为何《财富》美国500强公司收入创纪录利润却大跌?

WILL DANIEL

2023-06-15

利率上浮增加了许多《财富》美国500强公司在2022年的借款成本。

文本设置

文本设置

Plus(0条)

Plus(0条)

每年,我们都能透过《财富》美国500强榜单,了解美国资本主义规模最广泛、影响最深远的趋势。该榜单体现了美国大城市如何争相吸引大公司,介绍了不断变化的促进GDP增长的行业,并分析了从公司合并到科技公司日益强大的主导地位等重塑经济的趋势。

但第69期年度榜单还发现了公司资产负债表存在的一个有趣现象。公司收入创新高,但利润却大幅下降。当前的经济环境充斥着关于美国即将陷入经济衰退的末日预言、商业地产行业的“天启”以及“贪婪性通胀”导致物价暴涨的辩论。在这样的环境下,2022年度的《财富》美国500强榜单能为我们带来一些启示。但它是否预示着美国即将陷入经济衰退,还是将恢复常态?

2020年下半年至2021年,公司利润激增,这引发了备受生活成本上涨折磨的消费者们的愤怒,而去年,公司利润大幅下跌。美联储(Federal Reserve)为了给经济降温和抑制通胀进行加息,这令美国公司普遍难以消化,因此公司的收入创历史纪录,但利润却大幅下降。

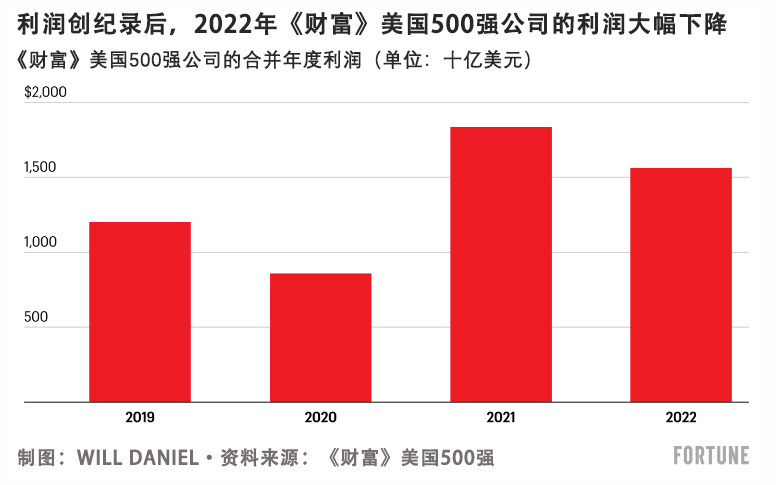

2021年,《财富》美国500强公司收入16.1万亿美元,利润为1.84万亿美元。但去年,虽然公司收入增长至18.1万亿美元,但利润却下降了约15%,只有1.56万亿美元。

出现这种趋势的原因是利率上浮增加了许多《财富》美国500强公司在2022年的借款成本,尽管通货膨胀导致公司物价上涨,但公司的利润空间却不断缩小。随着电商业务增速放缓和重回办公室办公趋势的兴起,困境之下的科技行业利润也大幅下降。虽然大型科技公司依旧在《财富》美国500强榜单上占据主导地位,但2022年,科技公司的利润率下降,其中微软(Microsoft)、Meta、苹果(Apple)、亚马逊(Amazon)和Alphabet等公司的合并年度利润较前一年减少了约770亿美元。仅亚马逊在2022年的净亏损额就达到27亿美元,而其在2021年的净利润为333亿美元。

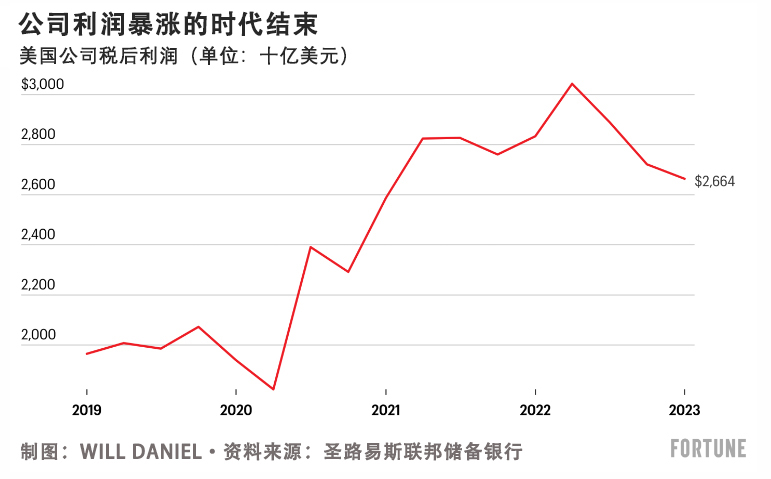

不止《财富》美国500强公司利润下降。圣路易斯联储(St. Louis Federal Reserve)的数据显示,从2022年第二季度的最高点到今年第一季度,美国公司税后利润总额下降了约12%。

尽管在华尔街一致预测美国将陷入经济衰退时,美国公司的利润趋势令人担忧,但《财富》杂志采访的经济学家们认为,这只是在商业周期中发生的公司收益的自然波动,至少目前不必太过担心。

无党派的非盈利研究中心国际法律与经济学中心(International Center for Law & Economics)的首席经济学家布莱恩·阿尔布雷克特对《财富》杂志表示:“公司利润有一个标准的周期性分量。

他表示,尽管存在明显的统计学上的不一致,但“这是正常经济现象”,他认为随着商业周期日益成熟,公司利润只会像往常一样恢复正常趋势。但要真正理解为什么利润下跌,我们必须回溯到三年前疫情所导致的虽然短暂但具有毁灭性的经济衰退。

自然利润周期?

阿尔布雷克特认为,随着经济衰退结束,利润会上涨,因为需求增长,但供应却跟不上需求的变化。这反过来会推高物价,使公司可以提高利润率。

商业情报公司MorningConsult的首席经济学家约翰·利尔解释称,2020年,美国摆脱了疫情导致的经济衰退,当时便出现了这种趋势。他对《财富》杂志表示:“2020年和2021年,企业的观点是:‘目前需求增长,通胀高企而且可能进一步上涨,因此我们一定要相应地定价。’他们可以将上涨的成本全部转嫁给消费者和商户,这会提高利润率。”

但现在,通胀率低于去年6月的四十年最高水平,而且在加息的影响下经济增速放缓,因此利尔表示,我们进入了商业周期中的自然“利润压缩”时期。

他表示:“导致利润增长和下降的因素是相同的。已实现和预期的需求日益疲软,通胀放缓,公司将增加的成本转嫁给消费者的能力下降。”

投行和对冲基金经理不断警告,在加息的影响下,随着经济增速放缓,公司利润可能下降。亿万富翁投资者和对冲基金经理斯坦利·德鲁肯米勒本周表示,他认为公司利润可能进一步下降20%至30%。

利尔和阿尔布雷克特表示,他们也认为今年公司利润会继续下降,但下降幅度不会达到华尔街所预测的水平。

阿尔布雷克特表示:“我认为只有美联储真正把事情搞砸,公司利润才会像人们所预测的那样大幅下降。”他认为,唯一发生这种情景的前提是美联储官员决定继续大幅加息。

利润下降是否预示着美国即将陷入经济衰退?

过去几年,关于经济衰退的预测不绝于耳。经济学家、亿万富翁投资者甚至前美联储官员不断警告,美国经济基础不稳固。尽管有各种悲观的预测,但美国的失业率却接近疫情之前的最低水平,美国GDP持续增长,而且股市刚刚进入了牛市。

依旧有人担心,公司利润下降可能是预示着美国即将陷入经济衰退的更具体的信号。历史上确实有证据表明,在发生经济衰退之前,公司利润会下降,例如在2006年第三季度,公司利润达到了最高水平,但一年多以后的2007年12月,美国正式陷入大衰退。1997年第四季度也发生了类似的状况,两年多以后,互联网泡沫破灭,导致2001年年初美国陷入经济衰退。

法国投资银行兴业银行(Societe Generale)的全球投资策略师阿尔伯特·爱德华兹在周四发表的一份研究报告中表示,“在经济衰退之前通常”确实会发生利润下滑。

他解释称:“在经济周期的最高点,成本上涨导致美国公司利润(和利润率)下降,迫使公司削减投资支出和裁员,进而引发经济衰退。”

然而,爱德华兹认为,所谓“贪婪性通胀”,即公司以新冠疫情、供应链中断和俄乌冲突为借口涨价,而不是因为实际成本上涨而涨价,“使公司可以通过涨价补偿成本上涨和销量增速放缓的影响,从而提高利润率”,这可能推迟了经济衰退发生的时间。

然而,利尔和阿尔布雷克特却坚决反对贪婪性通胀理论。他们认为,2020年和2021年公司利润上涨,只是因为财政和货币刺激政策以及供应链碎片化所导致的供需失衡。

但与爱德华兹的观点一样,阿尔布雷克特表示,2020年末和2021年公司利润大幅上涨,意味着最近的利润下降只是回归趋势,近期内不会发生经济衰退。

他说道:“利润以极快的速度下降确实是经济衰退的标志,但我并不确定当前的利润下降是否符合这个条件。要记住2020年和2021年利润增长的幅度。因此,我对近期的状况并不担心。它们只是在从超高峰值开始下降。或许它们会回落到正常的商业周期水平。”

然而,利尔表示,他认为,从历史经验来看,随着公司利润下降,公司应该着手为经济衰退做好准备,尽管经济衰退并非迫在眉睫的威胁。

他说道:“未来某个时间点会发生经济衰退。就好像你在询问:‘会下雨吗?’当然,最终一定会下雨。我认为,我们真正应该思考的问题是:‘要不要携带雨具?’我认为我们正在接近一个临界点,在未来12个月,经济衰退的概率将足以让公司做好相应的规划。”(财富中文网)

翻译:刘进龙

审校;汪皓

每年,我们都能透过《财富》美国500强榜单,了解美国资本主义规模最广泛、影响最深远的趋势。该榜单体现了美国大城市如何争相吸引大公司,介绍了不断变化的促进GDP增长的行业,并分析了从公司合并到科技公司日益强大的主导地位等重塑经济的趋势。

但第69期年度榜单还发现了公司资产负债表存在的一个有趣现象。公司收入创新高,但利润却大幅下降。当前的经济环境充斥着关于美国即将陷入经济衰退的末日预言、商业地产行业的“天启”以及“贪婪性通胀”导致物价暴涨的辩论。在这样的环境下,2022年度的《财富》美国500强榜单能为我们带来一些启示。但它是否预示着美国即将陷入经济衰退,还是将恢复常态?

2020年下半年至2021年,公司利润激增,这引发了备受生活成本上涨折磨的消费者们的愤怒,而去年,公司利润大幅下跌。美联储(Federal Reserve)为了给经济降温和抑制通胀进行加息,这令美国公司普遍难以消化,因此公司的收入创历史纪录,但利润却大幅下降。

2021年,《财富》美国500强公司收入16.1万亿美元,利润为1.84万亿美元。但去年,虽然公司收入增长至18.1万亿美元,但利润却下降了约15%,只有1.56万亿美元。

出现这种趋势的原因是利率上浮增加了许多《财富》美国500强公司在2022年的借款成本,尽管通货膨胀导致公司物价上涨,但公司的利润空间却不断缩小。随着电商业务增速放缓和重回办公室办公趋势的兴起,困境之下的科技行业利润也大幅下降。虽然大型科技公司依旧在《财富》美国500强榜单上占据主导地位,但2022年,科技公司的利润率下降,其中微软(Microsoft)、Meta、苹果(Apple)、亚马逊(Amazon)和Alphabet等公司的合并年度利润较前一年减少了约770亿美元。仅亚马逊在2022年的净亏损额就达到27亿美元,而其在2021年的净利润为333亿美元。

不止《财富》美国500强公司利润下降。圣路易斯联储(St. Louis Federal Reserve)的数据显示,从2022年第二季度的最高点到今年第一季度,美国公司税后利润总额下降了约12%。

尽管在华尔街一致预测美国将陷入经济衰退时,美国公司的利润趋势令人担忧,但《财富》杂志采访的经济学家们认为,这只是在商业周期中发生的公司收益的自然波动,至少目前不必太过担心。

无党派的非盈利研究中心国际法律与经济学中心(International Center for Law & Economics)的首席经济学家布莱恩·阿尔布雷克特对《财富》杂志表示:“公司利润有一个标准的周期性分量。

他表示,尽管存在明显的统计学上的不一致,但“这是正常经济现象”,他认为随着商业周期日益成熟,公司利润只会像往常一样恢复正常趋势。但要真正理解为什么利润下跌,我们必须回溯到三年前疫情所导致的虽然短暂但具有毁灭性的经济衰退。

自然利润周期?

阿尔布雷克特认为,随着经济衰退结束,利润会上涨,因为需求增长,但供应却跟不上需求的变化。这反过来会推高物价,使公司可以提高利润率。

商业情报公司MorningConsult的首席经济学家约翰·利尔解释称,2020年,美国摆脱了疫情导致的经济衰退,当时便出现了这种趋势。他对《财富》杂志表示:“2020年和2021年,企业的观点是:‘目前需求增长,通胀高企而且可能进一步上涨,因此我们一定要相应地定价。’他们可以将上涨的成本全部转嫁给消费者和商户,这会提高利润率。”

但现在,通胀率低于去年6月的四十年最高水平,而且在加息的影响下经济增速放缓,因此利尔表示,我们进入了商业周期中的自然“利润压缩”时期。

他表示:“导致利润增长和下降的因素是相同的。已实现和预期的需求日益疲软,通胀放缓,公司将增加的成本转嫁给消费者的能力下降。”

投行和对冲基金经理不断警告,在加息的影响下,随着经济增速放缓,公司利润可能下降。亿万富翁投资者和对冲基金经理斯坦利·德鲁肯米勒本周表示,他认为公司利润可能进一步下降20%至30%。

利尔和阿尔布雷克特表示,他们也认为今年公司利润会继续下降,但下降幅度不会达到华尔街所预测的水平。

阿尔布雷克特表示:“我认为只有美联储真正把事情搞砸,公司利润才会像人们所预测的那样大幅下降。”他认为,唯一发生这种情景的前提是美联储官员决定继续大幅加息。

利润下降是否预示着美国即将陷入经济衰退?

过去几年,关于经济衰退的预测不绝于耳。经济学家、亿万富翁投资者甚至前美联储官员不断警告,美国经济基础不稳固。尽管有各种悲观的预测,但美国的失业率却接近疫情之前的最低水平,美国GDP持续增长,而且股市刚刚进入了牛市。

依旧有人担心,公司利润下降可能是预示着美国即将陷入经济衰退的更具体的信号。历史上确实有证据表明,在发生经济衰退之前,公司利润会下降,例如在2006年第三季度,公司利润达到了最高水平,但一年多以后的2007年12月,美国正式陷入大衰退。1997年第四季度也发生了类似的状况,两年多以后,互联网泡沫破灭,导致2001年年初美国陷入经济衰退。

法国投资银行兴业银行(Societe Generale)的全球投资策略师阿尔伯特·爱德华兹在周四发表的一份研究报告中表示,“在经济衰退之前通常”确实会发生利润下滑。

他解释称:“在经济周期的最高点,成本上涨导致美国公司利润(和利润率)下降,迫使公司削减投资支出和裁员,进而引发经济衰退。”

然而,爱德华兹认为,所谓“贪婪性通胀”,即公司以新冠疫情、供应链中断和俄乌冲突为借口涨价,而不是因为实际成本上涨而涨价,“使公司可以通过涨价补偿成本上涨和销量增速放缓的影响,从而提高利润率”,这可能推迟了经济衰退发生的时间。

然而,利尔和阿尔布雷克特却坚决反对贪婪性通胀理论。他们认为,2020年和2021年公司利润上涨,只是因为财政和货币刺激政策以及供应链碎片化所导致的供需失衡。

但与爱德华兹的观点一样,阿尔布雷克特表示,2020年末和2021年公司利润大幅上涨,意味着最近的利润下降只是回归趋势,近期内不会发生经济衰退。

他说道:“利润以极快的速度下降确实是经济衰退的标志,但我并不确定当前的利润下降是否符合这个条件。要记住2020年和2021年利润增长的幅度。因此,我对近期的状况并不担心。它们只是在从超高峰值开始下降。或许它们会回落到正常的商业周期水平。”

然而,利尔表示,他认为,从历史经验来看,随着公司利润下降,公司应该着手为经济衰退做好准备,尽管经济衰退并非迫在眉睫的威胁。

他说道:“未来某个时间点会发生经济衰退。就好像你在询问:‘会下雨吗?’当然,最终一定会下雨。我认为,我们真正应该思考的问题是:‘要不要携带雨具?’我认为我们正在接近一个临界点,在未来12个月,经济衰退的概率将足以让公司做好相应的规划。”(财富中文网)

翻译:刘进龙

审校;汪皓

Every year, the Fortune 500 offers a snapshot of what the biggest and mightiest in American capitalism are up to. The list captures how the nation’s largest cities battle to draw in big business, reveals the ever-changing industries that are driving GDP growth, and unearths trends that are reinventing the economy, from corporate consolidation to tech’s increasing dominance.

But the 69th annual list also uncovered a funny thing on corporate balance sheets. Revenues hit a record high, but profits fell—by a lot. Amid an economic climate full of doom-mongering about a coming recession, a commercial real estate “apocalypse,” and a debate about “greedflation” being the reason for soaring prices, the Fortune 500 snapshot from 2022 is trying to tell us something. But is it a sign of an imminent recession or is this just a return to normal?

After corporate profits surged in the second half of 2020 and throughout 2021, sparking outrage from consumers struggling to cope with rising cost of living, things took a bearish turn last year. The Federal Reserve jacked up interest rates to slow the economy and fight inflation, leaving the corporate sector with a spate of indigestion, as companies raked in record revenues, but profits tanked.

In 2021, Fortune 500 companies earned $1.84 trillion in profits on $16.1 trillion in revenue. But last year, although revenue rose to $18.1 trillion, profits dropped roughly 15% to $1.56 trillion.

The trend came as rising interest rates increased borrowing costs for many Fortune 500 companies during the year, helping to chip away at margins even as inflation allowed for higher prices. The ailing tech sector also saw its profits sink sharply amid the e-commerce slowdown and return to office trend. Although big tech companies continue to dominate the Fortune 500, 2022 was a down year in terms of margins, which caused the combined annual profit of Microsoft, Meta, Apple, Amazon, and Alphabet to fall roughly $77 billion compared to the year before. Amazon alone contributed a net loss of $2.7 billion in 2022, compared to a net profit of $33.3 billion in 2021.

It’s not just Fortune 500 companies that are experiencing falling profits, either. Total after-tax U.S. corporate profits fell roughly 12% between their peak in the second quarter of 2022 and the first quarter of this year, according to data from the St. Louis Federal Reserve.

Still, despite the worrying profit trend, which comes amid consistent recession predictions from Wall Street, economists interviewed by Fortune argued it is merely an example of the natural ebbs and flows that occur in earnings during business cycles and we shouldn’t be too concerned—at least for now.

“There’s a standard cyclical component to profits,” Brian Albrect, chief economist at the International Center for Law & Economics, a non-profit, non-partisan research center, told Fortune.

Despite the jarring statistical incongruity, he said, “this is business as usual for the economy,” arguing that corporate profits are returning to trend, just like they typically do as business cycles mature. But to really understand why profits are falling you have to rewind to the brief but devastating recession caused by the pandemic just three years ago.

The natural profit cycle?

Profits tend to rise as economies come out of recessions, according to Albrecht, because demand increases and supply can’t keep up. That, in turn, drives up prices and enables corporations to increase margins.

John Leer, chief economist at the business intelligence firm MorningConsult, explained that this is exactly what happened as the U.S. emerged from the pandemic-induced recession in 2020. “In 2020 and 2021, you had companies out there saying, ‘We’re in a period of elevated demand, inflation is high, it’s likely to go higher, let’s make sure we set our prices accordingly.’ And they were able to pass along all those elevated costs to consumers and to businesses, which drove margins [higher],” he told Fortune.

Now though, with inflation falling from its four-decade high in June of last year, and economic growth slowing under the weight of higher interest rates, Leer says we’re headed towards the natural “margin compression” period of the business cycle.

“And that’s driven by the same things that made the profits go up, coming down,” he said. “You’ve got weaker demand, realized and expected, you’ve got slower inflation, realized and expected, and less ability for businesses to pass along elevated costs to consumers.”

Investment banks and hedge funders have consistently warned about the potential for profits to drop as the economy slows under the weight of rising interest rates. The billionaire investor and hedge funder Stanley Druckenmiller said just this week that he believes corporate profits could fall another 20% to 30%.

Both Leer and Albrecht said they also believe profits will continue to sink this year, but not to the extent that many forecasters on Wall Street are claiming.

“I think it would take a real mess-up from the Fed to get that kind of drop in profits,” Albrecht said, arguing that scenario is only likely if Fed officials decide to jack up rates dramatically from here.

Are fading profits a sign of an imminent recession?

There’s been no shortage of recession forecasts over the past few years. Economists, billionaire investors, and even former Federal Reserve officials have all repeatedly warned that the U.S. economy is on shaky ground. But despite the pessimistic predictions, the unemployment rate is stuck near pre-pandemic lows, U.S. GDP continues to rise, and stocks just entered a bull market.

Still, some fear that fading corporate profits could be a more concrete sign that a recession is coming soon. And there’s certainly evidence that corporate profit declines have preceded recessions in the past—they peaked in the third quarter of 2006, for example, more than a year before the Great Recession officially began in December of 2007. And the same thing happened in the fourth quarter of 1997, more than two years before the dot-com bubble blow up caused a recession in early 2001.

Albert Edwards, a global strategist at the French investment bank Societe Generale, explained in a Thursday research note that falling profits do “typically precede recessions.”

“Near the top of economic cycles, rising costs result in falling US corporate profits (and profit margins), prompting companies to cut investment spending and jobs, thereby triggering recessions,” he explained.

However, Edwards believes that “greedflation”—the idea that businesses’ used the pandemic, broken supply chains, and the war in Ukraine as an excuse to raise prices more than their costs actually increased—may be delaying the onset of the recession “by allowing companies to more than compensate for higher costs and slowing volumes through unprecedented hikes in prices and thus expanded margins.”

Both Leer and Albrecht, however, stand firmly against the Greedflation theory. They believe the rise of profits in 2020 and 2021 was purely a result of supply and demand imbalances in an economy that was flooded with fiscal and monetary stimulus while supply chains were fractured.

But, like Edwards, Albrecht noted that corporate profits’ sharp rise in late 2020 and 2021 could mean that the recent drop in profits is merely a return to trend, and a recession isn’t imminent.

“Very rapidly falling profits are a sign of recession, but I don’t know if this qualifies as that. You have to remember exactly how dramatic the profit rise was in 2020 and ‘21. So I’m not immediately concerned. They’re falling from that extreme peak. Maybe they’re just falling back to the normal business cycle setup,” he said.

Leer, however, said that he believes businesses should start planning for a recession amid falling corporate profits based on this history, even if it isn’t an imminent threat.

“There will be a recession at some point. It’s like asking, ‘Is it gonna rain?’” he said. “Well, eventually, yes, it’ll rain.? I think the real question is, ‘Should you bring your rain gear?’ And I think we’re headed to that spot where the probability of a recession over the next 12 months is high enough where it makes sense for businesses to start planning accordingly.”

请打开财富Plus APP