英特尔首席执行官离职,公司未来仍然极度不明朗

David Meyer

2024-12-06

英特尔亟需解决的根本问题是明确自身的定位。

文本设置

文本设置

Plus(0条)

Plus(0条)

英特尔从昔日无可匹敌的行业领导者跌落至现今每况愈下、方向迷失的境地,其中的失误与误判不胜枚举。然而,在本周首席执行官突然离职之后,英特尔正在探寻前行的方向,它亟需解决的根本问题是明确自身的定位,以及作为芯片制造商的真正优势所在。

这家拥有56年历史的半导体公司是同行业中最后一家既能自行设计芯片又能自行生产芯片的公司——多年来,这一强大的组合为英特尔带来了技术和财务上的双重优势。然而,随着市场的变化,这种模式已不再奏效,英特尔一直在努力调整以适应新变化。据业内专家称,首席执行官帕特·格尔辛格发现自己陷入了利益冲突的困境,难以推销公司的重组计划。

本周一格尔辛格突然“退休”后,多家媒体报道称,董事会对公司扭转亏损的进展感到不满,迫使他离职。

分析师认为,这一决定可能会对英特尔造成困扰,因为英特尔面临的核心挑战——身份认同危机仍未得到解决,并将继续对公司的业务运营和战略部署产生深远影响。

华尔街可能也持类似观点——英特尔的股价最初可能会因格尔辛格离职的消息而上涨,但随着这一变动所带来的连锁反应逐渐显现,周二股价下跌逾6%。

丹麦咨询公司Semiconductor Business Intelligence的分析师克劳斯·阿斯霍尔姆(Claus Aasholm)说:“解雇帕特·格尔辛格将带来巨大损失,可能会让英特尔一蹶不振。”

代工厂的雄心

英特尔在很多方面都出现了问题,比如在智能手机市场错失良机,在由英伟达(Nvidia)主导的人工智能芯片市场也处于落后地位。但核心问题在于英特尔的制造部门——英特尔晶圆代工厂。

2021年,当格尔辛格重返英特尔担任首席执行官时——他曾在英特尔工作了30年,后于2009年离开英特尔,先后在EMC(总裁兼首席运营官)和VMware(首席执行官)任职——这家美国芯片行业的标志性企业已经陷入困境。

英特尔的营业利润正在下滑;竞争对手AMD正从其个人电脑和数据中心业务中抢夺市场份额;就Mac产品线而言,苹果公司(Apple)最近决定从英特尔的x86架构处理器转向自研的基于ARM架构的芯片;英特尔也在努力升级其制造工艺,以赶上台积电(TSMC)和三星(Samsung)等公司的步伐。离任的首席执行官司睿博(Bob Swan)是一名财务出身的高管,而格尔辛格是一名深受欢迎的工程师。他的回归在英特尔内外都获得了积极反响。

格尔辛格为英特尔提出的扭亏为盈的宏伟蓝图包括在美国和欧洲新建更多工厂,力图使其转型为一家成功的合约芯片制造商,同时保持自行设计与制造处理器的业务模式。

出于以下几个原因,这是极具野心的想法。首先,英特尔在推进先进制造工艺方面的滞后已是业界周知的事实;台积电无论过去还是现在,都是备受推崇的合作伙伴。其次,英特尔合约制造业务需要的大客户对将知识产权交由英特尔的芯片设计业务运用持审慎态度(合乎情理)——这也是在先进芯片制造领域唯一能与台积电匹敌的三星经历过的信任问题。

因此,格尔辛格及其团队不得不对公司进行反复重组,以确保设计与制造业务的分离更具战略意义。重组在9月份画上句号,当时英特尔宣布,其代工厂将成为母公司旗下的独立子公司。

与时间赛跑

英特尔代工厂今年即将推出(但却迟迟未推出)的18A芯片制造工艺赢得了两大知名客户——微软(Microsoft)和亚马逊(Amazon)都已签约,将由该公司为其生产定制芯片,——但这两笔交易的规模远不足以维持这项业务的可持续发展。该部门今年第三季度的运营亏损高达58亿美元,收入下降了8%。

然而,阿斯霍尔姆认为格尔辛格在管理代工厂计划时表现出了“高超的政治和财务驾驭能力”,即使“英特尔的制造能力过去和现在都未能达到预期”。

这位前首席执行官在这方面最突出的成就是根据《芯片和科学法案》(CHIPS Act)为英特尔争取到了高达78.6亿美元的美国政府资金支持,该法案是拜登政府为避免过度依赖台湾而大力推动的重建美国芯片制造能力的法案。(英特尔公司本应再获得6亿美元的资助,但由于英特尔还赢得了一份价值30亿美元的美国军方合同,并将其在美国的中期投资计划缩减了10%,因此资助金额有所减少。)

格尔辛格还达成了两项巨额交易,外部资产管理公司为关键工厂扩展投入了大量现金。在第一个例子中,英特尔和布鲁克菲尔德资产管理公司(Brookfield Asset Management)于2022年达成协议,共同投资高达300亿美元,用于英特尔在亚利桑那州钱德勒新建工厂。今年,阿波罗全球管理公司(Apollo Global Management)也与英特尔达成了类似的协议,向其位于爱尔兰莱克斯利普的新Fab 34晶圆厂投资110亿美元。在这两个案例中,资产管理公司均获得了合资企业49%的股份,而英特尔则保留了51%的控股权。

阿斯霍尔姆告诉《财富》杂志,格尔辛格“虽然还没有筹集到全部资金,但已将一大笔资金收入囊中。”

花旗(Citi)分析师克里斯托弗·丹利(Christopher Danely)在格尔辛格离职后的周一报告中写道:“我们……相信格尔辛格已经开始扭转公司局面。在他加入时,英特尔在技术上比台积电/AMD落后了近两年,现在有望在2025年底追平——在我们看来,这无疑是一项非凡的成就。”

随着18A制造工艺将于明年投入使用——英特尔第三季度的亏损达到创纪录的166亿美元,同时今年有1.5万名员工遭到解雇——这位首席执行官似乎正在奋力驶过一座快速倒塌的桥梁。

他未能做到。现在的问题是英特尔能否做到。

未来之路

彻底摆脱代工厂显然是大势所趋。

就在格尔辛格被解职的几周前,四位英特尔前董事在《财富》杂志的专栏文章中提出了这一主张。他们认为,“在英特尔现有的公司架构下,其代工业务几乎没有成功的可能”,因为英特尔“未能证明其能够有效运营代工业务”,而且前面提及的英伟达和博通(Broadcom)等潜在客户也对英特尔缺乏信任。

花旗的丹利在报告中称:“我们认为,英特尔若能放弃转型为商业晶圆代工厂,将更符合股东的最大利益。鉴于代工厂计划的拥护者格尔辛格离职,我们认为放弃转型的可能性更大。”他补充道:“在理想情况下,格尔辛格会留下来,公司将逐步退出晶圆代工厂业务。”美国银行(Bank of America)的分析师也表示,目前拆分业务的可能性更大了。

然而,这一转型之路存在重大障碍。根据《芯片和科学法案》,美国政府对英特尔的资助条款明确了一项条件:如果代工厂被拆分,导致英特尔丧失对其的控制权,那么除非美国商务部改变立场,否则资金将无法到位。(实际上,若第三方获得了英特尔的全面控制权,同样的情况也会发生。尽管高通最近曾表现出收购英特尔的意向,但据报道,鉴于收购的复杂性,高通已不再对收购抱有兴趣。)

还有那些与资产管理公司的交易。阿斯霍尔姆表示:"按照目前的运营利润分配模式,[英特尔代工服务]难以吸引买家,甚至无法出售。与布鲁克菲尔德和阿波罗的两项交易都依赖英特尔利用其代工业务生产产品。英特尔必须在出售代工业务之前使其实现盈利。”

阿斯霍尔姆对格尔辛格被解职的解释是——他并未声称了解内幕,英特尔也拒绝置评——这位首席执行官是公司内部长期权力斗争的牺牲品。这场斗争的一方是负责英特尔传统x86个人电脑处理器业务的客户端计算事业部,而另一方是其他所有人。

他说:“纵观历史,英特尔虽创新颇多,却鲜有耐心走完最后一英里。”他指的是英特尔在2019年将其移动设备业务出售给苹果,并于翌年将存储芯片业务转让给海力士(SK Hynix)。“问题的症结在于,与英特尔的客户端计算事业部相比,这些新计划似乎总是黯然失色,且无一例外地遭到了遗弃。”

英特尔新任临时联席首席执行官之一是米歇尔·约翰斯顿·霍尔特豪斯(Michelle Johnston Holthaus),她在过去几年中一直负责客户端计算事业部业务。(另一位是首席财务官大卫·津斯纳(David Zinsner)。)阿斯霍尔姆说:"在英特尔近期历史中,客户端计算事业部管理层相较于公司高层拥有更大的实权。客户端计算事业部再次取得了胜利。”

至于格尔辛格的永久继任者,美国全国广播公司财经频道(CNBC)和路透社都报道称,英特尔正在寻找外部候选人。

美满科技集团(Marvell)首席执行官马特·墨菲(Matt Murphy)和数月前离开英特尔董事会的Cadence Design Systems执行董事长陈立武(Lip-Bu tan)均被列入潜在候选人之列。陈立武离开董事会导致英特尔缺乏在芯片制造领域具有丰富技术经验的人才。据路透社当时报道,陈立武对格尔辛格执行代工战略的方式、内部官僚主义和英特尔滞后的人工智能战略感到失望。

丹利在报告中称:“我们认为帕特是解决英特尔芯片制造问题的最佳首席执行官,同时希望公司退出晶圆代工业务,保留格尔辛格。随着帕特离职,如果新任首席执行官不像帕特那样精通先进半导体制造技术,英特尔持续落后于台积电/AMD的风险可能会进一步加大。”(财富中文网)

译者:中慧言-王芳

英特尔从昔日无可匹敌的行业领导者跌落至现今每况愈下、方向迷失的境地,其中的失误与误判不胜枚举。然而,在本周首席执行官突然离职之后,英特尔正在探寻前行的方向,它亟需解决的根本问题是明确自身的定位,以及作为芯片制造商的真正优势所在。

这家拥有56年历史的半导体公司是同行业中最后一家既能自行设计芯片又能自行生产芯片的公司——多年来,这一强大的组合为英特尔带来了技术和财务上的双重优势。然而,随着市场的变化,这种模式已不再奏效,英特尔一直在努力调整以适应新变化。据业内专家称,首席执行官帕特·格尔辛格发现自己陷入了利益冲突的困境,难以推销公司的重组计划。

本周一格尔辛格突然“退休”后,多家媒体报道称,董事会对公司扭转亏损的进展感到不满,迫使他离职。

分析师认为,这一决定可能会对英特尔造成困扰,因为英特尔面临的核心挑战——身份认同危机仍未得到解决,并将继续对公司的业务运营和战略部署产生深远影响。

华尔街可能也持类似观点——英特尔的股价最初可能会因格尔辛格离职的消息而上涨,但随着这一变动所带来的连锁反应逐渐显现,周二股价下跌逾6%。

丹麦咨询公司Semiconductor Business Intelligence的分析师克劳斯·阿斯霍尔姆(Claus Aasholm)说:“解雇帕特·格尔辛格将带来巨大损失,可能会让英特尔一蹶不振。”

代工厂的雄心

英特尔在很多方面都出现了问题,比如在智能手机市场错失良机,在由英伟达(Nvidia)主导的人工智能芯片市场也处于落后地位。但核心问题在于英特尔的制造部门——英特尔晶圆代工厂。

2021年,当格尔辛格重返英特尔担任首席执行官时——他曾在英特尔工作了30年,后于2009年离开英特尔,先后在EMC(总裁兼首席运营官)和VMware(首席执行官)任职——这家美国芯片行业的标志性企业已经陷入困境。

英特尔的营业利润正在下滑;竞争对手AMD正从其个人电脑和数据中心业务中抢夺市场份额;就Mac产品线而言,苹果公司(Apple)最近决定从英特尔的x86架构处理器转向自研的基于ARM架构的芯片;英特尔也在努力升级其制造工艺,以赶上台积电(TSMC)和三星(Samsung)等公司的步伐。离任的首席执行官司睿博(Bob Swan)是一名财务出身的高管,而格尔辛格是一名深受欢迎的工程师。他的回归在英特尔内外都获得了积极反响。

格尔辛格为英特尔提出的扭亏为盈的宏伟蓝图包括在美国和欧洲新建更多工厂,力图使其转型为一家成功的合约芯片制造商,同时保持自行设计与制造处理器的业务模式。

出于以下几个原因,这是极具野心的想法。首先,英特尔在推进先进制造工艺方面的滞后已是业界周知的事实;台积电无论过去还是现在,都是备受推崇的合作伙伴。其次,英特尔合约制造业务需要的大客户对将知识产权交由英特尔的芯片设计业务运用持审慎态度(合乎情理)——这也是在先进芯片制造领域唯一能与台积电匹敌的三星经历过的信任问题。

因此,格尔辛格及其团队不得不对公司进行反复重组,以确保设计与制造业务的分离更具战略意义。重组在9月份画上句号,当时英特尔宣布,其代工厂将成为母公司旗下的独立子公司。

与时间赛跑

英特尔代工厂今年即将推出(但却迟迟未推出)的18A芯片制造工艺赢得了两大知名客户——微软(Microsoft)和亚马逊(Amazon)都已签约,将由该公司为其生产定制芯片,——但这两笔交易的规模远不足以维持这项业务的可持续发展。该部门今年第三季度的运营亏损高达58亿美元,收入下降了8%。

然而,阿斯霍尔姆认为格尔辛格在管理代工厂计划时表现出了“高超的政治和财务驾驭能力”,即使“英特尔的制造能力过去和现在都未能达到预期”。

这位前首席执行官在这方面最突出的成就是根据《芯片和科学法案》(CHIPS Act)为英特尔争取到了高达78.6亿美元的美国政府资金支持,该法案是拜登政府为避免过度依赖台湾而大力推动的重建美国芯片制造能力的法案。(英特尔公司本应再获得6亿美元的资助,但由于英特尔还赢得了一份价值30亿美元的美国军方合同,并将其在美国的中期投资计划缩减了10%,因此资助金额有所减少。)

格尔辛格还达成了两项巨额交易,外部资产管理公司为关键工厂扩展投入了大量现金。在第一个例子中,英特尔和布鲁克菲尔德资产管理公司(Brookfield Asset Management)于2022年达成协议,共同投资高达300亿美元,用于英特尔在亚利桑那州钱德勒新建工厂。今年,阿波罗全球管理公司(Apollo Global Management)也与英特尔达成了类似的协议,向其位于爱尔兰莱克斯利普的新Fab 34晶圆厂投资110亿美元。在这两个案例中,资产管理公司均获得了合资企业49%的股份,而英特尔则保留了51%的控股权。

阿斯霍尔姆告诉《财富》杂志,格尔辛格“虽然还没有筹集到全部资金,但已将一大笔资金收入囊中。”

花旗(Citi)分析师克里斯托弗·丹利(Christopher Danely)在格尔辛格离职后的周一报告中写道:“我们……相信格尔辛格已经开始扭转公司局面。在他加入时,英特尔在技术上比台积电/AMD落后了近两年,现在有望在2025年底追平——在我们看来,这无疑是一项非凡的成就。”

随着18A制造工艺将于明年投入使用——英特尔第三季度的亏损达到创纪录的166亿美元,同时今年有1.5万名员工遭到解雇——这位首席执行官似乎正在奋力驶过一座快速倒塌的桥梁。

他未能做到。现在的问题是英特尔能否做到。

未来之路

彻底摆脱代工厂显然是大势所趋。

就在格尔辛格被解职的几周前,四位英特尔前董事在《财富》杂志的专栏文章中提出了这一主张。他们认为,“在英特尔现有的公司架构下,其代工业务几乎没有成功的可能”,因为英特尔“未能证明其能够有效运营代工业务”,而且前面提及的英伟达和博通(Broadcom)等潜在客户也对英特尔缺乏信任。

花旗的丹利在报告中称:“我们认为,英特尔若能放弃转型为商业晶圆代工厂,将更符合股东的最大利益。鉴于代工厂计划的拥护者格尔辛格离职,我们认为放弃转型的可能性更大。”他补充道:“在理想情况下,格尔辛格会留下来,公司将逐步退出晶圆代工厂业务。”美国银行(Bank of America)的分析师也表示,目前拆分业务的可能性更大了。

然而,这一转型之路存在重大障碍。根据《芯片和科学法案》,美国政府对英特尔的资助条款明确了一项条件:如果代工厂被拆分,导致英特尔丧失对其的控制权,那么除非美国商务部改变立场,否则资金将无法到位。(实际上,若第三方获得了英特尔的全面控制权,同样的情况也会发生。尽管高通最近曾表现出收购英特尔的意向,但据报道,鉴于收购的复杂性,高通已不再对收购抱有兴趣。)

还有那些与资产管理公司的交易。阿斯霍尔姆表示:"按照目前的运营利润分配模式,[英特尔代工服务]难以吸引买家,甚至无法出售。与布鲁克菲尔德和阿波罗的两项交易都依赖英特尔利用其代工业务生产产品。英特尔必须在出售代工业务之前使其实现盈利。”

阿斯霍尔姆对格尔辛格被解职的解释是——他并未声称了解内幕,英特尔也拒绝置评——这位首席执行官是公司内部长期权力斗争的牺牲品。这场斗争的一方是负责英特尔传统x86个人电脑处理器业务的客户端计算事业部,而另一方是其他所有人。

他说:“纵观历史,英特尔虽创新颇多,却鲜有耐心走完最后一英里。”他指的是英特尔在2019年将其移动设备业务出售给苹果,并于翌年将存储芯片业务转让给海力士(SK Hynix)。“问题的症结在于,与英特尔的客户端计算事业部相比,这些新计划似乎总是黯然失色,且无一例外地遭到了遗弃。”

英特尔新任临时联席首席执行官之一是米歇尔·约翰斯顿·霍尔特豪斯(Michelle Johnston Holthaus),她在过去几年中一直负责客户端计算事业部业务。(另一位是首席财务官大卫·津斯纳(David Zinsner)。)阿斯霍尔姆说:"在英特尔近期历史中,客户端计算事业部管理层相较于公司高层拥有更大的实权。客户端计算事业部再次取得了胜利。”

至于格尔辛格的永久继任者,美国全国广播公司财经频道(CNBC)和路透社都报道称,英特尔正在寻找外部候选人。

美满科技集团(Marvell)首席执行官马特·墨菲(Matt Murphy)和数月前离开英特尔董事会的Cadence Design Systems执行董事长陈立武(Lip-Bu tan)均被列入潜在候选人之列。陈立武离开董事会导致英特尔缺乏在芯片制造领域具有丰富技术经验的人才。据路透社当时报道,陈立武对格尔辛格执行代工战略的方式、内部官僚主义和英特尔滞后的人工智能战略感到失望。

丹利在报告中称:“我们认为帕特是解决英特尔芯片制造问题的最佳首席执行官,同时希望公司退出晶圆代工业务,保留格尔辛格。随着帕特离职,如果新任首席执行官不像帕特那样精通先进半导体制造技术,英特尔持续落后于台积电/AMD的风险可能会进一步加大。”(财富中文网)

译者:中慧言-王芳

The list of mistakes and miscalculations that turned Intel from an unbeatable industry titan into its current ailing and rudderless state is a long one. But as the company seeks a path forward following the abrupt exit of its CEO this week, the fundamental problem Intel needs to resolve comes down to its very identity, and to questions about where its true strengths lie, as a chip company.

The 56-year-old semiconductor company is among the last of its kind to both design its own chips and manufacture them—a powerful combination that for years gave Intel a technological and financial edge. With changes in the market making that model less viable though, Intel has struggled to adapt. And CEO Pat Gelsinger, according to industry experts, found himself caught between competing interests, unable to sell his plan for remaking the company.

After Gelsinger abruptly “retired” on Monday, multiple outlets reported that the board had become impatient with the company’s turnaround progress and forced him out.

That decision could come to haunt Intel, analysts suggest, since the identity crisis at the heart of Intel’s challenges remains unresolved and will continue to have a big impact on the company’s business and whatever strategy it chooses to pursue.

Wall Street may have the same idea—Intel’s share price may have initially jumped on news of Gelsinger’s exit, but it fell by more than 6% on Tuesday as the implications sunk in.

“Axing Pat Gelsinger is a massive loss and could cost Intel its life,” said Claus Aasholm, an analyst at Denmark’s Semiconductor Business Intelligence consultancy.

Foundry ambitions

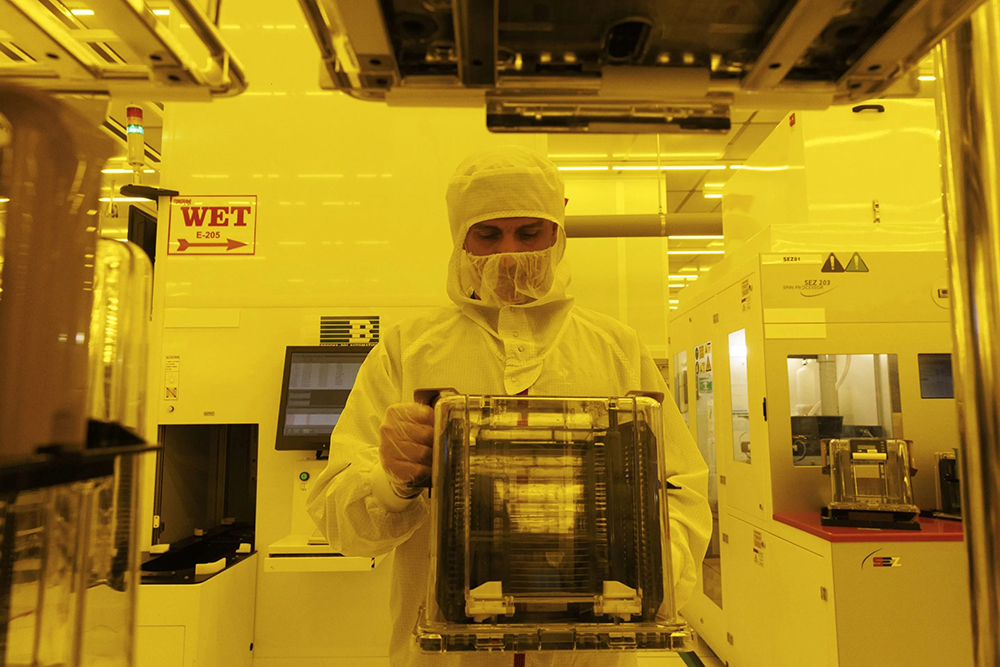

Plenty has gone wrong at Intel, which missed the boat on smartphones and is an also-ran in the Nvidia-dominated AI chip space. But the core issue in this affair is Intel Foundry, the company’s manufacturing arm.

When Gelsinger returned to Intel as CEO in 2021—he had served 30 years at the company before leaving in 2009 for stints at EMC (president and chief operating officer) and VMware (CEO)—the U.S. chip icon was already in trouble.

Chip manufacturing facilities have been one of Intel’s long-term advantages—and are at the heart of its current identity crisis.

Kobi Wolf—Bloomberg/Getty Images

Its operating profits were slipping; rival AMD was taking market share from its PC and data center businesses; Apple had recently decided to switch from Intel’s x86-architecture processors to its own ARM-based chips for its Mac line; and Intel was struggling to upgrade its manufacturing processes to keep up with the likes of Taiwan Semiconductor Manufacturing Co. (TSMC) and Samsung. Outgoing CEO Bob Swan was a finance guy, but Gelsinger was an engineer and a much liked one at that. His return was well received inside and outside Intel.

Gelsinger’s big idea for the Intel turnaround was to build out more factories in the U.S. and Europe and to finally become a successful contract chip manufacturer, as well as designer and maker of its own processors.

This was a hugely ambitious idea for a couple of reasons. Firstly, Intel’s delays in switching to more advanced manufacturing processes were very well publicized; TSMC remained and remains the premium option. Secondly, the big clients that Intel’s contract-manufacturing business needed were understandably wary about letting their intellectual property anywhere near Intel’s own chip-design business—a trust problem that Samsung, the only big rival to TSMC in advanced chip manufacturing, has also experienced.

As a result, Gelsinger and his team had to repeatedly reorganize the company to make the separation of its two sides ever more meaningful. This culminated in September’s announcement that Intel Foundry would become an independent subsidiary business within the mothership.

Race against time

Intel this year won two notable customers for Foundry’s upcoming (and much delayed) 18A chipmaking process—both Microsoft and Amazon have signed up to have the company produce custom chips for them—but neither deal is anywhere near the scale that’s needed to make the business sustainable. The division had an operating loss of $5.8 billion in the third quarter of this year, with revenues down 8%.

However, Aasholm argues that Gelsinger displayed “masterful navigation of the political and financial landscape” in his handling of the Foundry plans, even if “Intel’s manufacturing was and is subpar.”

The erstwhile CEO’s most prominent achievement on this front was the securing of up to $7.86 billion in U.S. government funding under the CHIPS Act, the Biden administration’s big push to rebuild America’s chip-manufacturing prowess as a hedge against overreliance on Taiwan. (It was to have been $600 million more, but the sum was reduced because Intel also won a $3 billion U.S. military contract and scaled back its medium-term U.S. investment plans by 10%.)

But Gelsinger also struck two megadeals that saw external asset managers throw vast amounts of cash at key plant buildouts. In the first example, Intel and Brookfield Asset Management agreed in 2022 to jointly invest up to $30 billion in Intel’s new factories in Chandler, Ariz. A similar deal followed this year, in which Apollo Global Management put $11 billion into Intel’s new Fab 34 plant in Leixlip, Ireland. In each case, the asset manager got 49% of the joint venture and Intel retained a controlling interest of 51%.

Gelsinger “still did not have all the money, but a big chunk was in the bag,” Aasholm told Fortune.

As CEO of Intel, Pat Gelsinger worked to get billions in funding from the Biden administration to manufacture chips in the U.S.

BRENDAN SMIALOWSKI—AFP/Getty Images

“We … believe Gelsinger has begun to right the manufacturing ship,” Citi analyst Christopher Danely wrote in a Monday note following Gelsinger’s ouster. “Intel was almost two years behind TSMC/AMD when he joined and is now poised to draw even … by the end of 2025—a remarkable feat in our opinion.”

With the 18A manufacturing process due to finally come online next year—but with Intel posting a record quarterly loss of $16.6 billion in Q3 and 15,000 workers being shown the door this year—it was as though the CEO was racing to make it over a fast-crumbling bridge.

He didn’t make it. The question now is whether Intel will.

The road ahead

There is clearly momentum behind the idea of getting rid of Foundry altogether.

Four former Intel directors advocated this route in a Fortune op-ed just weeks before Gelsinger’s defenestration. They argued that “an Intel foundry operation, inside Intel’s corporate structure, has little chance of success” because Intel has “failed to prove that it can effectively run a foundry,” and because of the aforementioned lack of trust on the part of potential clients like Nvidia and Broadcom.

“We believe it is in the best interest of Intel shareholders if the company stops trying to be a merchant foundry, and we believe the chance is higher now given Gelsinger was a champion of it,” said Citi’s Danely in his note, adding: “In our ideal world, Gelsinger would stay and foundry goes.” Bank of America’s analysts also said a breakup was now more likely.

But there are significant potential roadblocks in the way. The U.S. government erected one of them in the terms that were attached to Intel’s CHIPS Act funding: If Foundry gets spun off, and Intel loses control of it, bang goes the cash, unless the Department of Commerce has a change of heart. (Indeed, the same result would follow if a third party gained control of Intel as a whole. Qualcomm was sniffing around Intel recently but reportedly lost interest owing to the complexity of a takeover.)

Then there are those deals with the asset management companies. “With the current operating profit split, [Intel Foundry Services] is unsellable,” said Aasholm. “It cannot even be given away. The two deals with Brookfield and Apollo depend on Intel products using IFS. Intel will have to get IFS to profitability before selling it.”

Aasholm’s interpretation of Gelsinger’s ouster—he does not claim insider knowledge, and Intel declined to comment—is that the CEO fell victim to a long-running power struggle within the company. On the one side: the Client Computing Group (CCG), which handles Intel’s traditional x86 PC processor business. On the other: everyone else.

“Historically, Intel has innovated a lot but has never had the patience to go the last mile,” he said, pointing to Intel’s sale of its mobile model business to Apple in 2019, and that of its memory chip business to SK Hynix the following year. “The problem is that these initiatives always look small compared to CCG, and each was abandoned.”

One of Intel’s new interim co-CEOs is Michelle Johnston Holthaus, who has run CCG for the past couple of years. (The other is CFO David Zinsner.) “In Intel’s most recent history, CCG management has been more powerful than senior management itself. And once again, CCG won,” said Aasholm.

As for Gelsinger’s permanent replacement, both CNBC and Reuters report that Intel is looking at external candidates.

Marvell CEO Matt Murphy’s name is in the frame, as is that of Cadence Design Systems executive chair Lip-Bu Tan—who departed Intel’s board just a few months ago, leaving it without anyone with deep technical experience in chip manufacturing. Reuters reported at the time that Tan had been frustrated with the way Gelsinger’s Foundry strategy was being executed, and with internal bureaucracy and Intel’s lagging AI strategy.

“We believe Pat was the best CEO for fixing Intel’s manufacturing and prefer the company exit Foundry and keep Gelsinger,” said Danely in his note. “Now that Pat is gone, the risk increases that Intel could remain behind TSMC/AMD if the new CEO is not as well-versed in advanced semiconductor manufacturing as Pat.”

请打开财富Plus APP