have a better understanding of local clients’ businesses, allowing them to provide loans that larger lenders wouldn’t even consider.

Smaller banks’ willingness to lend makes them “crucial to entrepreneurship and job growth” across the country, Weiler argues. And to his point, a 2019 study published by the American Economic Association found that regional and community bank closings “lead to a persistent decline in local small business lending.”

“The more community banks there are, the greater the relationship lending possibilities are, the more stable the loan base is. And that actually leads to economic resilience, especially in rural areas,” Weiler said.

‘Suit of armor’ in hard times

With obtaining financing becoming more difficult, small businesses will need to be creative and flexible to handle market headwinds. Fortunately, as many firms proved during the pandemic, small business knows how to adapt.

“Small businesses that make it through this that are able to harness the opportunities of this crisis climate, there’s no doubt they’ll have to be nimble and flexible,” Audretsch said.

It is still unclear to what extent the banking crisis could cause contagion through the financial system, but given its exposure, looking at what happens to small business could be a telling sign. A “spike up in layoffs and bankruptcies” within the sector would be an indicator of a looming recession or even a financial depression, Audretsch said.

But so far, despite the credit crunch and inflation’s staying power, small businesses have been resilient even if they’re pessimistic about the overall economy. Around two thirds of owners surveyed by the Chamber said their businesses were in good financial health with comfortable cash flows, while 69% said they have retained the same number of employees in the past year.

“A lot of these successful small business owners having survived COVID have this suit of armor on now,” according to the Chamber’s Sullivan. “They say, ‘If we can get through COVID we can get through anything,’ and there’s a lot of truth to that.”

The small businesses that made it out of COVID were the ones that were creative and adapted to their new conditions. In the same way, the past year’s souring market environment has weeded out unsustainable tech startups and crypto companies. Now entrepreneurship could be in for a thinning too—thriving in small business may be, in a way it hasn’t been for many years, about survival of the fittest.

请打开财富Plus APP