德州奥斯汀躲过了2008年的房地产市场崩溃,现在却成为市场回调的中心

LANCE LAMBERT

2023-06-07

在美国400个大型房地产市场中,奥斯汀的房价在本轮市场回调中下跌幅度最大。

文本设置

文本设置

Plus(0条)

Plus(0条)

本世纪初,随着房价上涨,炒房客们纷纷押注快速上涨的阳光地带市场,如凤凰城、拉斯维加斯和迈阿密等。投机者往往希望通过炒房获利,他们认为人口密集的阳光地带市场风险最低,却能带来最高的回报。当然,事实证明他们大错特错,因为这些市场繁荣变成了最严重的房地产泡沫。泡沫最终破灭,并引发了金融危机。

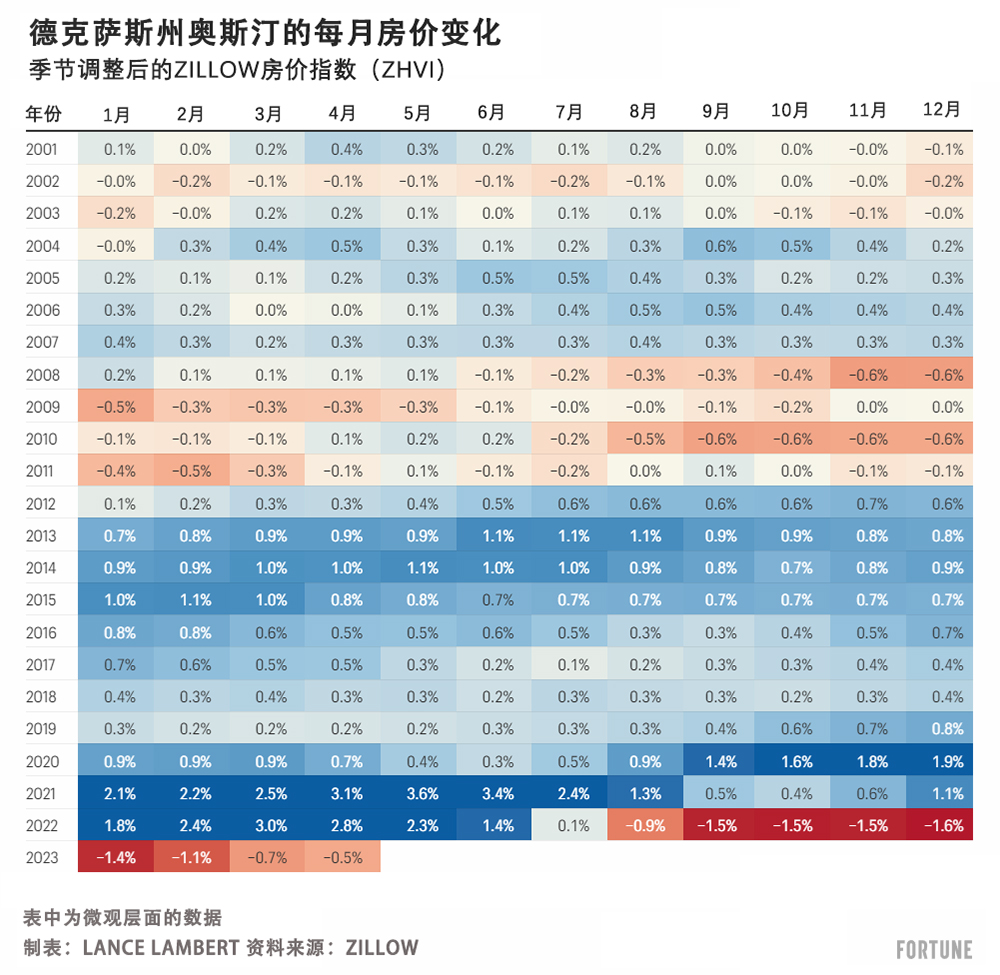

相对而言,本世纪初的阳光地带房地产市场崩溃只有一个例外,那就是孤星州德克萨斯。奥斯汀和达拉斯等市场从房价最高点到最低点分别仅下跌了8.5%和10.5%,而Zillow房价指数(Zillow Home Value Index,ZHVI)跟踪的房价显示,从2007年左右到2012年左右,拉斯维加斯、凤凰城和迈阿密从房价最高点到最低点的跌幅分别高达63.9%、56.4%和52.2%。

虽然在2005年左右,全美积极的贷款机构纷纷允许借款人以极低的首付申请按揭,但德克萨斯却继续采取保守的贷款政策。更严格的贷款法律帮助德克萨斯州躲过了本世纪初的房地产市场崩溃,而且据德州农工大学(Texas A&M)的研究人员表示,这些法律还减少了“止赎的数量”。

时间来到2023年,德克萨斯州有一个城市成为疫情期间的房地产繁荣和房地产回调的中心,它就是奥斯汀。

事实上,Zillow房价指数显示,从2022年7月至2023年4月,奥斯汀的房价下跌了10.02%,是同期全美房价下跌幅度(1%)的10倍。这是全美400个大型房地产市场到目前为止的最大跌幅,超过了旧金山(-10%)、俄勒冈州班德(-9.5%)和博伊西(-9.3%)。

当全美大多数市场的房价几乎没有下跌时,为什么奥斯汀会受到如此严重的冲击?首先,奥斯汀市场泡沫化严重。

理论上,房地产泡沫需要具备三个条件。

第一,房地产泡沫需要房价被严重高估,这意味着本地房价远高于本地收入历史上能够支撑的房价。奥斯汀在疫情期间的房地产繁荣中就发生了这样的情况。事实上,据穆迪分析(Moody's Analytics)统计,在2022年第一季度房价最高时,奥斯汀的房价“被高估”63.7%。穆迪认为,这个比例只要高于25%就属于“被严重高估”。

第二,房地产泡沫需要有投机者。虽然这一点很难量化,但它通常表现为投资者的过度扩张。奥斯汀资深房地产中介和房地产投资人西恩·丰特斯认为,这正是奥斯汀在2020年至2022年期间出现的状况。他表示,许多本地投资者购买租赁物业,他们清楚这些物业的租金不足以偿还抵押贷款。他们为什么要这样做?丰特斯表示,他们认为奥斯汀房价会继续暴涨,因此尽管他们每个月要支付贷款,但投资依旧能够带来回报。这就是典型的投机行为。

丰特斯对《财富》杂志表示:“随着资金成本[抵押贷款利率]上涨,许多[奥斯汀的]投机者会停止买房。有些投资者陷入困境,有些人减少投资,而有些人每个月依旧要为支持这些房产支付100美元、200美元甚至更多。”

第三,房地产泡沫必须要经历房价下跌。当然,这一点需要根据事实情况进行判断。尽管如此,考虑到奥斯汀房价在短短九个月内已经下跌了两位数,可以说当地市场已经符合这个标准。

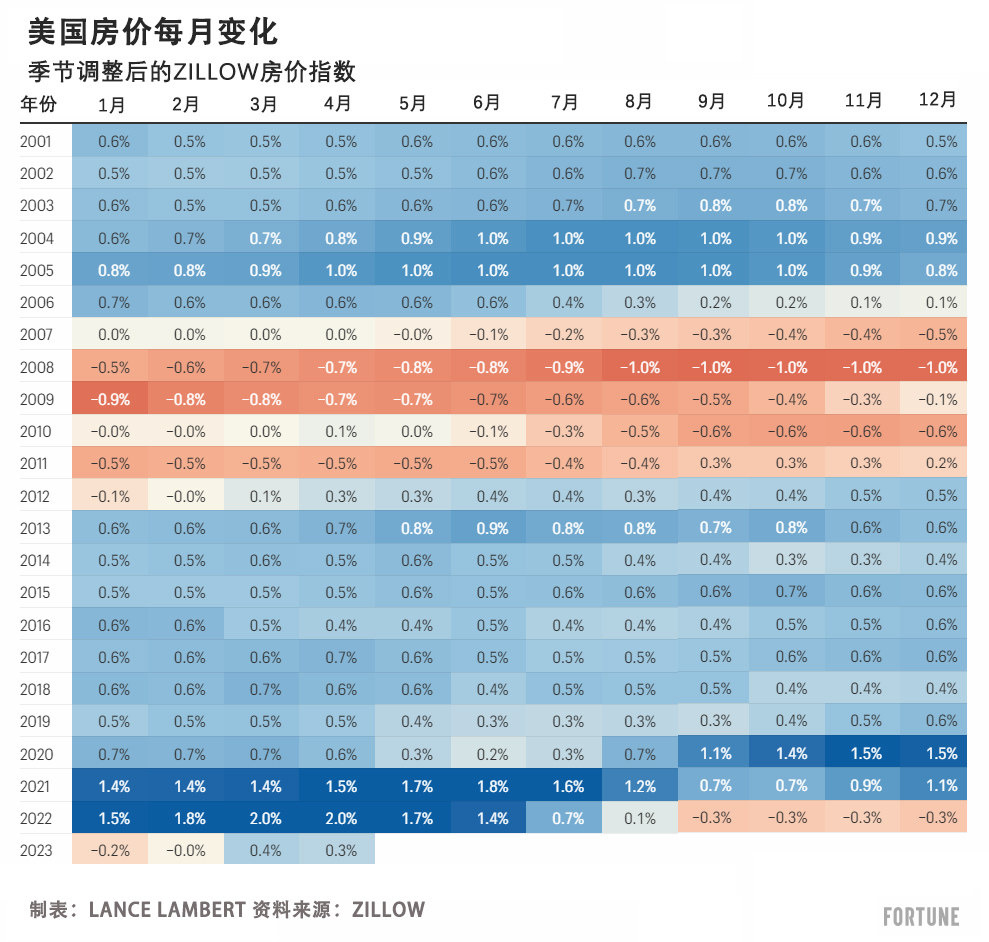

此次房价回调虽然对奥斯汀造成了最严重的冲击,但相对于本世纪初的房地产市场崩溃而言,此次房价回调的幅度不大,并且相对温和。事实上,根据Zillow房价指数判断,美国房价在五个月内持续环比下跌后,3月和4月的房价却在上涨(见下图)。

在全美400个大型房地产市场中,有226个市场在4月份已经恢复到史上最高房价,或者房价刷新历史记录。

在174个房价下跌的市场中,只有38个市场下跌幅度达到或高于5.00%。这些市场大多数位于西部山区、西南部或太平洋沿岸。这些下跌的城市有一个共同的特征,那就是基本面紧张,尤其是本地房价和租金差值高于平均水平。

未来奥斯汀市场将如何变化?这一点很难说。

穆迪分析估计,德克萨斯州大都市区奥斯汀-朗德罗克-乔治城在当前周期房价从最高点到最低点的下跌幅度为-17.9%,包括2023年第二季度至2024年第二季度之间将下跌-8.8%。然而,Zillow的预测模型显示,奥斯汀房价在2023年4月至2024年4月期间将反弹+2.2%。

奥斯汀市场面临的最大问题是基本面问题。穆迪分析认为,2023年第一季度,奥斯汀房价依旧“被高估”36.6%(尽管较2022年第一季度“被高估”63.7%已经大幅下降)。其次,据Realtor.com统计,奥斯汀房屋库存持续增加,5月挂牌数量同比增长了112%。

然而,奥斯汀确实有一些长期利好消息,可能让持续回调具有挑战性。最重要的是,奥斯汀依旧是科技工作者和雇主们逃避高税负的热门目的地。

要知道,虽然奥斯汀房价去年小幅下跌,但依旧比2020年3月上涨了42.6%。奥斯汀的大多数业主都有大量房屋资产净值。(财富中文网)

翻译:刘进龙

审校:汪皓

本世纪初,随着房价上涨,炒房客们纷纷押注快速上涨的阳光地带市场,如凤凰城、拉斯维加斯和迈阿密等。投机者往往希望通过炒房获利,他们认为人口密集的阳光地带市场风险最低,却能带来最高的回报。当然,事实证明他们大错特错,因为这些市场繁荣变成了最严重的房地产泡沫。泡沫最终破灭,并引发了金融危机。

相对而言,本世纪初的阳光地带房地产市场崩溃只有一个例外,那就是孤星州德克萨斯。奥斯汀和达拉斯等市场从房价最高点到最低点分别仅下跌了8.5%和10.5%,而Zillow房价指数(Zillow Home Value Index,ZHVI)跟踪的房价显示,从2007年左右到2012年左右,拉斯维加斯、凤凰城和迈阿密从房价最高点到最低点的跌幅分别高达63.9%、56.4%和52.2%。

虽然在2005年左右,全美积极的贷款机构纷纷允许借款人以极低的首付申请按揭,但德克萨斯却继续采取保守的贷款政策。更严格的贷款法律帮助德克萨斯州躲过了本世纪初的房地产市场崩溃,而且据德州农工大学(Texas A&M)的研究人员表示,这些法律还减少了“止赎的数量”。

时间来到2023年,德克萨斯州有一个城市成为疫情期间的房地产繁荣和房地产回调的中心,它就是奥斯汀。

事实上,Zillow房价指数显示,从2022年7月至2023年4月,奥斯汀的房价下跌了10.02%,是同期全美房价下跌幅度(1%)的10倍。这是全美400个大型房地产市场到目前为止的最大跌幅,超过了旧金山(-10%)、俄勒冈州班德(-9.5%)和博伊西(-9.3%)。

当全美大多数市场的房价几乎没有下跌时,为什么奥斯汀会受到如此严重的冲击?首先,奥斯汀市场泡沫化严重。

理论上,房地产泡沫需要具备三个条件。

第一,房地产泡沫需要房价被严重高估,这意味着本地房价远高于本地收入历史上能够支撑的房价。奥斯汀在疫情期间的房地产繁荣中就发生了这样的情况。事实上,据穆迪分析(Moody's Analytics)统计,在2022年第一季度房价最高时,奥斯汀的房价“被高估”63.7%。穆迪认为,这个比例只要高于25%就属于“被严重高估”。

第二,房地产泡沫需要有投机者。虽然这一点很难量化,但它通常表现为投资者的过度扩张。奥斯汀资深房地产中介和房地产投资人西恩·丰特斯认为,这正是奥斯汀在2020年至2022年期间出现的状况。他表示,许多本地投资者购买租赁物业,他们清楚这些物业的租金不足以偿还抵押贷款。他们为什么要这样做?丰特斯表示,他们认为奥斯汀房价会继续暴涨,因此尽管他们每个月要支付贷款,但投资依旧能够带来回报。这就是典型的投机行为。

丰特斯对《财富》杂志表示:“随着资金成本[抵押贷款利率]上涨,许多[奥斯汀的]投机者会停止买房。有些投资者陷入困境,有些人减少投资,而有些人每个月依旧要为支持这些房产支付100美元、200美元甚至更多。”

第三,房地产泡沫必须要经历房价下跌。当然,这一点需要根据事实情况进行判断。尽管如此,考虑到奥斯汀房价在短短九个月内已经下跌了两位数,可以说当地市场已经符合这个标准。

此次房价回调虽然对奥斯汀造成了最严重的冲击,但相对于本世纪初的房地产市场崩溃而言,此次房价回调的幅度不大,并且相对温和。事实上,根据Zillow房价指数判断,美国房价在五个月内持续环比下跌后,3月和4月的房价却在上涨(见下图)。

在全美400个大型房地产市场中,有226个市场在4月份已经恢复到史上最高房价,或者房价刷新历史记录。

在174个房价下跌的市场中,只有38个市场下跌幅度达到或高于5.00%。这些市场大多数位于西部山区、西南部或太平洋沿岸。这些下跌的城市有一个共同的特征,那就是基本面紧张,尤其是本地房价和租金差值高于平均水平。

未来奥斯汀市场将如何变化?这一点很难说。

穆迪分析估计,德克萨斯州大都市区奥斯汀-朗德罗克-乔治城在当前周期房价从最高点到最低点的下跌幅度为-17.9%,包括2023年第二季度至2024年第二季度之间将下跌-8.8%。然而,Zillow的预测模型显示,奥斯汀房价在2023年4月至2024年4月期间将反弹+2.2%。

奥斯汀市场面临的最大问题是基本面问题。穆迪分析认为,2023年第一季度,奥斯汀房价依旧“被高估”36.6%(尽管较2022年第一季度“被高估”63.7%已经大幅下降)。其次,据Realtor.com统计,奥斯汀房屋库存持续增加,5月挂牌数量同比增长了112%。

然而,奥斯汀确实有一些长期利好消息,可能让持续回调具有挑战性。最重要的是,奥斯汀依旧是科技工作者和雇主们逃避高税负的热门目的地。

要知道,虽然奥斯汀房价去年小幅下跌,但依旧比2020年3月上涨了42.6%。奥斯汀的大多数业主都有大量房屋资产净值。(财富中文网)

翻译:刘进龙

审校:汪皓

As home prices started to boom in the early 2000s, housing speculators doubled down on fast-growing Sun Belt markets like Phoenix, Las Vegas, and Miami. Those speculators, who were often house flippers, assumed high-population Sun Belt markets would provide the best return at the lowest risk. Of course, they were famously wrong, as those booms turned out to be some of the biggest housing bubbles, which ultimately burst and helped spur the financial crisis.

The ’00s Sunbelt housing crash had one, relatively speaking, exception: The Lone Star State. Peak-to-trough, home prices in markets like Austin and Dallas only fell 8.5% and 10.5%, respectively, while house prices tracked by the Zillow Home Value Index (ZHVI) fell 63.9% in Las Vegas, 56.4% in Phoenix, and 52.2% in Miami between their peaks around 2007 and bottoms around 2012.

While zealous lenders across the nation in the mid ’00s were allowing borrowers to take on mortgages without putting much down, Texas stuck with its conservative lending practices. Those tighter lending laws helped the state escape the ’00s housing crash and, according to Texas A&M researchers, limited “the number of foreclosures.”

Fast-forward to 2023, and this time around one pocket of Texas is arguably the epicenter of both the Pandemic Housing Boom and the Pandemic Housing Correction: Austin.

Indeed, between July 2022 and April 2023, Austin home prices as measured by the Zillow Home Value Index have fallen 10.02%—that’s 10 times greater than the national decline (1%) registered by ZHVI during the same time period. That’s the biggest decline, so far, among the nation’s 400 largest housing markets, just beating out San Francisco (-10%), Bend, Ore. (-9.5%), and Boise (-9.3%).

Why is Austin getting hit so hard while much of the country sees little to no correction? For one thing, Austin got bubbly.

In theory, a housing bubble requires three elements.

First, a housing bubble requires steep home price overvaluation—meaning local home prices far exceed what local incomes historically support. That's exactly what occurred in Austin during the Pandemic Housing Boom. In fact, according to Moody's Analytics, Austin home prices were "overvalued" by 63.7% at the height of the boom in the first quarter of 2022. Anything above 25%, Moody's considers "significantly overvalued."

Second, a housing bubble requires speculation. While this one can be challenging to quantify, it usually comes in the form of investors overextending themselves. In the view of Sean Fuentes, a long-time real estate agent and housing investor in Austin, that's exactly what happened in Austin between 2020 and 2022. In his telling, many local investors were buying rental properties which they knew wouldn't yield a rent required to cover the mortgage. Why? Fuentes says they thought that Austin home prices would continue to soar, making the investment fruitful despite the fact they're losing money each month on the mortgage. That's textbook speculation.

"Once the cost of money [mortgage rates] went up, a lot of [Austin] speculators stopped buying," Fuentes tells Fortune. "Some of them are in trouble, some are taking haircuts on their investments, and others are still having to pay $100, $200, or more per month to support the property."

Third, in order to be called a bubble, prices must fall. Of course, this one can only be determined after the fact. That said, given that Austin home prices have fallen double-digits in just nine months, it's fair to say Austin also meets this criteria.

This housing correction, which has hit the hardest in Austin, is mild and tame compared to the '00s housing crash. Indeed, after falling on a month-over-month basis for just five months, U.S. home prices as measured by the Zillow Home Value Index rose in both March and April (see chart below).

Among the nation's 400 largest housing markets, 226 are either back to their all-time home price high or just set a new all-time high in April.

Of the 174 down markets, only 38 are down by 5.00% or more. Most of those markets are either in the Mountain West, Southwest, or along the Pacific Coast. The unifying characteristic among these down markets is strained fundamentals, specifically a wider-than-average gap between local house prices and local rents.

Where will Austin go from here? It's hard to say.

Moody's Analytics estimates that the Austin-Round Rock-Georgetown, Texas metro area will see a -17.9% peak-to-trough house price decline this cycle, including a -8.8% decline between Q2 2023 and Q2 2024. However, Zillow's forecast model is predicting Austin will rebound +2.2% between April 2023 and April 2024.

The biggest headwind still facing Austin is underlying fundamentals. According to Moody's Analytics, Austin was still "overvalued" by 36.6% in Q1 2023 (although down from its peak 63.7% "overvaluation" in Q1 2022). Second, inventory continues to build in Austin, with active listings up 112% year-over-year in May, according to Realtor.com.

However, Austin does have long-term tailwinds that could make a sustained correction challenging. First and foremost, it's still a hot destination for tech workers and employers who are fleeing high-tax states.

Keep in mind that while Austin home values have come down a bit over the past year, they're still up 42.6% since March 2020. Most Austin homeowners have an enormous amount of home equity.

请打开财富Plus APP