越来越多的美国人拖欠信用卡账单,美国经济亮起了警示灯

JASON MA

2025-01-12

银行信用卡债务冲销达到了2010年以来的最高水平,这对经济而言是一个潜在的警示信号,因为消费者近年来一直在应对通胀压力和借贷成本上升的双重挑战。

文本设置

文本设置

Plus(0条)

Plus(0条)

美国人在偿还信用卡账单方面遭遇重重困难,这迫使贷款机构放弃追讨债务,进而承受更大的损失。

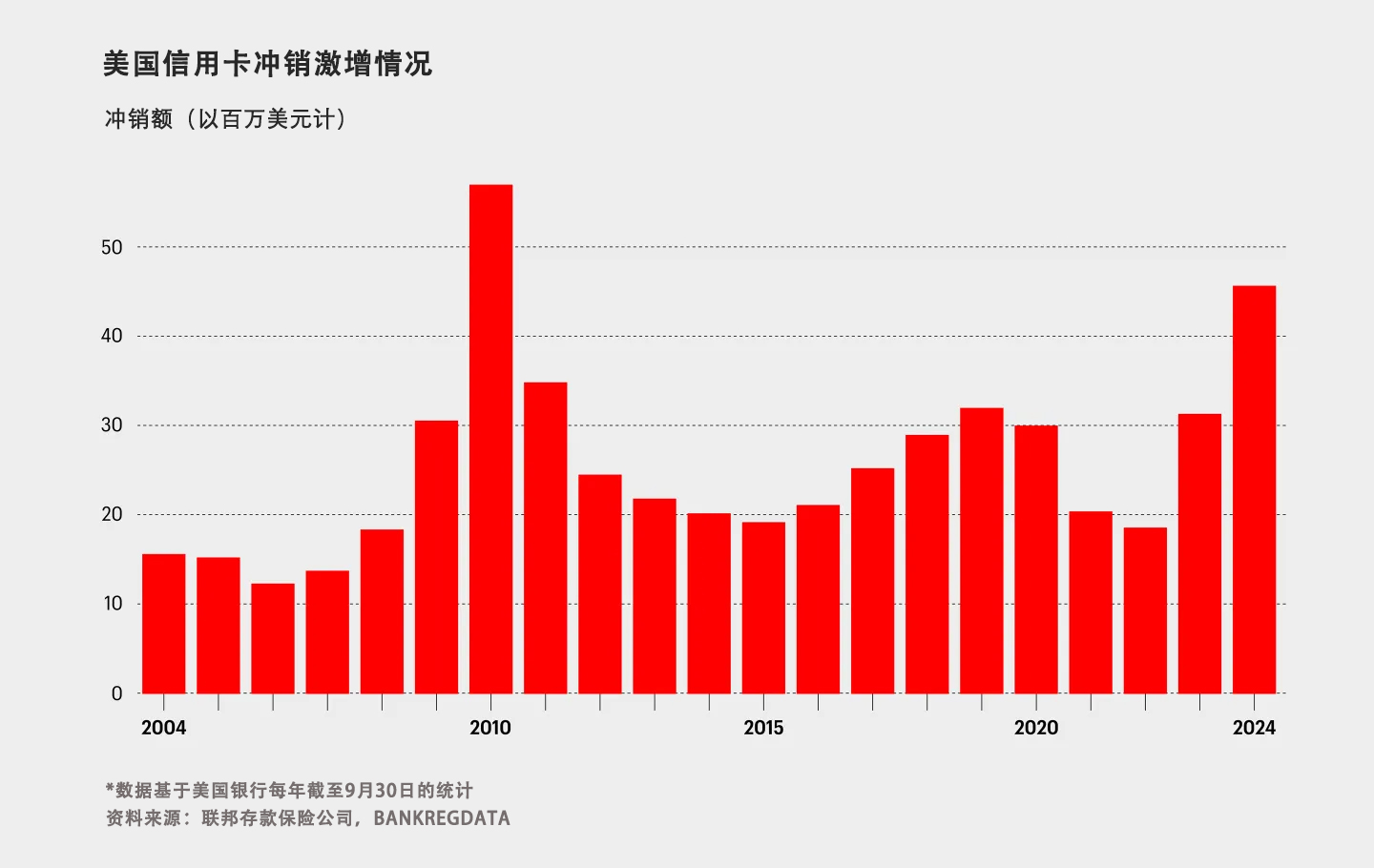

银行信用卡债务冲销达到了2010年以来的最高水平,彼时消费者仍在努力摆脱金融危机和大衰退的影响。

根据BankRegData编制的联邦存款保险公司(FDIC)季度统计数据,截至2024年前三季度,信用卡债务冲销总额达到457亿美元,较上年同期增长46%。

英国《金融时报》最先报道了今年信用卡债务冲销额激增的情况,这对经济而言是一个潜在的警示信号,因为消费者近年来一直在应对通胀压力和借贷成本上升的双重挑战。

第四季度的数据尚未公布,但很可能会显示进一步增长,原因是年底假日购物热潮期间,冲销额通常会有所上升。

纽约联邦储备银行的另一份数据显示,第三季度信用卡余额增加了240亿美元,目前总额为1.17万亿美元,较上年同期增长8.1%。

尽管信用卡的拖欠率从第二季度的9.1%下降到8.8%,但整体消费者债务的拖欠率从3.2%上升至3.5%。

纽约联邦储备银行(New York Fed)经济研究顾问李东勋(Donghoon Lee)上月在一份声明中表示:“尽管名义上家庭余额仍在持续攀升,但收入增长速度超过了债务增长速度。尽管本季度拖欠情况有所缓解,但拖欠率上升仍表明许多家庭承受着压力。”

Capital One等个人发卡机构近期也表示,其信用卡债务冲销率有所上升。

这种压力表明,尽管国内生产总值增长、薪资增长以及个人收入等经济数据均呈现出积极态势,但消费者在疫情期间及其后掀起的大规模购买热潮,如今正逐渐给他们带来沉重负担。

通胀率已从2022年9%的高位大幅降至11月的2.7%,但物价仍高于疫情前的水平。

与此同时,尽管政策制定者今年已开始下调基准利率,但美联储此前大幅上调基准利率(对信用卡利率产生了影响)所带来的影响仍在持续。

据英国《金融时报》报道,在截至9月份的12个月里,那些未能全额偿还月度信用卡账单的消费者支付了1700亿美元的利息。

消费者的压力可能不会很快得到缓解。当选总统唐纳德·特朗普(Donald Trump)征收关税和打击移民的计划预计将导致消费者面临物价上涨的局面。

如果这些政策导致通胀持续高企,那么美联储在进一步降低利率方面的空间将会变得更加有限,这无疑会加重信用卡用户的负担。(财富中文网)

译者:中慧言-王芳

美国人在偿还信用卡账单方面遭遇重重困难,这迫使贷款机构放弃追讨债务,进而承受更大的损失。

银行信用卡债务冲销达到了2010年以来的最高水平,彼时消费者仍在努力摆脱金融危机和大衰退的影响。

根据BankRegData编制的联邦存款保险公司(FDIC)季度统计数据,截至2024年前三季度,信用卡债务冲销总额达到457亿美元,较上年同期增长46%。

英国《金融时报》最先报道了今年信用卡债务冲销额激增的情况,这对经济而言是一个潜在的警示信号,因为消费者近年来一直在应对通胀压力和借贷成本上升的双重挑战。

第四季度的数据尚未公布,但很可能会显示进一步增长,原因是年底假日购物热潮期间,冲销额通常会有所上升。

纽约联邦储备银行的另一份数据显示,第三季度信用卡余额增加了240亿美元,目前总额为1.17万亿美元,较上年同期增长8.1%。

尽管信用卡的拖欠率从第二季度的9.1%下降到8.8%,但整体消费者债务的拖欠率从3.2%上升至3.5%。

纽约联邦储备银行(New York Fed)经济研究顾问李东勋(Donghoon Lee)上月在一份声明中表示:“尽管名义上家庭余额仍在持续攀升,但收入增长速度超过了债务增长速度。尽管本季度拖欠情况有所缓解,但拖欠率上升仍表明许多家庭承受着压力。”

Capital One等个人发卡机构近期也表示,其信用卡债务冲销率有所上升。

这种压力表明,尽管国内生产总值增长、薪资增长以及个人收入等经济数据均呈现出积极态势,但消费者在疫情期间及其后掀起的大规模购买热潮,如今正逐渐给他们带来沉重负担。

通胀率已从2022年9%的高位大幅降至11月的2.7%,但物价仍高于疫情前的水平。

与此同时,尽管政策制定者今年已开始下调基准利率,但美联储此前大幅上调基准利率(对信用卡利率产生了影响)所带来的影响仍在持续。

据英国《金融时报》报道,在截至9月份的12个月里,那些未能全额偿还月度信用卡账单的消费者支付了1700亿美元的利息。

消费者的压力可能不会很快得到缓解。当选总统唐纳德·特朗普(Donald Trump)征收关税和打击移民的计划预计将导致消费者面临物价上涨的局面。

如果这些政策导致通胀持续高企,那么美联储在进一步降低利率方面的空间将会变得更加有限,这无疑会加重信用卡用户的负担。(财富中文网)

译者:中慧言-王芳

Americans are having more trouble paying credit card bills, forcing lenders to take steeper losses as they give up on collecting those debts.

Banks are writing off credit card debt at the highest level since 2010, when consumers were still emerging from the aftermath of the financial crisis and Great Recession.

According to quarterly FDIC stats compiled by BankRegData, the total amount charged off through the first three quarters of 2024 reached $45.7 billion, up 46% from the same period a year ago.

This year’s surge, which was first reported by the Financial Times, represents a potential red flag for the economy as consumers have juggled inflation and higher borrowing costs in recent years.

Numbers for the fourth quarter aren’t available yet but likely will show a further increase as write-offs typically tick higher at the end of the year amid the holiday-shopping frenzy.

Separate data from the New York Federal Reserve shows credit card balances grew by $24 billion during the third quarter and now total $1.17 trillion, up 8.1% from a year ago.

While the delinquency rate on card balances improved to 8.8% from 9.1% in the second quarter, the rate across all consumer debt ticked up to 3.5%, from 3.2%.

“Although household balances continue to rise in nominal terms, growth in income has outpaced debt,” Donghoon Lee, economic research advisor at the New York Fed, said in a statement last month. “Still, elevated delinquency rates reveal stress for many households, even amid some moderation in delinquency trends this quarter.”

Individual card issuers like Capital One have also recently flagged increases in their write-off rates.

Such strains indicate the massive buying spree that consumers embarked on during the pandemic and afterward is starting to catch up to them now. That’s despite otherwise positive economic readings on GDP growth, payroll gains, and personal income.

Inflation has cooled sharply from a high of 9% in 2022 to 2.7% in November, but prices are still elevated from pre-pandemic levels.

Meanwhile, the Federal Reserve’s aggressive hiking of benchmark interest rates, which influence credit card rates, is still being felt even as policymakers have started to bring them down this year.

In the 12 months that ended in September, consumers who didn’t fully pay off their monthly credit card bills paid $170 billion in interest, according to the FT.

Consumers may not see much relief soon. President-elect Donald Trump’s plans to impose tariffs and crack down on immigration are expected to result in higher prices for consumers.

And if those policies keep inflation sticky, the Fed will have less leeway to further lower rates, keeping the burden heavy on credit card users.

请打开财富Plus APP